The information and documents contained on the following pages of this website are for information purposes only. These materials do neither constitute an offer nor an invitation to subscribe to or to purchase securities, nor any investment advice or service, and are not meant to serve as a basis for any kind of obligation, contractual or otherwise. The securities described on the following pages have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), and may not be offered or sold in the United States of America (the "United States") absent registration or an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. There will be no public offering of such securities in the United States or anywhere else and, if offered, any such securities will be offered and sold only (i) outside of the United States in "offshore transactions" in accordance with Regulation S of the Securities Act and (ii) in the United States to "qualified institutional buyers" (as defined in Rule 144A under the Securities Act) in transactions exempt from the registration requirements of the Securities Act.

THE FOLLOWING INFORMATION AND DOCUMENTS ARE NOT DIRECTED AT AND ARE NOT INTENDED FOR USE BY (I) PERSONS WHO ARE RESIDENTS OF OR LOCATED IN THE UNITED STATES, CANADA, AUSTRALIA, JAPAN OR SOUTH AFRICA, OR (II) PERSONS IN ANY OTHER JURISDICTION WHERE THE COMMUNICATION OR RECEIPT OF SUCH INFORMATION IS RESTRICTED IN SUCH A WAY THAT PROVIDES THAT SUCH PERSONS SHALL NOT RECEIVE IT. SUCH PERSONS, OR PERSONS ACTING FOR THE BENEFIT OF ANY SUCH PERSONS, ARE NOT PERMITTED TO VISIT THE FOLLOWING PAGES OF THE WEBSITE.

To visit the following parts of this website you must confirm that

(i) you are not a resident of or located in the United States, Canada, Australia, Japan or South Africa,

(ii) you are not a person to whom the communication of the information contained on the website is restricted,

(iii) you will not distribute any of the information and documents contained thereon to any such person, and

(iv) you are not acting for the benefit of any such person.

By clicking on the "Accept" button below, you will be deemed to have made this confirmation.

THIS ANNOUNCEMENT, INCLUDING THE INFORMATION INCLUDED HEREIN, IS RESTRICTED AND IS NOT FOR PUBLICATION, DISTRIBUTION OR RELEASE IN OR INTO THE UNITED STATES OF AMERICA, CANADA, AUSTRALIA, JAPAN, SOUTH AFRICA OR ANY OTHER JURISDICTION IN WHICH OFFERS OR SALES OF THE SECURITIES WOULD BE PROHIBITED BY APPLICABLE LAW.

THIS ANNOUNCEMENT IS FOR INFORMATION PURPOSES ONLY AND IS NOT AN OFFER OF SECURITIES IN ANY JURISDICTION.

- Decisive step in #FutureFresenius highlights another strategic milestone to evolve into a more focused and stronger company.

- Enhances strategic flexibility and financial profile to strengthen the balance sheet

- Demonstrates commitment to long-term sustainable value creation and provides the basis to further strengthen the growth platforms as part of REJUVENATE

- Fresenius intends to retain 25% plus one share of Fresenius Medical Care demonstrating it remains a committed shareholder

- Proceeds will be used in line with stated capital allocation priorities to deliver long-term growth and shareholder value

Fresenius SE & Co. KGaA (Frankfurt/Xetra: FRE) today announced its intention to reduce its stake in Fresenius Medical Care AG ("FME").

Fresenius intends to sell approximately 10.5 million shares of FME (the "Shares"), equivalent to approximately 3.6% of FME's issued share capital, by way of an accelerated bookbuilding procedure (the "Equity Offering"). In addition, Fresenius intends to issue bonds exchangeable into ordinary Shares with approximately 10.5 million Shares underlying, equivalent to approximately 3.6% of FME's issued share capital (the "Exchangeable Bonds" and together with the Equity Offering, the "Combined Offering"). The final size of the respective instruments is to be determined following the completion of the bookbuilding process. Fresenius will retain no less than 25 per cent plus one share of FME.

Fresenius will use the proceeds in line with the #FutureFresenius strategy and the Fresenius' stated capital allocation priorities, including further strengthening the balance sheet, reducing leverage, and delivering long-term growth and shareholder value.

Following the completion of this transaction, Fresenius remains by far the largest shareholder of FME and will continue to actively support the management board through the two Fresenius representatives on the supervisory board of FME.

The placements will start immediately following this announcement and will be addressed to institutional investors only. BofA Securities Europe SA and Goldman Sachs Bank Europe SE are acting as Joint Global Coordinators and alongside BNP Paribas and Deutsche Bank Aktiengesellschaft as Joint Bookrunners on the Combined Offering, with Banco Santander, S.A. acting as Co-Lead Manager. In the context of the placements, Fresenius has agreed to a lock-up undertaking of 180 days, subject to customary exceptions.

The Exchangeable Bonds will have a maturity of 3 years, will be issued with a denomination of EUR 100,000 each at a price between 100.75% and 102.25% of their principal amount and are expected to pay no periodic interest, resulting in a yield-to-maturity of between (0.75)% and (0.25)% per annum. The exchange premium will be set at pricing and is expected to be between 25% and 30% above the placement price per Share in the Equity Offering and the Delta Placement (as defined below).

The Company has been informed by the Joint Bookrunners that the Joint Bookrunners will organize a simultaneous placement of Shares on behalf of certain subscribers of the Exchangeable Bonds who wish to sell these Shares in short sales to purchasers procured by the Joint Bookrunners in order to hedge the market risk to which the subscribers are exposed with respect to the Exchangeable Bonds that they acquire (the "Delta Placement"). The placement price for the Shares sold in the Delta Placement shall be determined via an accelerated bookbuilding process that will be carried out by the Joint Bookrunners concurrently with the Equity Offering. Fresenius will not receive any proceeds, directly or indirectly, from any Shares sold pursuant to the Delta Placement.

This announcement is an advertisement and not a prospectus and not an offer of securities for sale in or into any jurisdiction, including the United States, Canada, Australia, Japan, South Africa or any jurisdiction in which offers or sales of the securities would be prohibited by applicable law. Neither this announcement nor anything contained herein shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

This announcement is not an offer to sell, or solicitation of an offer to buy, any securities in the United States. The securities described herein have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), and may not be offered or sold in the United States absent registration or an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. There will be no public offering of the securities described herein in the United States or anywhere else and, if offered, any such securities will be offered and sold only (i) outside of the United States in "offshore transactions" in accordance with Regulation S of the Securities Act and/or (ii) in the United States to "qualified institutional buyers" (as defined in Rule 144A under the Securities Act) in transactions exempt from the registration requirements of the Securities Act.

This document and the offer when made, in member states of the European Economic Area ("EEA) (each a "Member State") and the United Kingdom, are only addressed to and directed at persons who are "qualified investors" as defined in the EU Prospectus Regulation or the UK Prospectus Regulation ("Qualified Investors"). Each person in a Member State or in the United Kingdom who initially acquires any securities described herein or to whom any offer of such securities may be made and, to the extent applicable, any funds on behalf of which such person is acquiring the Bonds that are located in a Member State or in the United Kingdom will be deemed to have represented, acknowledged and agreed that it is a Qualified Investor.

In addition, in the United Kingdom, this document is only being distributed to and is only directed at (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "Order"), (ii) high net worth entities falling withing Article 49(2) of the Order and (iii) persons at or to whom it can otherwise lawfully be distributed or directed (all such persons together being referred to as "relevant persons"). The securities are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such securities will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this notification or any of its contents.

The information contained in this announcement is for background purposes only and does not purport to be full or complete. No reliance may be placed for any purpose on the information contained in this announcement or its accuracy or completeness. No prospectus will be prepared in connection with the offering of the securities referred to herein. The securities referred to herein may not be offered to the public in any jurisdiction in circumstances which would require the preparation or registration of any prospectus or offering document relating to the securities referred to herein in such jurisdiction.

