- Group revenue +5% (+7% at constant currency), driven by very good results in health care services

- Considerable net income growth of 22%, supported by lower costs for health care supplies and Global Efficiency Program

- Strong operating performance in North America: revenue +8%, operating income (EBIT) +20%

- Care Coordination maintains significant revenue growth (+21%) and continues to invest in infrastructure

- Fresenius Medical Care on track to achieve full year guidance

Key figures – second quarter 2016

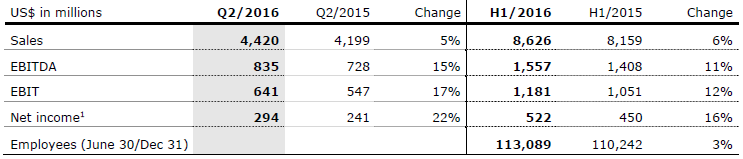

Net revenue: $4,420 million, +5 %

Operating income: (EBIT) $641 million, +17 %

Net income1: $294 million, +22 %

Basic earnings per share: $0.96, +22 %

Key figures – first half 2016

Net revenue: $8,626 million, +6 %

Operating income (EBIT): $1,181million, +12 %

Net income1: $522 million, +16 %

Basic earnings per share: $1.71, +15 %

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

“Following a solid start to the year, we have accelerated our growth in the second quarter”, said Rice Powell, Chief Executive Officer of Fresenius Medical Care. “Our strong earnings growth demonstrates our ability to further improve our cost base and the success of our Global Efficiency Program. I am extremely pleased with our excellent operational performance in the core dialysis services business. Care Coordination maintains strong topline growth and we continue to invest in the infrastructure of this business. Despite unfavorable foreign currency developments and continuous cost pressure, we are confident we will achieve our full year guidance.”

Revenue & earnings

Net revenue for the second quarter improved by 5% and reached $4,420 million (+7% at constant currency), driven by very good health care services revenue growth in North America. Health care services revenue increased by 7% to $3,571 million, mainly due to organic revenue growth. Dialysis products revenue decreased by 1% to $849 million in the second quarter, impacted by negative currency developments (+2% at constant currency) and compared to an exceptionally strong performance in the previous year’s second quarter. The revenue increase at constant exchange rates was driven by higher sales of dialyzers and machines.

Net revenue in the first half of 2016 increased by 6% (health care services revenue +7%/+9% at constant currency; dialysis products revenue +1%/+4% at constant currency).

In the second quarter, operating income (EBIT) increased by 17% to $641 million. The operating income margin increased to 14.5%, due to strong operating performance across all segments. The increase in North America was supported by lower costs for health care supplies and a favorable impact from higher volume with commercial payors. This was partially offset by higher personnel expenses related to dialysis services in the North America segment. The increase in the Asia-Pacific segment was driven by favorable exchange rate effects and higher business growth.

For the first half of 2016, operating income (EBIT) increased by 12% to $1,181 million.

Net interest expense in the second quarter remained at the previous year’s level ($102 million). For the first half of 2016, net interest expense increased by 2% to $208 million.

Income tax expense increased to $169 million in the second quarter. This translates into an effective tax rate of 31.3%, an increase of 90 basis points compared to Q2 2015 (30.4%). This increase was mainly driven by a relative to income before taxes lower increase of tax-free income attributable to noncontrolling interests.

For the first half of 2016, tax expense increased to $306 million, translating into an effective tax rate of 31.5% (-70 basis points).

Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA increased by 22% to $294 million in the second quarter, mainly driven by the strong performance of the North America segment. Based on approximately 305.5 million shares (weighted average number of shares outstanding), basic earnings per share (EPS) increased accordingly to $0.96 (+22%), compared to $0.79 in the previous year’s second quarter.

For the first half of 2016, net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA increasead by 16% to $522 million.

Segment development

In the second quarter, North America revenue increased by 8% to $3,168 million (72% of total revenue). Health care services revenue grew by 8% to $2,938 million, of which Care Coordination contributed $564 million (+21%), supported by considerable organic revenue growth of 17%. Dialysis care revenue contributed $2,374 million (+5%), driven by growth in dialysis treatments and increases in revenue per treatment. Dialysis products revenue grew by 2% to $230 million, due to increased product sales (especially machines and dialyzers). Operating income in North America came in at $513 million (+20%). The substantially improved operating income margin of 16.2% (+170 basis points) was attributable to lower costs for health care supplies, a favorable impact from commercial payors, lower legal expenses and increased income from equity method investees. This was partially offset by higher personnel expenses related to dialysis services and a lower margin in Care Coordination. The margin decrease in Care Coordination was driven by increased costs for hospitalist and intensivist services due to further infrastructure development, partially offset by one-time gains from the endovascular and cardiovascular services business.

For the first half of 2016, North America revenue increased by 9% to $6,212 million. Operating income increased by 24% to $949 million.