This announcement may include statements that are, or may be deemed to be, "forward‐looking statements". These forward‐looking statements may be identified by the use of forward‐looking terminology, including the terms "believes", "estimates", "plans", "projects", "anticipates", "expects", "intends", "may", "will" or "should" or, in each case, their negative or other variations or comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions. Forward‐looking statements may and often do differ materially from actual results. Any forward‐looking statements reflect the Company's current view with respect to future events and are subject to risks relating to future events and other risks, uncertainties and assumptions relating to its business, results of operations, financial position, liquidity, prospects, growth or strategies. Forward‐looking statements speak only as of the date they are made.

The Company and its affiliates as well as the Joint Bookrunners, the Co-Lead Manager and their respective affiliates expressly disclaim any obligation or undertaking to update, review or revise any forward-looking statement contained in this announcement whether as a result of new information, future developments or otherwise.

Solely for the purposes of the product governance requirements contained within: (a) EU Directive 2014/65/EU on markets in financial instruments, as amended ("MiFID II"); (b) Articles 9 and 10 of Commission Delegated Directive (EU) 2017/593 supplementing MiFID II; (c) local implementing measures (together, the "MiFID II Product Governance Requirements"); and (d) the FCA Handbook Product Intervention and Product Governance Sourcebook (the "UK MiFIR Product Governance Rules"), and disclaiming all and any liability, whether arising in tort, contract or otherwise, which any "manufacturer" (for the purposes of the MiFID II Product Governance Requirements and UK MiFIR Product Governance Rules) may otherwise have with respect thereto, the Bonds have been subject to a product approval process, which has determined that: (i) the target market for the Bonds is eligible counterparties and professional clients only, each as defined in MiFID II and the UK MiFIR Product Governance Rules; and (ii) all channels for distribution of the Bonds to eligible counterparties and professional clients are appropriate. Any person subsequently offering, selling or recommending the Bonds (a "distributor") should take into consideration the manufacturer's target market assessment; however, a distributor subject to MiFID II or the UK MiFIR Product Governance Rulesis responsible for undertaking its own target market assessment in respect of the Bonds (by either adopting or refining the manufacturer's target market assessment) and determining appropriate distribution channels. The target market assessment is without prejudice to the requirements of any contractual or legal selling restrictions in relation to any offering of the Bonds and/or the underlying shares. For the avoidance of doubt, the target market assessment does not constitute: (a) an assessment of suitability or appropriateness for the purposes of MIFID II or the UK MiFIR Product Governance Rules; or (b) a recommendation to any investor or group of investors to invest in, or purchase, or take any action whatsoever with respect to the Bonds.

The Bonds are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the EEA or the United Kingdom (the "UK"). For these purposes, a "retail investor" means (a) in the EEA, a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of MIFID II; (ii) a customer within the meaning of Directive (EU) 2016/97 (as amended, the "Insurance Distribution Directive"), where that customer would not qualify as a professional client as defined in point (10) of article 4(1) of MIFID II, and (b) in the UK, a person who is one (or more) of (i) a retail client, within the meaning of Regulation (EU) no 2017/565 as it forms part of UK domestic law by virtue of the EUWA or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 of the UK (the "FSMA") and any rules or regulations made under the FSMA to implement Directive (EU) 2016/97, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of regulation (EU) No 600/2014 as it forms part of UK domestic law by virtue of the EUWA.

Consequently, no key information document required by Regulation (EU) No 1286/2014 (the "EU PRIIPs Regulation") or the EU PRIIPS Regulation as it forms part of UK domestic law by virtue of the EUWA (the "UK PRIIPS Regulation") for offering or selling the Bonds or otherwise making them available to retail investors in the EEA or the UK has been prepared and therefore offering or selling the Bonds or otherwise making them available to any retail investor in the EEA or the UK may be unlawful under the EU PRIIPs Regulation and/or the UK PRIIPS Regulation.

The Joint Bookrunners and the Co-Lead Manager are acting exclusively for the Company and no-one else in connection with the Combined Offering. They will not regard any other person as their respective clients in relation to the Combined Offering and will not be responsible to anyone other than the Company for providing the protections afforded to its clients, nor for providing advice in relation to the Combined Offering, the contents of this announcement or any transaction, arrangement or other matter referred to herein.

Any decision to purchase any of the securities described herein should only be made on the basis of an independent review by a prospective investor of the Company's publicly available information. Neither the Joint Bookrunners nor the Co-Lead Manager nor any of their respective affiliates nor any of its or their respective directors, officers, employees, advisers or agents accepts any liability arising from the use of, or make any representation as to the accuracy or completeness of, this announcement or the Company's publicly available information.

No reliance may or should be placed by any person for any purposes whatsoever on the information contained in this announcement or on its completeness, accuracy or fairness. The information in this announcement is subject to change.

* * *

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius SE & Co. KGaA

Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11852

Chairman of the Supervisory Board: Wolfgang Kirsch

General Partner: Fresenius Management SE

Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11673

Management Board: Michael Sen (Chairman), Pierluigi Antonelli, Sara Hennicken, Robert Möller, Dr. Michael Moser

Chairman of the Supervisory Board: Wolfgang Kirsch

The information and documents contained on the following pages of this website are for information purposes only. These materials do neither constitute an offer nor an invitation to subscribe to or to purchase securities, nor any investment advice or service, and are not meant to serve as a basis for any kind of obligation, contractual or otherwise. The securities described on the following pages have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), and may not be offered or sold in the United States of America (the "United States") absent registration or an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. There will be no public offering of such securities in the United States or anywhere else and, if offered, any such securities will be offered and sold only (i) outside of the United States in "offshore transactions" in accordance with Regulation S of the Securities Act and (ii) in the United States to "qualified institutional buyers" (as defined in Rule 144A under the Securities Act) in transactions exempt from the registration requirements of the Securities Act.

THE FOLLOWING INFORMATION AND DOCUMENTS ARE NOT DIRECTED AT AND ARE NOT INTENDED FOR USE BY (I) PERSONS WHO ARE RESIDENTS OF OR LOCATED IN THE UNITED STATES, CANADA, AUSTRALIA, JAPAN OR SOUTH AFRICA, OR (II) PERSONS IN ANY OTHER JURISDICTION WHERE THE COMMUNICATION OR RECEIPT OF SUCH INFORMATION IS RESTRICTED IN SUCH A WAY THAT PROVIDES THAT SUCH PERSONS SHALL NOT RECEIVE IT. SUCH PERSONS, OR PERSONS ACTING FOR THE BENEFIT OF ANY SUCH PERSONS, ARE NOT PERMITTED TO VISIT THE FOLLOWING PAGES OF THE WEBSITE.

To visit the following parts of this website you must confirm that

(i) you are not a resident of or located in the United States, Canada, Australia, Japan or South Africa,

(ii) you are not a person to whom the communication of the information contained on the website is restricted,

(iii) you will not distribute any of the information and documents contained thereon to any such person, and

(iv) you are not acting for the benefit of any such person.

By clicking on the "Accept" button below, you will be deemed to have made this confirmation.

THIS ANNOUNCEMENT, INCLUDING THE INFORMATION INCLUDED HEREIN, IS RESTRICTED AND IS NOT FOR PUBLICATION, DISTRIBUTION OR RELEASE IN OR INTO THE UNITED STATES OF AMERICA, CANADA, AUSTRALIA, JAPAN, SOUTH AFRICA OR ANY OTHER JURISDICTION IN WHICH OFFERS OR SALES OF THE SECURITIES WOULD BE PROHIBITED BY APPLICABLE LAW.

THIS ANNOUNCEMENT IS FOR INFORMATION PURPOSES ONLY AND IS NOT AN OFFER OF SECURITIES IN ANY JURISDICTION.

- Decisive step in #FutureFresenius highlights another strategic milestone to evolve into a more focused and stronger company.

- Enhances strategic flexibility and financial profile to strengthen the balance sheet

- Demonstrates commitment to long-term sustainable value creation and provides the basis to further strengthen the growth platforms as part of REJUVENATE

- Fresenius intends to retain 25% plus one share of Fresenius Medical Care demonstrating it remains a committed shareholder

- Proceeds will be used in line with stated capital allocation priorities to deliver long-term growth and shareholder value

Fresenius SE & Co. KGaA (Frankfurt/Xetra: FRE) today announced its intention to reduce its stake in Fresenius Medical Care AG ("FME").

Fresenius intends to sell approximately 10.5 million shares of FME (the "Shares"), equivalent to approximately 3.6% of FME's issued share capital, by way of an accelerated bookbuilding procedure (the "Equity Offering"). In addition, Fresenius intends to issue bonds exchangeable into ordinary Shares with approximately 10.5 million Shares underlying, equivalent to approximately 3.6% of FME's issued share capital (the "Exchangeable Bonds" and together with the Equity Offering, the "Combined Offering"). The final size of the respective instruments is to be determined following the completion of the bookbuilding process. Fresenius will retain no less than 25 per cent plus one share of FME.

Fresenius will use the proceeds in line with the #FutureFresenius strategy and the Fresenius' stated capital allocation priorities, including further strengthening the balance sheet, reducing leverage, and delivering long-term growth and shareholder value.

Following the completion of this transaction, Fresenius remains by far the largest shareholder of FME and will continue to actively support the management board through the two Fresenius representatives on the supervisory board of FME.

The placements will start immediately following this announcement and will be addressed to institutional investors only. BofA Securities Europe SA and Goldman Sachs Bank Europe SE are acting as Joint Global Coordinators and alongside BNP Paribas and Deutsche Bank Aktiengesellschaft as Joint Bookrunners on the Combined Offering, with Banco Santander, S.A. acting as Co-Lead Manager. In the context of the placements, Fresenius has agreed to a lock-up undertaking of 180 days, subject to customary exceptions.

The Exchangeable Bonds will have a maturity of 3 years, will be issued with a denomination of EUR 100,000 each at a price between 100.75% and 102.25% of their principal amount and are expected to pay no periodic interest, resulting in a yield-to-maturity of between (0.75)% and (0.25)% per annum. The exchange premium will be set at pricing and is expected to be between 25% and 30% above the placement price per Share in the Equity Offering and the Delta Placement (as defined below).

The Company has been informed by the Joint Bookrunners that the Joint Bookrunners will organize a simultaneous placement of Shares on behalf of certain subscribers of the Exchangeable Bonds who wish to sell these Shares in short sales to purchasers procured by the Joint Bookrunners in order to hedge the market risk to which the subscribers are exposed with respect to the Exchangeable Bonds that they acquire (the "Delta Placement"). The placement price for the Shares sold in the Delta Placement shall be determined via an accelerated bookbuilding process that will be carried out by the Joint Bookrunners concurrently with the Equity Offering. Fresenius will not receive any proceeds, directly or indirectly, from any Shares sold pursuant to the Delta Placement.

This announcement is an advertisement and not a prospectus and not an offer of securities for sale in or into any jurisdiction, including the United States, Canada, Australia, Japan, South Africa or any jurisdiction in which offers or sales of the securities would be prohibited by applicable law. Neither this announcement nor anything contained herein shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

This announcement is not an offer to sell, or solicitation of an offer to buy, any securities in the United States. The securities described herein have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), and may not be offered or sold in the United States absent registration or an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act. There will be no public offering of the securities described herein in the United States or anywhere else and, if offered, any such securities will be offered and sold only (i) outside of the United States in "offshore transactions" in accordance with Regulation S of the Securities Act and/or (ii) in the United States to "qualified institutional buyers" (as defined in Rule 144A under the Securities Act) in transactions exempt from the registration requirements of the Securities Act.

This document and the offer when made, in member states of the European Economic Area ("EEA) (each a "Member State") and the United Kingdom, are only addressed to and directed at persons who are "qualified investors" as defined in the EU Prospectus Regulation or the UK Prospectus Regulation ("Qualified Investors"). Each person in a Member State or in the United Kingdom who initially acquires any securities described herein or to whom any offer of such securities may be made and, to the extent applicable, any funds on behalf of which such person is acquiring the Bonds that are located in a Member State or in the United Kingdom will be deemed to have represented, acknowledged and agreed that it is a Qualified Investor.

In addition, in the United Kingdom, this document is only being distributed to and is only directed at (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "Order"), (ii) high net worth entities falling withing Article 49(2) of the Order and (iii) persons at or to whom it can otherwise lawfully be distributed or directed (all such persons together being referred to as "relevant persons"). The securities are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such securities will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this notification or any of its contents.

The information contained in this announcement is for background purposes only and does not purport to be full or complete. No reliance may be placed for any purpose on the information contained in this announcement or its accuracy or completeness. No prospectus will be prepared in connection with the offering of the securities referred to herein. The securities referred to herein may not be offered to the public in any jurisdiction in circumstances which would require the preparation or registration of any prospectus or offering document relating to the securities referred to herein in such jurisdiction.

This announcement may include statements that are, or may be deemed to be, "forward‐looking statements". These forward‐looking statements may be identified by the use of forward‐looking terminology, including the terms "believes", "estimates", "plans", "projects", "anticipates", "expects", "intends", "may", "will" or "should" or, in each case, their negative or other variations or comparable terminology, or by discussions of strategy, plans, objectives, goals, future events or intentions. Forward‐looking statements may and often do differ materially from actual results. Any forward‐looking statements reflect the Company's current view with respect to future events and are subject to risks relating to future events and other risks, uncertainties and assumptions relating to its business, results of operations, financial position, liquidity, prospects, growth or strategies. Forward‐looking statements speak only as of the date they are made.

The Company and its affiliates as well as the Joint Bookrunners, the Co-Lead Manager and their respective affiliates expressly disclaim any obligation or undertaking to update, review or revise any forward-looking statement contained in this announcement whether as a result of new information, future developments or otherwise.

Solely for the purposes of the product governance requirements contained within: (a) EU Directive 2014/65/EU on markets in financial instruments, as amended ("MiFID II"); (b) Articles 9 and 10 of Commission Delegated Directive (EU) 2017/593 supplementing MiFID II; (c) local implementing measures (together, the "MiFID II Product Governance Requirements"); and (d) the FCA Handbook Product Intervention and Product Governance Sourcebook (the "UK MiFIR Product Governance Rules"), and disclaiming all and any liability, whether arising in tort, contract or otherwise, which any "manufacturer" (for the purposes of the MiFID II Product Governance Requirements and UK MiFIR Product Governance Rules) may otherwise have with respect thereto, the Bonds have been subject to a product approval process, which has determined that: (i) the target market for the Bonds is eligible counterparties and professional clients only, each as defined in MiFID II and the UK MiFIR Product Governance Rules; and (ii) all channels for distribution of the Bonds to eligible counterparties and professional clients are appropriate. Any person subsequently offering, selling or recommending the Bonds (a "distributor") should take into consideration the manufacturer's target market assessment; however, a distributor subject to MiFID II or the UK MiFIR Product Governance Rulesis responsible for undertaking its own target market assessment in respect of the Bonds (by either adopting or refining the manufacturer's target market assessment) and determining appropriate distribution channels. The target market assessment is without prejudice to the requirements of any contractual or legal selling restrictions in relation to any offering of the Bonds and/or the underlying shares. For the avoidance of doubt, the target market assessment does not constitute: (a) an assessment of suitability or appropriateness for the purposes of MIFID II or the UK MiFIR Product Governance Rules; or (b) a recommendation to any investor or group of investors to invest in, or purchase, or take any action whatsoever with respect to the Bonds.