EMEA revenue increased by 1% to $676 million in the second quarter of 2016 (+3% at constant currency). Health care services revenue for the EMEA segment increased by 7% (+9% at constant curreny) to $331 million. This was the result of contributions from acquisitions (7%) and organic revenue growth (3%), partially offset by the negative effect of exchange rate fluctuations (2%) and the effect of closed or sold clinics (1%). Dialysis treatments increased by 9% in the second quarter. Dialysis products revenue decreased by 4% (-3% at constant currency) to $345 million. The decrease was driven by lower sales of dialyzers, machines, renal pharmaceuticals and bloodlines, partially offset by higher sales of products for acute care treatments and peritoneal dialysis products. Operating income in the EMEA segment increased by 4% to $139 million in the second quarter, due to favorable foreign exchange effects and a positive impact from manufacturing driven by higher volumes and production efficiencies. The operating income margin increased to 20.6% (+50 basis points).

For the first half of 2016, EMEA revenue increased by 1% to $1,307 million and operating income decreased by 2% to $269 million.

Asia-Pacific revenue grew by 5% (+6% at constant currency) to $397 million in the second quarter. The region recorded $177 million in health care services revenue, based on an increase of 4% in dialysis treatments. With a 4% growth in revenue to $220 million (+9% at constant currency), the product business showed a very good sales performance across the entire dialysis products range. Operating income showed a strong increase (+12%) to $75 million. The operating income margin increased to 18.9% (+110 basis points). This was driven by favorable foreign currency effects and the positive underlying business performance, in particular in China and India.

For the first half of 2016, Asia-Pacific revenue grew by 6% to $771 million (+8% at constant currency) and operating income decreased by 8% to $140 million.

Latin America delivered revenue of $175 million, a decrease of 14% and an improvement of 9% at constant currency. Health care services revenue decreased by 17% to $125 million (+9% at constant currency) as a result of negative foreign currency effects and the effect of closed or sold clinics (mainly in Venezuela). Dialysis treatments decreased accordingly by 7% in the second quarter. This was partially offset by the strong organic revenue growth of 19%. Dialysis products revenue decreased by 5% to $50 million (+8% at constant currency). The 8% increase at constant curreny was driven by higher sales of dialyzers, hemodialysis solutions and concentrates, machines and bloodlines, partially offset by lower sales of peritoneal dialysis products. Operating income came in at $16 million (+4%) with the operating margin increasing to 9.3%. The margin increase was primarily driven by favorable foreign exchange effects.

For the first half of 2016, Latin America revenue decreased by 18% to $328 million (+7% at constant currency) and operating income decreased by 19% to $27 million.

Cash flow

In the second quarter of 2016, the company generated $678 million in net cash provided by operating activities, representing 15.3% of revenue ($385 million in Q2 2015). The strong increase was primarily driven by an adjustment during the first quarter which impacted invoicing and was largely resolved during the second quarter. In addition, the timing of working capital items and higher earnings had a positive effect on cash flow. These effects were partially offset by higher income tax payments. The number of DSO (days sales outstanding) came in at 70 days, a reduction of 4 days compared to the first quarter of 2016.

In the first half of 2016, the company generated net cash provided by operating activities of $857 million, representing 9.9% of revenue.

Employees

As of June 30, 2016, Fresenius Medical Care had 106,556 employees (full-time equivalents) worldwide, compared to 102,893 employees at the end of June 2015. This increase was attributable to our continued organic growth.

Recent events: 6008 CAREsystem

In May 2016, Fresenius Medical Care launched the 6008 CAREsystem, a new innovative hemodialysis therapy system enabling better care for chronic patients. To enable significantly reduced complexity in therapy delivery, the system uses a new, all-in-one disposable with completely pre-connected bloodlines for all treatment modalities. More than 150,000 treatments have already been performed with the system.

Outlook 2016 confirmed

Based on the positive business development in the first half of 2016, Fresenius Medical Care confirms its full year outlook 2016. The company expects a currency-adjusted revenue growth between +7% and +10% for 2016. Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA is expected to increase by +15% to +20% over the previous year.

Conference call

Fresenius Medical Care will hold a conference call to discuss the results of the second quarter/first half 2016 on Tuesday, August 2, 2016 at 3.30 p.m. CEDT/ 9.30 a.m. EDT. The company invites investors to follow the live webcast of the call at the company’s website www.freseniusmedicalcare.com in the “Investors/Events” section. A replay will be available shortly after the call.

Please refer to the attachments for a complete overview of the results for the second quarter and first half of 2016.

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases of which about 2.8 million patients worldwide regularly undergo dialysis treatment. Through its network of 3,504 dialysis clinics, Fresenius Medical Care provides dialysis treatments for 301,548 patients around the globe. Fresenius Medical Care is also the leading provider of dialysis products such as dialysis machines or dialyzers. Along with the core business, the company focuses on expanding the range of related medical services in the field of Care Coordination. Fresenius Medical Care is listed on the Frankfurt Stock Exchange (FME) and on the New York Stock Exchange (FMS).

For more information visit the Company’s website at www.freseniusmedicalcare.com.

Disclaimer

This release contains forward-looking statements that are subject to various risks and uncertainties. Actual results could differ materially from those described in these forward-looking statements due to certain factors, including changes in business, economic and competitive conditions, regulatory reforms, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. These and other risks and uncertainties are detailed in Fresenius Medical Care AG & Co. KGaA's reports filed with the U.S. Securities and Exchange Commission. Fresenius Medical Care AG & Co. KGaA does not undertake any responsibility to update the forward-looking statements in this release.