The Bonds are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the EEA or the United Kingdom (the "UK"). For these purposes, a "retail investor" means (a) in the EEA, a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of MIFID II; (ii) a customer within the meaning of Directive (EU) 2016/97 (as amended, the "Insurance Distribution Directive"), where that customer would not qualify as a professional client as defined in point (10) of article 4(1) of MIFID II, and (b) in the UK, a person who is one (or more) of (i) a retail client, within the meaning of Regulation (EU) no 2017/565 as it forms part of UK domestic law by virtue of the EUWA or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 of the UK (the "FSMA") and any rules or regulations made under the FSMA to implement Directive (EU) 2016/97, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of regulation (EU) No 600/2014 as it forms part of UK domestic law by virtue of the EUWA.

Consequently, no key information document required by Regulation (EU) No 1286/2014 (the "EU PRIIPs Regulation") or the EU PRIIPS Regulation as it forms part of UK domestic law by virtue of the EUWA (the "UK PRIIPS Regulation") for offering or selling the Bonds or otherwise making them available to retail investors in the EEA or the UK has been prepared and therefore offering or selling the Bonds or otherwise making them available to any retail investor in the EEA or the UK may be unlawful under the EU PRIIPs Regulation and/or the UK PRIIPS Regulation.

The Joint Bookrunners and the Co-Lead Manager are acting exclusively for the Company and no-one else in connection with the Combined Offering. They will not regard any other person as their respective clients in relation to the Combined Offering and will not be responsible to anyone other than the Company for providing the protections afforded to its clients, nor for providing advice in relation to the Combined Offering, the contents of this announcement or any transaction, arrangement or other matter referred to herein.

Any decision to purchase any of the securities described herein should only be made on the basis of an independent review by a prospective investor of the Company's publicly available information. Neither the Joint Bookrunners nor the Co-Lead Manager nor any of their respective affiliates nor any of its or their respective directors, officers, employees, advisers or agents accepts any liability arising from the use of, or make any representation as to the accuracy or completeness of, this announcement or the Company's publicly available information.

No reliance may or should be placed by any person for any purposes whatsoever on the information contained in this announcement or on its completeness, accuracy or fairness. The information in this announcement is subject to change.

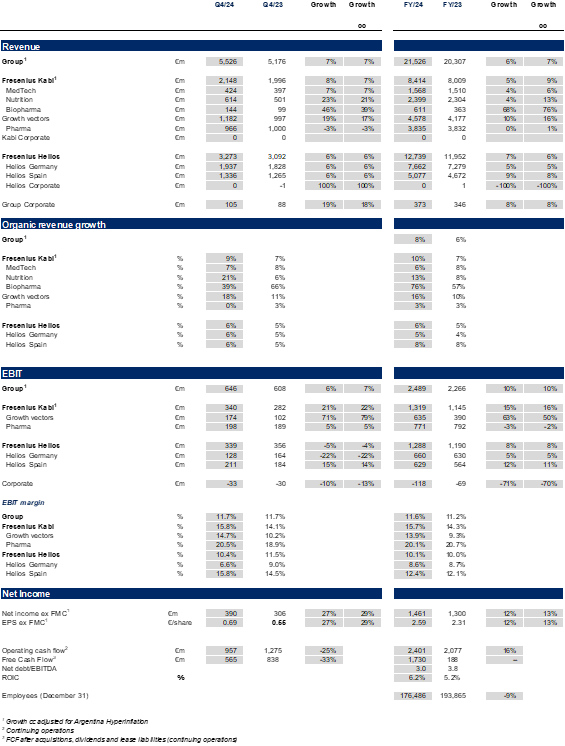

FY/24: Upgraded outlook achieved, consistent financial performance with profitable growth.

- Group revenue1 at €21.5 billion with strong organic growth of 8%1,2

- Group EBIT1 at €2.5 billion, increase of 10%3 in constant currency; EBIT margin1 of 11.6%, 40 bps above prior year

- Net income1,4 grew by 13%3 in constant currency to €1,461 million, outpacing revenue growth

- EPS1,4 grew to €2.59

- Accumulative Group structural productivity savings ahead of plan reached €474 million (planned €400 million)

- Excellent Group operating cash flow of €2.4 billion resulting from focused cash management

- Deleveraging continued, net debt/EBITDA ratio further improved to 3.0x1,5 driven by excellent cash flow. Improvement of more than 70 bps since YE/23

- Dividend proposal of €1.00 per share

Q4/2024: Continued growth and further deleveraging

- Group revenue1 at €5.5 billion with organic growth of 7%1,2 driven by consistent positive development of Kabi and a strong performance at Helios

- Group EBIT1 at €646 million with solid constant currency growth of 7%3 on the back of significant operational improvements at Kabi; end of energy relief payments weighing on Helios Germany; Group EBIT margin1 of 11.7%

- EPS1,4 with outstanding constant currency growth of 29%3 to €0.69, upward impact due to high tax rate in prior-year quarter

- Strong operating cashflow of close to €1 billion in Q4

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

Michael Sen, CEO of Fresenius: “Thanks to a tremendous team effort, Fresenius delivered outstanding results in 2024 with high-single-digit organic revenue growth and double-digit EBIT and EPS growth. Our growth vectors – Nutrition, MedTech and Biopharma – and consistent performance from Helios paced this strong development. On top of this operating success, we ended the year with a significant reduction in leverage, which is at the lowest level in seven years. The momentum for success will continue through 2025, as we move to the next phase of #FutureFresenius and take the company to the next level of performance. For 2025 we expect 4% to 6% in revenue growth and 3% to 7% in EBIT growth. We have also upgraded our ambition level of the Fresenius Financial Framework. This includes higher margin ambitions for Kabi, and for the Group a lower leverage corridor. We also want to pass on our improving financial strength to our shareholders. Thus, we want to recommend a dividend payment for the year of 1 Euro per share. As we move forward, we continue to focus on performance and delivery. Our mission to save and improve human lives is unwavering: Fresenius is Committed to Life."

Outlook for Fiscal Year 2025

Fresenius Group5: Organic revenue growth1,2 of 4% to 6%,

constant currency EBIT growth3 in the range of 3% to 7%

Fresenius Kabi1: Organic revenue growth2,3 in the mid- to high-single-digit percentage range; EBIT margin of 16.0% to 16.5%

Fresenius Helios4: Organic revenue growth2 in the mid-single-digit percentage range; EBIT margin3 around 10%

Assumptions to guidance: Guidance assumes current factors and known uncertainties, but it does not reflect potential extreme scenarios from a fast-moving geopolitical environment.

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 2024 base: €21,526 million (revenue) and €2,489 million (EBIT)

Fresenius Financial Framework – Ambitions further raised

- Structural EBIT margin3 ambition raised for Kabi to 16 to 18% (previously 14 to 17%).

- Self-imposed leverage target corridor upgraded to 2.5 to 3.0x net debt/EBITDA (previously 3.5 to 3.0x)

New dividend policy reflects capital allocation priorities

Fresenius’ new dividend policy is designed to ensure attractive shareholder returns while at the same time providing strategic flexibility. Going forward, Fresenius will pay out 30 to 40% of its Group core net income excluding Fresenius Medical Care and before special items as dividend. For fiscal year 2024, Fresenius will propose a dividend of €1.00 per share. The dividend proposal is a strong increase over the 2022 base and demonstrates Fresenius’ improving financial strength and its commitment to delivering shareholder value. For fiscal year 2023, Fresenius’ dividend payment was interrupted by legal restrictions due to the receipt of the energy relief payments at Helios in Germany.

1 2024 base: €8,414 million (revenue) and €1,319 million (EBIT)

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Before special items

4 2024 base: €12,739 million (revenue) and €1,288 million (EBIT)

5 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

Fresenius Group – Business development FY/24

Fresenius closed fiscal year 2024 with a strong fourth quarter and achieved its twice-upgraded full-year guidance. The consistent positive delivery of Fresenius Kabi and the strong performance at Fresenius Helios, drove an 8%1 year-on-year Group organic revenue1 increase to €21.5 billion. Due to an improved operating business performance, Group EBIT before special items increased 10%3 in constant currency to €2.5 billion. Earnings per share2,4 rose by 13%3 in constant currency to €2.59.

End of 2024, the #FutureFresenius Revitalize phase has been successfully concluded, resulting in significant financial progress driven by a simpler Group structure, improved steering, an optimized portfolio and a refined operating model. In 2025, the focus will be on continued value creation by entering the Rejuvenate phase, which also aims to pursue platform-driven growth. In 2025 the emphasis will be on further debt reduction, delivering higher Kabi margins, drive Helios’ programme and fostering innovation.

A dedicated performance programme for Helios has been set up to increase efficiency and productivity, and to counteract the end of the energy relief funding. The programme is expected to contribute ~€100 million at EBIT level by 2025 at Helios Germany. Combined with further incremental growth of Helios in Germany and Spain, the Fresenius Helios EBIT margin is expected to be around 10% in FY/25. Contributions from the performance programme will be weighted to the second half of 2025, in particular, as some of the levers are process-related and will take time to deliver and realize benefits. Some of the performance measures are likely to materialize fully beyond 2025. This sets an excellent basis for further improving productivity within the 10 to 12% structural margin band in 2026 and beyond.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Ex Fresenius Medical Care

Operating Companies – Business development FY/24 and Q4

Fresenius Kabi

In FY/24, Fresenius Kabi delivered consistent financial performance over the course of the year with excellent organic revenue growth of 10% above the top-end of the structural growth band and an impressive EBIT margin expansion of 140 bps to 15.7%.

Q4/24: Fresenius Kabi delivered a strong finish to the year

- Organic revenue growth of 9%1 driven by positive pricing effects, particularly in Argentina, revenue increased by 8% to €2,148 million.

- Growth vectors with strong organic revenue1 increase of 18%: MedTech 7%, Nutrition 21%, Biopharma 39%.

- Nutrition revenue: €614 million, benefited from positive pricing effects in Argentina and the good development in the U.S., driven by the ongoing roll-out of lipid emulsions.

- Biopharma revenue: €144 million, driven by the overall good rollout of Tyenne in Europe and the U.S.

- MedTech revenue: €424 million, driven by a broad-based positive development across most regions, including the U.S. and Europe

- Pharma revenue: €966 million, flat organic revenue development1; the positive development in many regions was offset by a softer development in China.

- China business continued to be impacted by a general economic weakness, price declines in connection with tenders, and indirect effects of the government’s countrywide anti-corruption campaign.

- EBIT2 of Fresenius Kabi grew 21% to €340 million, driven by good revenue development and improved structural productivity. The EBIT-margin2 was 15.8%, a 170 bps expansion.

- EBIT2 of the Growth Vectors increased by 71% on a positive development across the board; EBIT margin2 was 14.7%. EBIT positive in Biopharma in FY/24.

- EBIT2 of Pharma increased by 5% to €198 million. EBIT margin2 was 20.5% driven in particulars by cost discipline.

1 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

2 Before special items

Fresenius Helios

In FY 2024, Fresenius Helios delivered organic revenue growth of 6% driven by solid activity growth and favorable price developments in Germany and Spain. EBIT margin of 10.1%1 within the structural margin band ambition.

Q4/24: Fresenius Helios with strong EBIT development in Spain; end of energy relief payments weighing on Helios Germany

- Strong 6% organic revenue growth at the top-end of structural growth band driven equally by Helios Germany (6% organic growth) and Helios Spain (6% organic growth); revenue before special items increased 6% to €3,273 million.

- Helios Germany with revenue of €1,937 million; growth driven by pricing effects and admissions growth.

- Helios Spain with revenue before special items of €1,336 million, driven by solid activity levels and favourable price effects. The clinics in Latin America also showed a good performance.

- EBIT1 of Fresenius Helios declined 5% to €339 million as the energy relief funds ended in Q4. EBIT margin1 was solid at 10.4% driven by the excellent profitability at Helios Spain with a margin of 15.8% and 15% EBIT growth.

- EBIT1 of Helios Germany decreased by 22% to €128 million as the prior-year quarter was significantly supported by energy relief funds.

- Dedicated Helios performance programme initiated to drive further operational excellence and compensate end of energy relief funding in Germany. Fresenius Helios EBIT margin is expected to be around 10% in FY/25.

1 Before special items

Group figures Q4 & FY 2024

Conference call and Audio webcast

As part of the publication Fourth Quarter and Full Year 2024 results, a conference call will be held on February 26, 2025 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on our website.

Contact for shareholders

Investor Relations

Telephone: + 49 61 72 6 08-24 87

Telefax: + 49 61 72 6 08-24 88

E-mail: ir-fre@fresenius.com

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q4/2024.

- Consolidated results for Q4/24 as well as for Q4/23 include special items. An overview of the results for Q4/2024 - before and after special items – is available on our website.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q4/24 and Q4/23 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

- Information on the performance indicators is available on our website at www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

-

Fresenius Management Board (from left to right): Pierluigi Antonelli, Sara Hennicken, Michael Sen, Robert Möller, Dr. Michael Moser Download Image (JPG 3.05 MB) -

![]()

Michael Sen, CEO of Fresenius: "As we move forward, we continue to focus on performance and delivery. Our mission to save and improve human lives is unwavering: Fresenius is Committed to Life." Download Image (JPG 2.90 MB)

An overview of key financial figures is available at the end of the release.

FY/24: Upgraded outlook achieved, consistent financial performance with profitable growth.

- Group revenue1 at €21.5 billion with strong organic growth1,2 of 8%

- Group EBIT1 at €2.5 billion, increase of 10%3 in constant currency; EBIT margin1 of 11.6%, 40 bps above prior year

- Net income1,4 grew by 13%3 in constant currency to €1,461 million, outpacing revenue growth

- EPS1,4 grew to €2.59

- Accumulative Group structural productivity savings ahead of plan reached €474 million (planned €400 million)

- Excellent Group operating cash flow of €2.4 billion resulting from focused cash management

- Deleveraging continued: net debt/EBITDA ratio further improved to 3.0x1,5 driven by excellent cash flow. Decline of more than 70 bps since YE/23

- Dividend proposal of €1.00 per share

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation.

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

Q4/2024: Continued growth and further deleveraging

- Group revenue1 at €5.5 billion with organic growth of 7%1,2 driven by consistent positive development of Kabi and a strong performance at Helios

- Group EBIT1 at €646 million with solid constant currency growth of 7%3 on the back of significant operational improvements at Kabi; end of energy relief payments weighing on Helios Germany; Group EBIT margin1 of 11.7%

- EPS1,4 with outstanding constant currency growth of 29%3 to €0.69; upward impact due to high tax rate in prior-year quarter

- Strong operating cashflow of close to €1 billion in Q4

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

Michael Sen, CEO of Fresenius: “Thanks to a tremendous team effort, Fresenius delivered outstanding results in 2024 with high-single-digit organic revenue growth and double-digit EBIT and EPS growth. Our growth vectors – Nutrition, MedTech and Biopharma – and consistent performance from Helios paced this strong development. On top of this operating success, we ended the year with a significant reduction in leverage, which is at the lowest level in seven years.

The momentum for success will continue through 2025, as we move to the next phase of #FutureFresenius and take the company to the next level of performance. For 2025 we expect 4% to 6% in revenue growth and 3% to 7% in EBIT growth. We have also upgraded our ambition level of the Fresenius Financial Framework. This includes higher margin ambitions for Kabi, and for the Group a lower leverage corridor.

We also want to pass on our improving financial strength to our shareholders. Thus, we want to recommend a dividend payment for the year of 1 Euro per share.

As we move forward, we continue to focus on performance and delivery. Our mission to save and improve human lives is unwavering: Fresenius is Committed to Life."