If no timeframe is specified, information refers to H1/2016

Q2/2016:

- Sales: €7.1 billion (+2%, +5% in constant currency)

- EBIT1: €1,051 million (+8%, +11% in constant currency)

- Net income1,2: €393 million (+12%, +15% in constant currency)

H1/2016:

- Sales: €14.0 billion (+4%, +6% in constant currency)

- EBIT1: €2,010 million (+10%, +11% in constant currency)

- Net income1,2: €755 million (+18%, +18% in constant currency)

1 2015 before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 13-14 of the pdf file.

Stephan Sturm, CEO of Fresenius, said: “Once again, all four business segments contributed to strong organic growth. This confirms Fresenius’ sound strategic position as a healthcare Group. We have continued to grow even in regions where economies have slowed. This confirms the stability of our markets and businesses. Even compared with an excellent prior-year quarter, Fresenius has again achieved double-digit earnings growth. This confirms that we are providing the right products and services to patients worldwide. Fresenius has now delivered the 50th consecutive quarter of earnings growth. We continue to look forward with great confidence, and are raising our 2016 earnings guidance.”

2016 Group earnings guidance raised

Based on the Group’s excellent financial results in the first half of 2016 and strong prospects for the remainder of the year, Fresenius raises its 2016 Group earnings guidance. Net income1,2 is now expected to grow by 11% to 14% in constant currency. Previously, Fresenius expected net income1,2 growth of 8% to 12% in constant currency. The company confirms its Group sales guidance. Sales are expected to increase by 6% to 8% in constant currency.

The net debt/EBITDA3 ratio is expected to be approximately 2.5 at the end of 2016.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 2015 before special items

3 Calculated at FY average exchange rates for both net debt and EBITDA; excluding potential acquisitions

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

6% sales growth in constant currency

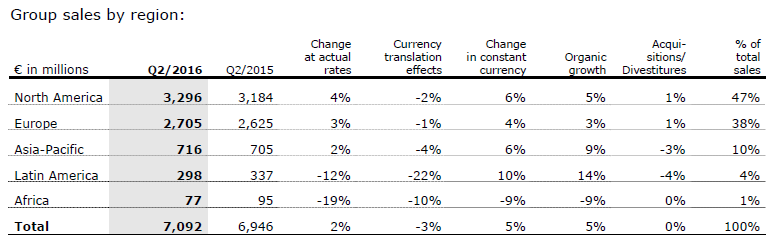

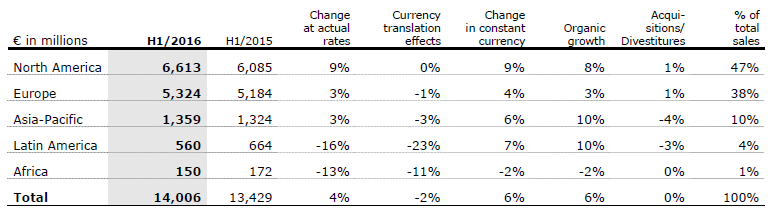

Group sales increased by 4% (6% in constant currency) to €14,006 million (H1/2015: €13,429 million). Organic sales growth was 6%. Acquisitions contributed 1% and divestitures reduced sales by 1%. Negative currency translation effects (-2%) were mainly driven by the devaluation of Latin American currencies against the Euro. In Q2/2016, Group sales increased by 2% (5% in constant currency) to €7,092 million (Q2/2015: €6,946 million). Organic sales growth was 5%. Acquisitions contributed 1%, while divestitures reduced sales by 1%.

Group sales by region:

18% net income1,2 growth in constant currency

Group EBITDA2 increased by 9% (10% in constant currency) to €2,576 million (H1/2015: €2,364 million). Group EBIT2 increased by 10% (11% in constant currency) to €2,010 million (H1/2015: €1,822 million). The EBIT margin2 increased to 14.4% (H1/2015: 13.6%). In Q2/2016, Group EBIT2 increased by 8% (11% in constant currency) to €1,051 million (Q2/2015: €971 million), the EBIT margin was 14.8% (Q2/2015: 14.0%).

Group net interest decreased to -€291 million (H1/2015: -€330 million), mainly due to more favorable financing terms and lower net debt.

With 28.6%, the Group tax rate (before special items) was on Q1/2016 level (28.4%) and hence in line with expectations. In Q2/2016, the Group tax rate was 28.7% (Q2/2015: 29.0%).

Noncontrolling interest increased to €473 million (H1/2015: €409 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income , increased by 18% (18% in constant currency) to €755 million (H1/2015: €642 million). Earnings per share1,2 increased by 17% (18% in constant currency) to €1.38 (H1/2015: €1.18). In Q2/2016, Group net income1,2 increased by 12% (15% in constant currency) to €393 million (Q2/2015: €350 million). Earnings per share1,2 increased by 12% (14% in constant currency) to €0.72 (Q2/2015: €0.64).