Outlook for Fiscal Year 2025

Fresenius Group1: Organic revenue growth3,5 of 4% to 6%,

constant currency EBIT growth4 in the range of 3% to 7%

Fresenius Kabi2: Organic revenue growth3 in the mid- to high-single-digit percentage range; EBIT margin5 of 16.0% to 16.5%

Fresenius Helios6: Organic revenue growth5 in the mid-single-digit percentage range; EBIT margin5 around 10%

Assumptions to guidance: Guidance assumes current factors and known uncertainties, but it does not reflect potential extreme scenarios from a fast-moving geopolitical environment.

Fresenius Financial Framework – Ambitions further raised

- Structural EBIT margin5 ambition raised for Kabi to 16 to 18% (previously 14 to 17%).

- Self-imposed leverage target7 corridor upgraded to 2.5 to 3.0x net debt/EBITDA (previously 3.5 to 3.0x)

New dividend policy reflects capital allocation priorities

Fresenius’ new dividend policy is designed to ensure attractive shareholder returns while at the same time providing strategic flexibility. Going forward, Fresenius will pay out 30 to 40% of its Group core net income excluding Fresenius Medical Care and before special items as dividend.

For fiscal year 2024, Fresenius wants to propose a dividend of €1.00 per share. The dividend proposal is a strong increase over the 2022 base and demonstrates Fresenius’ improving financial strength and its commitment to delivering shareholder value.

For fiscal year 2023, Fresenius’ dividend payment was interrupted by legal restrictions due to the receipt of the energy relief payments at Helios in Germany.

1 2024 base: €21,526 million (revenue) and €2,489 million (EBIT)

2 2024 base: €8,414 million (revenue) and €1,319 million (EBIT)

3 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

4 Growth rate adjusted for Argentina hyperinflation

5 Before special items

6 2024 base: €12,739 million (revenue) and €1,288 million (EBIT)

7 At expected average exchange rates for both net debt and EBITDA; pro forma closed

acquisitions/divestitures; excluding further potential acquisitions/divestitures; before

special items; including lease liabilities, including Fresenius Medical Care dividend

Fresenius Group – Business development FY/24

Fresenius closed fiscal year 2024 with a strong fourth quarter and achieved its twice-upgraded full-year guidance. The consistent positive delivery of Fresenius Kabi and the strong performance at Fresenius Helios drove an 8%1 year-on-year group organic revenue2 increase to €21.5 billion. Due to an improved operating business performance, Group EBIT before special items increased 10%3 in constant currency to €2.5 billion. Earnings per share2,4 rose by 13%3 in constant currency to €2.59.

End of 2024, the #FutureFresenius Revitalize phase has been successfully concluded, resulting in significant financial progress driven by a simpler Group structure, improved steering, an optimized portfolio and a refined operating model. In 2025, the focus will be on continued value creation by entering the Rejuvenate phase, which also aims to pursue platform-driven growth. In 2025 the emphasis will be on further debt reduction, delivering higher Kabi margins, drive Helios’ program and fostering innovation.

A dedicated performance programme for Helios has been set up to increase efficiency and productivity, and to counteract the end of the energy relief funding. The programme is expected to contribute ~€100 million at EBIT level by 2025 at Helios Germany. Combined with further incremental growth of Helios in Germany and Spain, the Fresenius Helios EBIT margin is expected to be around 10% in FY/25. Contributions from the performance programme will be weighted to the second half of 2025, in particular, as some of the levers are process-related and will take time to deliver and realize benefits. Some of the performance measures are likely to materialize fully beyond 2025. This sets an excellent basis for further improving productivity within the 10 to 12% structural margin band in 2026 and beyond.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Ex Fresenius Medical Care

Operating Companies – Business development FY/24 and Q4

Fresenius Kabi

In FY/24, Fresenius Kabi delivered consistent financial performance over the course of the year with excellent organic revenue growth of 10%1 above the top-end of the structural growth band and an impressive EBIT margin2 expansion of 140 bps to 15.7%.

Q4/24: Fresenius Kabi delivered a strong finish to the year

- Organic revenue growth of 9%1 driven by positive pricing effects, particularly in Argentina, revenue increased by 8% to €2,148 million.

- Growth vectors with strong organic revenue1 increase of 18%: MedTech 7%, Nutrition 21%, Biopharma 39%.

- Nutrition revenue: €614 million, benefited from positive pricing effects in Argentina and the good development in the U.S., driven by the ongoing roll-out of lipid emulsions.

- Biopharma revenue: €144 million, driven by the overall good rollout of Tyenne in Europe and the U.S.

- MedTech revenue: €424 million, driven by a broad-based positive development across most regions, including the U.S. and Europe

- Pharma revenue: €966 million, flat organic revenue development1; the positive development in many regions was offset by a softer development in China.

- China business continued to be impacted by a general economic weakness, price declines in connection with tenders, and indirect effects of the government’s countrywide anti-corruption campaign.

- EBIT2 of Fresenius Kabi grew 21% to €340 million, driven by good revenue development and improved structural productivity. The EBIT-margin2 was 15.8%, a 170 bps expansion.

- EBIT2 of the Growth Vectors increased by 71% on a positive development across the board; EBIT margin2 was 14.7%. EBIT positive in Biopharma in FY/24.

- EBIT2 of Pharma increased by 5% to €198 million. EBIT margin2 was 20.5% driven in particular by cost discipline.

1 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

2 Before special items

Fresenius Helios

In FY 2024, Fresenius Helios delivered organic revenue growth of 6% driven by solid activity growth and favorable price developments in Germany and Spain. EBIT margin1 of 10.1% within the structural margin band ambition.

Q4/24: Fresenius Helios with strong EBIT development in Spain; end of energy relief payments weighing on Helios Germany

- Strong 6% organic revenue growth at the top-end of structural growth band driven equally by Helios Germany (6% organic growth) and Helios Spain (6% organic growth); revenue before special items increased 6% to €3,273 million.

- Helios Germany with revenue of €1,937 million; growth driven by pricing effects and admissions growth.

- Helios Spain with revenue before special items of €1,336 million, driven by solid activity levels and favourable price effects. The clinics in Latin America also showed a good performance.

- EBIT1 of Fresenius Helios declined 5% to €339 million as the energy relief funds ended in Q4. EBIT margin1 was solid at 10.4% driven by the excellent profitability at Helios Spain with a margin of 15.8% and 15% EBIT growth.

- EBIT1 of Helios Germany decreased by 22% to €128 million as the prior-year quarter was significantly supported by energy relief funds.

- Dedicated Helios performance programme initiated to drive further operational excellence and compensate end of energy relief funding in Germany. Fresenius Helios EBIT margin is expected to be around 10% in FY/25.

1 Before special items

Financial figures and growth rates adjusted for the divestment of the fertility services group

Eugin and the hospital stake in Peru.

Group figures Q4 & FY 2024

Note on the presentation of financial figures

- If no timeframe is specified, information refers to Q4/2024.

- Consolidated results for Q4/24 as well as for Q4/23 include special items. An overview of the results for Q4/2024 - before and after special items – is available on our website.

- The results of Fresenius Helios and accordingly of the Fresenius Group for Q4/24 and Q4/23 are adjusted by the sale of the fertility services group Eugin and the divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru.

- Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

- Information on the performance indicators is available on our website at https://www.fresenius.com/alternative-performance-measures.

* * *

Conference call and Audio webcast

As part of the publication Fourth Quarter and Full Year 2024 results, a conference call will be held on February 26, 2025 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

Fresenius SE & Co. KGaA

Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11852

Chairman of the Supervisory Board: Wolfgang Kirsch

General Partner: Fresenius Management SE

Registered Office: Bad Homburg, Germany / Commercial Register: Amtsgericht Bad Homburg, HRB 11673

Management Board: Michael Sen (Chairman), Pierluigi Antonelli, Sara Hennicken, Robert Möller, Dr. Michael Moser

Chairman of the Supervisory Board: Wolfgang Kirsch

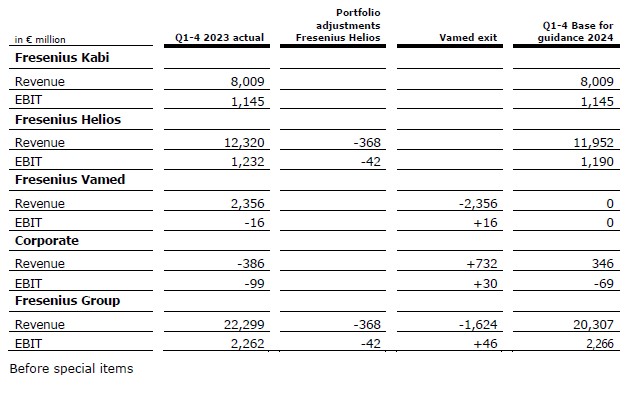

Fresenius entered an agreement with Worldwide Hospital Group (WWH) to fully divest Vamed’s international project business (Health Tech Engineering, HTE). In May 2024, Fresenius originally announced a gradual wind-down of the HTE project business, largely to be completed by 2026, as part of Fresenius’ structured exit from its Investment Company Vamed. The divestment will now accelerate the exit and enable Fresenius to further increase focus and management capacity on the ongoing progress of its core businesses Fresenius Kabi and Fresenius Helios, in line with #FutureFresenius. For the employees of Vamed’s international project business, the transaction offers the perspective of the continuation of the business.

Worldwide Hospitals Group (WWH), a healthcare company based in Germany, specializes in delivering flexible modular hospital solutions—both at sea and on land. Vamed's international project business will complement and enhance WWH's core business.

Closing is expected mid of 2025 and subject to the fulfilment of certain closing conditions.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release

Fresenius entered an agreement with Worldwide Hospital Group (WWH) to fully divest Vamed’s international project business (Health Tech Engineering, HTE). In May 2024, Fresenius originally announced a gradual wind-down of the HTE project business, largely to be completed by 2026, as part of Fresenius’ structured exit from its Investment Company Vamed. The divestment will now accelerate the exit and enable Fresenius to further increase focus and management capacity on the ongoing progress of its core businesses Fresenius Kabi and Fresenius Helios, in line with #FutureFresenius. For the employees of Vamed’s international project business, the transaction offers the perspective of the continuation of the business.

Worldwide Hospitals Group (WWH), a healthcare company based in Germany, specializes in delivering flexible modular hospital solutions—both at sea and on land. Vamed's international project business will complement and enhance WWH's core business.

Closing is expected mid of 2025 and subject to the fulfilment of certain closing conditions.

Fresenius SE & Co. KGaA (Frankfurt/Xetra: FRE) is a global healthcare company headquartered in Bad Homburg v. d. Höhe, Germany. In the 2023 fiscal year, Fresenius generated €22.3 billion in annual revenue. Fresenius offers solutions to the social challenges posed by a growing and ageing population and the resulting need for affordable, high-quality healthcare. Fresenius currently counts over 175,000 employees. The Fresenius Group comprises the operating companies Fresenius Kabi and Fresenius Helios as well as the investment company Fresenius Medical Care. With 140 hospitals and countless outpatient facilities, Fresenius Helios is the leading private hospital operator in Germany and Spain, treating around 26 million patients every year. Fresenius Kabi’s product portfolio includes a range of highly complex biopharmaceuticals, clinical nutrition, medical technology, and generic intravenous drugs. Fresenius was established in 1912 by the Frankfurt pharmacist Dr. Eduard Fresenius. After his death, Else Kröner took over management of the company in 1952. She laid the foundations for a global enterprise that today pursues the goal of improving people’s health. The largest shareholder is the non-profit Else Kröner-Fresenius Foundation, which is dedicated to advancing medical research and supporting humanitarian projects.

Fresenius has signed a new five-year global contract with Microsoft focused on collaboration and IT security for all Fresenius employees. Starting in June 2025, the contract will encompass tools such as Microsoft Defender, Microsoft 365, SharePoint, OneDrive, and Microsoft Power BI, combining the license demands of all Fresenius segments under one agreement. The objective is to streamline and simplify daily office operations for employees while enhancing security capabilities.

“This contract represents another milestone and is a substantial improvement to our IT foundation. We are moving to a comprehensive and state-of-the-art ecosystem across all segments,” says Ingo Elfering, Chief Information Officer of the Fresenius Group.

The collaboration between Fresenius and Microsoft, expanding since 2022, focuses on cloud computing, security features, collaboration features and AI enablement. It has facilitated successful large-scale cloud migrations at Fresenius and established the groundwork for further innovation and change initiatives.

“Our Microsoft technology helps Fresenius to focus more on their customers and patients and less on IT management. Security and data protection are our top priorities in its development. Microsoft plays a central role in the digital ecosystem, and this comes with a critical responsibility to earn and maintain trust, especially in healthcare”, explains Michael Sahnau, Director Health & Life Science at Microsoft Germany.

Looking ahead, the collaboration will enhance the capabilities especially of Fresenius’ Helios Group with advanced Artificial Intelligence adoption and new cloud technologies. It will also expand across all of Fresenius cloud migration strategy and a modern, harmonized, and cost-efficient IT framework.

Fresenius SE & Co. KGaA (Frankfurt/Xetra: FRE) is a global healthcare company headquartered in Bad Homburg v. d. Höhe, Germany. In the 2023 fiscal year, Fresenius generated €22.3 billion in annual revenue. Fresenius offers solutions to the social challenges posed by a growing and ageing population and the resulting need for affordable, high-quality healthcare. Fresenius currently counts over 175,000 employees. The Fresenius Group comprises the operating companies Fresenius Kabi and Fresenius Helios as well as the investment company Fresenius Medical Care. With 140 hospitals and countless outpatient facilities, Fresenius Helios is the leading private hospital operator in Germany and Spain, treating around 26 million patients every year. Fresenius Kabi’s product portfolio includes a range of highly complex biopharmaceuticals, clinical nutrition, medical technology, and generic intravenous drugs. Fresenius was established in 1912 by the Frankfurt pharmacist Dr. Eduard Fresenius. After his death, Else Kröner took over management of the company in 1952. She laid the foundations for a global enterprise that today pursues the goal of improving people’s health. The largest shareholder is the non-profit Else Kröner-Fresenius Foundation, which is dedicated to advancing medical research and supporting humanitarian projects.

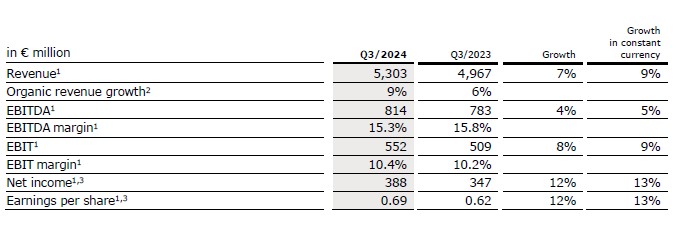

- Group organic revenue growth of 9%1,2 to €5.3 billion2 driven by a strong Kabi performance and good organic growth at Helios.

- Strong bottom-line traction with Group EBIT2 increase in constant currency of 9%3 to €552 million and EPS growth of 7%2,3,4.

- Group outlook for fiscal 2024 upgraded; Organic revenue growth1,2 is now expected to grow between 6% to 8% (previous: between 4% to 7%) and EBIT growth2 in constant currency is now targeted to be in the 8 to 11% range (previous: between 6% to 10%).

- Group-wide cost and productivity savings ahead of plan with target for FY/24 already achieved YTD.

- Excellent operating cash flow resulting from focused cash management.

- Deleveraging continued, and leverage ratio further improved to 3.24x2,5 driven by excellent cash flow; Leverage target corridor under review.