Continued investment in growth

Spending on property, plant and equipment was €670 million (H1/2015: €611 million), primarily for the modernization and expansion of dialysis clinics, production facilities and hospitals. Total acquisition spending was €505 million (H1/2015: €194 million).

Cash flow development

Operating cash flow increased by 6% to €1,330 million (H1/2015: €1,251 million) with a margin of 9.5% (H1/2015: 9.3%). Operating cash flow in Q2/2016 increased to €996 million (Q2/2015: €720 million). The cash flow margin increased to 14.0% (Q2/2015: 10.4%). As expected, the operating cashflow of Fresenius Medical Care improved considerably in Q2/2016.

Free cash flow before acquisitions and dividends increased slightly to €650 million (H1/2015: €646 million). Free cash flow after acquisitions and dividends was -€206 million (H1/2015: €107 million).

Solid balance sheet structure

The Group’s total assets increased by 2% (3% in constant currency) to €43,821 million (Dec. 31, 2015: €42,959 million). The increase is mainly driven by business expansion. Current assets grew by 5% (6% in constant currency) to €11,000 million (Dec. 31, 2015: €10,479 million). Non-current assets increased by 1% (2% in constant currency) to €32,821 million (Dec. 31, 2015: € 32,480 million).

Total shareholders’ equity grew by 3% (also 3% in constant currency) to €18,458 million (Dec. 31, 2015: €18,003 million). The equity ratio increased to 42.1% (Dec. 31, 2015: 41.9%).

Group debt increased by 1% (2% in constant currency) to €14,960 million (Dec. 31, 2015: € 14,769 million). As of June 30, 2016, the net debt/EBITDA ratio was 2.62 , (Dec. 31, 2015: 2.681).

12015 before special items; at LTM average exchange rates for both net debt and EBITDA

2Pro forma acquisitions

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

Increased number of employees

As of June 30, 2016, the number of employees increased by 2% to 227,856 (Dec. 31, 2015: 222,305).

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of June 30, 2016, Fresenius Medical Care was treating 301,548 patients in 3,504 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

- 7% sales growth in constant currency in Q2

- 22% net income growth in Q2

- 2016 outlook confirmed

Sales increased by 6% (8% in constant currency) to US$8,626 million (H1/2015: US$8,159 million). Organic sales growth was 7%. Acquisitions contributed 1%. Currency translation effects reduced sales by 2%. In Q2/2016, sales increased by 5% (7% in constant currency) to US$4,420 million (Q2/2015: US$4,199 million). Organic sales growth was 6%.

Health Care services sales (dialysis services and care coordination) increased by 7% (9% in constant currency) to US$6,985 million (H1/2015: US$6,527 million). Dialysis product sales increased by 1% (4% in constant currency) to US$1,640 million (H1/2015: US$1,631 million).

In North America, sales increased by 9% to US$6,212 million (H1/2015: US$5,717 million). Health Care services sales grew by 9% to US$5,770 million (H1/2015: US$5,293 million). Dialysis product sales increased by 4% to US$441 million (H1/2015: US$424 million).

Sales outside North America decreased by 1% (increased by 6% in constant currency) to US$2,406 million (H1/2015: US$2,427 million). Health Care services sales decreased by 2% (increased by 7% in constant currency) to US$1,215 million (H1/2015: US$1,234 million). Dialysis product sales remained nearly unchanged at (increased by 5% in constant currency to) US$1,191 million (H1/2015: US$1,193 million).

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

EBIT increased by 12% (13% in constant currency) to US$1,181 million (H1/2015: US$1,051 million). The EBIT margin was 13.7% (H1/2015: 12.9%). In Q2/2016, EBIT increased by 17% (17% in constant currency) to US$641 million (Q2/2015: US$547 million). The EBIT margin was 14.5% (Q2/2015: 13.0%).

Net income increased by 16% (16% in constant currency) to US$522 million (H1/2015: US$450 million). In Q2/2016, net income grew by 22% (22% in constant currency) to US$294 million (Q2/2015: US$241 million).

Operating cash flow increased by 3% to US$857 million (H1/2015: US$832 million). The cash flow margin was 9.9% (H1/2015: 10.2%). In Q2/2016, operating cash flow increased to US$678 million (Q2/2015: US$385 million) with a cash flow margin of 15.3% (Q2/2015: 9.2%). The sequential improvement is mainly driven by the anticipated catch-up effect after the adjustment in invoicing in Q1/2016.

Fresenius Medical Care confirms its outlook for 2016. The company expects sales to grow by 7% to 10% in constant currency and net income1 is expected to increase by 15% to 20% in 2016.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 2015 before GranuFlo®/NaturaLyte® settlement costs (-US$37 million after tax) and before acquisitions (US$9 million after tax); hence the basis for expected net income growth is US$1,057 million.

For further information, please see Fresenius Medical Care’s Press Release at www.freseniusmedicalcare.com.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

- 3% organic sales growth in Q2

- 1% constant currency EBIT1 growth in Q2

- 2016 outlook raised: both, organic sales growth and EBIT1 growth in constant currency of 3% to 5% expected

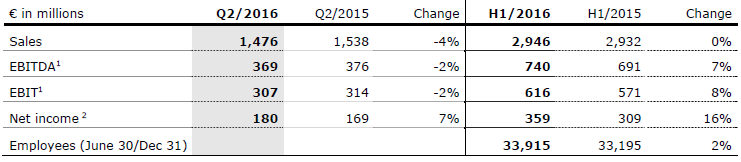

Sales increased slightly (by 4% in constant currency) to €2,946 million (H1/2015: €2,932 million). Organic sales growth was 6%. Divestitures reduced sales by 2%. In Q2/2016, sales decreased by 4% (increased by 1% in constant currency) to €1,476 million (Q2/2015: €1,538 million). Negative currency translation effects (-5%) were mainly driven by the devaluation of the Chinese yuan, the U.S. dollar and the Argentine peso against the Euro. Organic sales growth was 3%.

Sales in Europe remained nearly unchanged at €1,048 million (H1/2015: €1,052 million). Organic sales growth was 2%. Divestitures reduced sales by 1%. Also in Q2/2016, sales were almost unchanged at €536 million (Q2/2015: €534 million). Organic sales growth was 2%.

Sales in North America increased by 6% (organic growth: 6%) to €1,086 million (H1/2015: €1,026 million), driven by persisting drug shortages as well as new product launches in Q1/2016. In Q2/2016, sales decreased by 8% (organic: 6%) to €510 million (Q2/2015: €553 million), mainly due to the high prior-year basis driven by significant new product launches.

1 2015 before special items

2 Net income attributable to shareholders of Fresenius Kabi AG; 2015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14.

Sales in Asia-Pacific decreased by 6% (organic growth: 7%) to €531 million (H1/2015: €564 million). Adverse currency translation effects reduced sales by 5%, divestitures by another 8%. In Q2/2016, sales decreased by 6% (organic growth: 8%) to €277 million (Q2/2015: €296 million).

Given adverse currency translation effects, sales in Latin America/Africa decreased by 3% (organic growth: 21%, in particular due to inflation driven price increases) to €281 million (H1/2015: €290 million). In Q2/2016, sales decreased by 1% (organic growth 22%) to €153 million (Q2/2015: €155 million).

EBIT2 increased by 8% (10% in constant currency) to €616 million (H1/2015: €571 million). The EBIT margin2 improved to 20.9% (H1/2015: 19.5%). In Q2/2016, EBIT2 decreased by 2% (increased by 1% in constant currency) to €307 million (Q2/2015: €314 million). The EBIT margin2 increased to 20.8% (Q2/2015: 20.4%).

Net income1 increased by 16% (37% in constant currency) to €359 million (H1/2015: €309 million). In Q2/2016, net income1 increased by 7% (30% in constant currency) to €180 million (Q2/2015: €169 million).

Given adverse currency translation effects, operating cash flow decreased by 5% to €335 million (H1/2015: €354 million) with a margin of 11.4% (H1/2015: 12.1%). While operating cash flow reached a very strong €211 million in Q2/2016, it could not match the exceptional prior-year quarter (Q2/2015: €271 million). The same applies to the margin of 14.3% (Q2/2015: 17.6%).

Fresenius Kabi raises its outlook for 2016 and now expects organic sales growth of 3% to 5% and EBIT2 growth in constant currency of 3% to 5%. Previously, Fresenius Kabi projected low single-digit organic sales growth and EBIT2 in constant currency to be roughly flat compared with 2015.

1 Net income attributable to shareholders of Fresenius Kabi AG; 2015 before special items

2 2015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

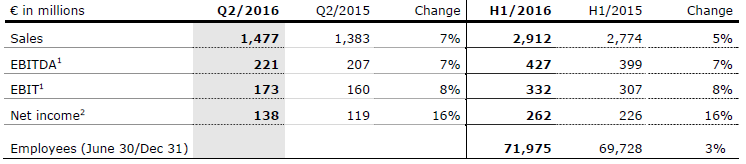

Fresenius Helios

Fresenius Helios is Germany’s largest hospital operator. HELIOS operates 112 hospitals, thereof 88 acute care clinics (including seven maximum care hospitals in Berlin-Buch, Duisburg, Erfurt, Krefeld, Schwerin, Wiesbaden and Wuppertal) and 24 post-acute care clinics. HELIOS treats more than 4.7 million patients per year, thereof approximately 1.3 million inpatients, and operates more than 34,000 beds.

- 6% organic sales growth in Q2

- 60 bps sequential EBIT margin increase

- 2016 outlook confirmed

Sales increased by 5% to €2,912 million (H1/2015: €2,774 million). Organic sales growth was 4% (H1/2015: 3%). Acquisitions and divestitures had no material effect. In Q2/2016, sales increased by 7% to €1,477 million (Q2/2015: €1,383 million). Organic sales growth was 6% (Q2/2015: 2%).

EBIT1 grew by 8% to €332 million (H1/2015: €307 million). The EBIT margin1 increased to 11.4% (H1/2015: 11.1%). In Q2/2016, EBIT1 increased by 8% to €173 million (Q2/2015: €160 million). Sequentially, the EBIT margin increased by 60 bps to 11.7%.