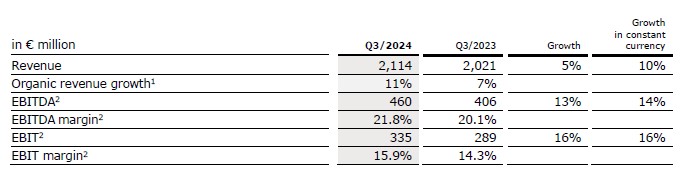

- Fresenius Kabi delivering above the top-end of the structural growth band with organic revenue growth of 11%6; strong EBIT margin at 15.9%2.

- Growth Vectors at Kabi show continued strong performance, led by dynamic growth at Biopharma, which had yet again positive EBIT in Q3. Tyenne is in line with expectations, building on strong momentum.

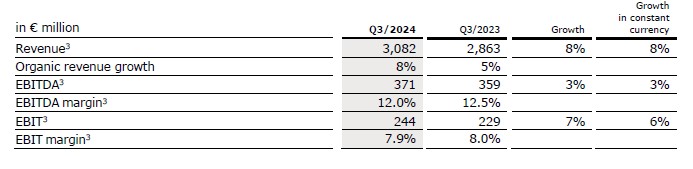

- Fresenius Helios with excellent organic revenue growth of 8% driven by solid performance in Spain and supported by some favorable technical reclassifications in Germany; EBIT margin of 7.9%2 in line with expectations due to anticipated lower seasonal demand in Spain; last quarter of energy relief funding support.

- Dedicated Helios performance program underway to drive further operational excellence and compensate ending energy relief funding in Germany.

Michael Sen, CEO of Fresenius: Team Fresenius delivered an excellent third quarter in 2024 – all financial metrics improved versus the prior year. Revenues grew strongly, with margin expansion across the Group, and significantly improved cash flow generation. Both Kabi and Helios continue to deliver consistent and sustained financial performance. We are more focused and stronger, deploying our cash to reduce debt further, while growing earnings per share and driving shareholder returns. Quarter after quarter we are showing how our #FutureFresenius strategy is paying off. Our mission remains at the core of our activities: saving and improving human lives. Fresenius is: Committed to Life.” Sen continued, “Given the strength of our first nine months, we are upgrading our revenue and earnings guidance for the year.”

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

6 Organic growth rate adjusted for the accounting effects related to Argentina hyperinflation.

Conference call and Audio webcast

As part of the publication of the results for Q3/24, a conference call will be held on November 6, 2024 at 1:30 p.m. CET (7:30 a.m. EST). All investors are cordially invited to follow the conference call in a live audio webcast at www.fresenius.com/investors. Following the call, a replay will be available on

our website.

Note on the presentation of financial figures

An overview of the presentation of the financial figures are available on page 14 of this Investor News.

Structural productivity improvements: Target achieved ahead of plan

The Group-wide cost and efficiency measures are progressing faster than planned. The target for annual sustainable cost savings of ~€400 million at EBIT level has already been achieved with accumulative savings totaling €408 million until the end of Q3/24. Originally, it was expected to achieve the target by year-end 2025.

Fresenius will continue its efforts to increase structural productivity. So far, Kabi has delivered the majority of the savings. Going forward, it will be Fresenius Helios with its dedicated efficiency program focused on operations excellence including reduction of process and waiting times and digitalization of processes, resource optimization and synergies in particular in logistics and procurement. An update will be provided as part of the FY/24 results in February 2025.

Further efforts to enhance structural efficiency will, however, also be driven forward by Fresenius Kabi and the Corporate Center. Key elements include measures to reduce complexity, optimize supply chains and improve procurement processes.

Group sales and earnings development

Group revenue before special items increased by 7% (9% in constant currency) to €5,303 million (Q3/23: €4,967 million). Organic growth was 9%2, driven by Kabi and Helios's ongoing strong performance. Currency translation had a negative effect of 2% on revenue growth.

Group EBITDA before special items increased by 4% (5% in constant currency) to €814 million (Q3/23: €783 million).

Group EBIT before special items increased by 8% (9% in constant currency) to €552 million (Q3/23: €509 million), mainly driven by the strong organic revenue growth at Kabi and Helios and the continued progress of the groupwide cost savings program. The EBIT margin before special items was 10.4% (Q3/23: 10.2%). Reported Group EBIT was €492 million (Q3/23: €362 million).

Group net interest before special items increased to -€116 million (Q3/23: -€102 million) mainly due to financing activities in a higher interest rate environment.

Group tax rate before special items was 24.5% (Q3/23: 23.1%).

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

Net income1 from deconsolidated Fresenius Medical Care operations before special items increased by 38% (42% in constant currency) to €76 million (Q3/231: €55 million).

Group net income1 before special items increased by 12% (13% in constant currency) to €388 million (Q3/231: €347 million). The increase was driven by operating strength. Reported Group net income1 increased to €326 million (Q3/231: -€406 million) mainly due to Fresenius Medical Care's positive net income contribution. The negative net income in the prior year period was due to the non-cash valuation effect of Fresenius Medical Care in accordance with IFRS 5.

Group net income1 before special items excluding Medical Care increased by 7% (7% in constant currency) to €312 million (Q3/231: €292 million).

Earnings per share1 before special items increased by 12% (13% in constant currency) to €0.69 (Q3/231: €0.62). Reported earnings per share1 were €0.58 (Q3/231: -€0.72).

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at

Financial Results | FSE (fresenius.com).

Group Cash flow development

Group operating cash flow (continuing operations) increased to €763 million (Q3/23: €603 million) mainly driven by the very good operational business development and improvements in working capital at Helios and Kabi. Group operating cash flow margin was 14.4% (Q3/23: 12.1%). Before acquisitions, dividends and lease liabilities, free cash flow (continuing operations) increased to €532 million (Q3/23: €346 million). After acquisitions, dividends and lease liabilities, free cash flow (continuing operations) improved to €623 million (Q3/23: €102 million).

Fresenius Kabi’s operating cash flow remained almost stable at €374 million (Q3/23: €380 million) with a margin of 17.7% (Q3/23: 18.8%).

Fresenius Helios’ operating cash flow increased to €454 million (Q3/23: €208 million) due to the strong focus on cash and working capital management in Germany and Spain. The operating cash flow margin improved to 14.7% (Q3/23: 7.3%).

The cash conversion rate (CCR), which is defined as the ratio of adjusted free cash flow1 to EBIT before special items was 1.2 in Q3/24 (LTM) (Q3/23: 0.9, LTM). This positive development is due to the strong cash flow focus across the Group.

The CCR is expected to be around 1 in FY/24.

1Cash flow before acquisitions and dividends; before interest, tax, and special items

Group leverage

Group debt decreased by -16% (-16% in constant currency) to €13,317 million

(Dec. 31, 2023: € 15,830 million) mainly related to the repayment of debt based on the excellent cash flow development and the around €400 million reduction of the leasing liabilities related to the Vamed exit. Group net debt decreased by -11%

(-11% in constant currency) to € 11,823 million (Dec. 31, 2023: € 13,268 million).

As of September 30, 2024, the net debt/EBITDA ratio was 3.24x1,2 (Dec. 31, 2023: 3.76x1,2) corresponding to a reduction of 52 bps compared to Dec. 31, 2023. This achievement is due to a combination of better EBITDA and Free cash flow. The legally required suspension of dividend payments and the Vamed exit further supported the positive development. Compared to Q3/23 (4.03x1,2) this is a 79 bps reduction.

Fresenius anticipates improving net debt/EBITDA ratio further3 towards the lower end of the self-imposed corridor of 3.0 to 3.5x by year-end 2024. This is expected to be driven by further reducing net debt and operational performance of the Operating Companies.

ROIC was 6.1% in Q1-3/24 (FY/23: 5.2%) mainly driven by the improvement in EBIT and the stringent capital allocation. With that, ROIC is within the ambition range of 6% to 8%. For 2024, Fresenius expects ROIC to be above 6.0% (previous: around 6.0%).

1 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

2 Before special items