Net income2 increased by 16% to €262 million (H1/2015: €226 million). In Q2/2016, net income2 increased by 16% to €138 million (Q2/2015: €119 million).

Fresenius Helios confirms its outlook for 2016 and projects organic sales growth of 3% to 5%. EBIT is expected to increase to €670 to €700 million.

1 2015 before special items

2 Net income attributable to shareholders of HELIOS Kliniken GmbH; 2015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

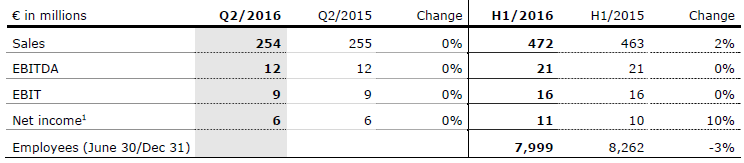

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

- Sales development reflects typical quarterly fluctuations in the project business

- Strong order intake of €228 million in Q2

- 2016 outlook confirmed

Sales increased by 2% (2% in constant currency) to €472 million (H1/2015: €463 million). Organic sales growth was 3%. Sales in the project business decreased by 3% to €195 million (H1/2015: €202 million). Sales in the service business grew by 6% to €277 million (H1/2015: €261 million). In Q2/2016, sales remained nearly unchanged at €254 million (Q2/2015: €255 million). Organic sales growth was 1%.

EBIT remained unchanged at €16 million (H1/2015: €16 million). The EBIT margin was 3.4% (H1/2015: 3.5%). In Q2/2016, EBIT remained unchanged at €9 million (Q2/2015: €9 million). The EBIT margin of 3.5% was at prior-year level.

Net income1 grew by 10% to €11 million (H1/2015: €10 million). In Q2/2016, net income1 of €6 million was at prior-year level.

Order intake increased by 64% to €465 million (H1/2015: €284 million). As of June 30, 2016, order backlog grew to €1,917 million (December 31, 2015: €1,650 million).

Fresenius Vamed confirms its outlook for 2016 and expects organic sales growth in the range of 5% to 10% and EBIT growth of 5% to 10%.

1 Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for the first half of 2016, a conference call for analysts and investors will be held on August 2, 2016 at 2 p.m. CEDT (8 a.m. EDT). You are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/media. Following the call, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

If no timeframe is specified, information refers to H1/2016

Q2/2016:

- Sales: €7.1 billion (+2%, +5% in constant currency)

- EBIT1: €1,051 million (+8%, +11% in constant currency)

- Net income1,2: €393 million (+12%, +15% in constant currency)

H1/2016:

- Sales: €14.0 billion (+4%, +6% in constant currency)

- EBIT1: €2,010 million (+10%, +11% in constant currency)

- Net income1,2: €755 million (+18%, +18% in constant currency)

12015 before special items2Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation tables on pages 13-14 of the pdf file.

Stephan Sturm, CEO of Fresenius, said: “Once again, all four business segments contributed to strong organic growth. This confirms Fresenius’ sound strategic position as a healthcare Group. We have continued to grow even in regions where economies have slowed. This confirms the stability of our markets and businesses. Even compared with an excellent prior-year quarter, Fresenius has again achieved double-digit earnings growth. This confirms that we are providing the right products and services to patients worldwide. Fresenius has now delivered the 50th consecutive quarter of earnings growth. We continue to look forward with great confidence, and are raising our 2016 earnings guidance.”

2016 Group earnings guidance raised

Based on the Group’s excellent financial results in the first half of 2016 and strong prospects for the remainder of the year, Fresenius raises its 2016 Group earnings guidance. Net income1,2 is now expected to grow by 11% to 14% in constant currency. Previously, Fresenius expected net income1,2 growth of 8% to 12% in constant currency. The company confirms its Group sales guidance. Sales are expected to increase by 6% to 8% in constant currency.

The net debt/EBITDA3 ratio is expected to be approximately 2.5 at the end of 2016.

1Net income attributable to shareholders of Fresenius SE & Co. KGaA22015 before special items3Calculated at FY average exchange rates for both net debt and EBITDA; excluding potential acquisitions

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

6% sales growth in constant currency

Group sales increased by 4% (6% in constant currency) to €14,006 million (H1/2015: €13,429 million). Organic sales growth was 6%. Acquisitions contributed 1% and divestitures reduced sales by 1%. Negative currency translation effects (-2%) were mainly driven by the devaluation of Latin American currencies against the Euro. In Q2/2016, Group sales increased by 2% (5% in constant currency) to €7,092 million (Q2/2015: €6,946 million). Organic sales growth was 5%. Acquisitions contributed 1%, while divestitures reduced sales by 1%.

18% net income1,2 growth in constant currency

Group EBITDA2 increased by 9% (10% in constant currency) to €2,576 million (H1/2015: €2,364 million). Group EBIT2 increased by 10% (11% in constant currency) to €2,010 million (H1/2015: €1,822 million). The EBIT margin2 increased to 14.4% (H1/2015: 13.6%). In Q2/2016, Group EBIT2 increased by 8% (11% in constant currency) to €1,051 million (Q2/2015: €971 million), the EBIT margin was 14.8% (Q2/2015: 14.0%).

Group net interest decreased to -€291 million (H1/2015: -€330 million), mainly due to more favorable financing terms and lower net debt.

With 28.6%, the Group tax rate (before special items) was on Q1/2016 level (28.4%) and hence in line with expectations. In Q2/2016, the Group tax rate was 28.7% (Q2/2015: 29.0%).

Noncontrolling interest increased to €473 million (H1/2015: €409 million), of which 96% was attributable to the noncontrolling interest in Fresenius Medical Care.

Group net income , increased by 18% (18% in constant currency) to €755 million (H1/2015: €642 million). Earnings per share1,2 increased by 17% (18% in constant currency) to €1.38 (H1/2015: €1.18). In Q2/2016, Group net income1,2 increased by 12% (15% in constant currency) to €393 million (Q2/2015: €350 million). Earnings per share1,2 increased by 12% (14% in constant currency) to €0.72 (Q2/2015: €0.64).

Continued investment in growth

Spending on property, plant and equipment was €670 million (H1/2015: €611 million), primarily for the modernization and expansion of dialysis clinics, production facilities and hospitals. Total acquisition spending was €505 million (H1/2015: €194 million).

Cash flow development

Operating cash flow increased by 6% to €1,330 million (H1/2015: €1,251 million) with a margin of 9.5% (H1/2015: 9.3%). Operating cash flow in Q2/2016 increased to €996 million (Q2/2015: €720 million). The cash flow margin increased to 14.0% (Q2/2015: 10.4%). As expected, the operating cashflow of Fresenius Medical Care improved considerably in Q2/2016.

Free cash flow before acquisitions and dividends increased slightly to €650 million (H1/2015: €646 million). Free cash flow after acquisitions and dividends was -€206 million (H1/2015: €107 million).

Solid balance sheet structure

The Group’s total assets increased by 2% (3% in constant currency) to €43,821 million (Dec. 31, 2015: €42,959 million). The increase is mainly driven by business expansion. Current assets grew by 5% (6% in constant currency) to €11,000 million (Dec. 31, 2015: €10,479 million). Non-current assets increased by 1% (2% in constant currency) to €32,821 million (Dec. 31, 2015: € 32,480 million).

Total shareholders’ equity grew by 3% (also 3% in constant currency) to €18,458 million (Dec. 31, 2015: €18,003 million). The equity ratio increased to 42.1% (Dec. 31, 2015: 41.9%).

Group debt increased by 1% (2% in constant currency) to €14,960 million (Dec. 31, 2015: € 14,769 million). As of June 30, 2016, the net debt/EBITDA ratio was 2.62 , (Dec. 31, 2015: 2.681).

12015 before special items; at LTM average exchange rates for both net debt and EBITDA2Pro forma acquisitionsFor a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of June 30, 2016, Fresenius Medical Care was treating 301,548 patients in 3,504 dialysis clinics. Along with its core business, the company seeks to expand the range of medical services in the field of care coordination.

- 7% sales growth in constant currency in Q2

- 22% net income growth in Q2

- 2016 outlook confirmed

Sales increased by 6% (8% in constant currency) to US$8,626 million (H1/2015: US$8,159 million). Organic sales growth was 7%. Acquisitions contributed 1%. Currency translation effects reduced sales by 2%. In Q2/2016, sales increased by 5% (7% in constant currency) to US$4,420 million (Q2/2015: US$4,199 million). Organic sales growth was 6%.

Health Care services sales (dialysis services and care coordination) increased by 7% (9% in constant currency) to US$6,985 million (H1/2015: US$6,527 million). Dialysis product sales increased by 1% (4% in constant currency) to US$1,640 million (H1/2015: US$1,631 million).

In North America, sales increased by 9% to US$6,212 million (H1/2015: US$5,717 million). Health Care services sales grew by 9% to US$5,770 million (H1/2015: US$5,293 million). Dialysis product sales increased by 4% to US$441 million (H1/2015: US$424 million).

Sales outside North America decreased by 1% (increased by 6% in constant currency) to US$2,406 million (H1/2015: US$2,427 million). Health Care services sales decreased by 2% (increased by 7% in constant currency) to US$1,215 million (H1/2015: US$1,234 million). Dialysis product sales remained nearly unchanged at (increased by 5% in constant currency to) US$1,191 million (H1/2015: US$1,193 million).

1Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

EBIT increased by 12% (13% in constant currency) to US$1,181 million (H1/2015: US$1,051 million). The EBIT margin was 13.7% (H1/2015: 12.9%). In Q2/2016, EBIT increased by 17% (17% in constant currency) to US$641 million (Q2/2015: US$547 million). The EBIT margin was 14.5% (Q2/2015: 13.0%).

Net income increased by 16% (16% in constant currency) to US$522 million (H1/2015: US$450 million). In Q2/2016, net income grew by 22% (22% in constant currency) to US$294 million (Q2/2015: US$241 million).

Operating cash flow increased by 3% to US$857 million (H1/2015: US$832 million). The cash flow margin was 9.9% (H1/2015: 10.2%). In Q2/2016, operating cash flow increased to US$678 million (Q2/2015: US$385 million) with a cash flow margin of 15.3% (Q2/2015: 9.2%). The sequential improvement is mainly driven by the anticipated catch-up effect after the adjustment in invoicing in Q1/2016.

Fresenius Medical Care confirms its outlook for 2016. The company expects sales to grow by 7% to 10% in constant currency and net income1 is expected to increase by 15% to 20% in 2016.

1Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

22015 before GranuFlo®/NaturaLyte® settlement costs (-US$37 million after tax) and before acquisitions (US$9 million after tax); hence the basis for expected net income growth is US$1,057 million.

For further information, please see Fresenius Medical Care’s Press Release at www.freseniusmedicalcare.com.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products.

- 3% organic sales growth in Q2

- 1% constant currency EBIT1 growth in Q2

- 2016 outlook raised: both, organic sales growth and EBIT1 growth in constant currency of 3% to 5% expected

Sales increased slightly (by 4% in constant currency) to €2,946 million (H1/2015: €2,932 million). Organic sales growth was 6%. Divestitures reduced sales by 2%. In Q2/2016, sales decreased by 4% (increased by 1% in constant currency) to €1,476 million (Q2/2015: €1,538 million). Negative currency translation effects (-5%) were mainly driven by the devaluation of the Chinese yuan, the U.S. dollar and the Argentine peso against the Euro. Organic sales growth was 3%.

Sales in Europe remained nearly unchanged at €1,048 million (H1/2015: €1,052 million). Organic sales growth was 2%. Divestitures reduced sales by 1%. Also in Q2/2016, sales were almost unchanged at €536 million (Q2/2015: €534 million). Organic sales growth was 2%.

Sales in North America increased by 6% (organic growth: 6%) to €1,086 million (H1/2015: €1,026 million), driven by persisting drug shortages as well as new product launches in Q1/2016. In Q2/2016, sales decreased by 8% (organic: 6%) to €510 million (Q2/2015: €553 million), mainly due to the high prior-year basis driven by significant new product launches.

12015 before special items2Net income attributable to shareholders of Fresenius Kabi AG; 2015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14.

Sales in Asia-Pacific decreased by 6% (organic growth: 7%) to €531 million (H1/2015: €564 million). Adverse currency translation effects reduced sales by 5%, divestitures by another 8%. In Q2/2016, sales decreased by 6% (organic growth: 8%) to €277 million (Q2/2015: €296 million).

Given adverse currency translation effects, sales in Latin America/Africa decreased by 3% (organic growth: 21%, in particular due to inflation driven price increases) to €281 million (H1/2015: €290 million). In Q2/2016, sales decreased by 1% (organic growth 22%) to €153 million (Q2/2015: €155 million).

EBIT2 increased by 8% (10% in constant currency) to €616 million (H1/2015: €571 million). The EBIT margin2 improved to 20.9% (H1/2015: 19.5%). In Q2/2016, EBIT2 decreased by 2% (increased by 1% in constant currency) to €307 million (Q2/2015: €314 million). The EBIT margin2 increased to 20.8% (Q2/2015: 20.4%).

Net income1 increased by 16% (37% in constant currency) to €359 million (H1/2015: €309 million). In Q2/2016, net income1 increased by 7% (30% in constant currency) to €180 million (Q2/2015: €169 million).

Given adverse currency translation effects, operating cash flow decreased by 5% to €335 million (H1/2015: €354 million) with a margin of 11.4% (H1/2015: 12.1%). While operating cash flow reached a very strong €211 million in Q2/2016, it could not match the exceptional prior-year quarter (Q2/2015: €271 million). The same applies to the margin of 14.3% (Q2/2015: 17.6%).

Fresenius Kabi raises its outlook for 2016 and now expects organic sales growth of 3% to 5% and EBIT2 growth in constant currency of 3% to 5%. Previously, Fresenius Kabi projected low single-digit organic sales growth and EBIT2 in constant currency to be roughly flat compared with 2015.

1Net income attributable to shareholders of Fresenius Kabi AG; 2015 before special items22015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

Fresenius Helios

Fresenius Helios is Germany’s largest hospital operator. HELIOS operates 112 hospitals, thereof 88 acute care clinics (including seven maximum care hospitals in Berlin-Buch, Duisburg, Erfurt, Krefeld, Schwerin, Wiesbaden and Wuppertal) and 24 post-acute care clinics. HELIOS treats more than 4.7 million patients per year, thereof approximately 1.3 million inpatients, and operates more than 34,000 beds.

- 6% organic sales growth in Q2

- 60 bps sequential EBIT margin increase

- 2016 outlook confirmed

Sales increased by 5% to €2,912 million (H1/2015: €2,774 million). Organic sales growth was 4% (H1/2015: 3%). Acquisitions and divestitures had no material effect. In Q2/2016, sales increased by 7% to €1,477 million (Q2/2015: €1,383 million). Organic sales growth was 6% (Q2/2015: 2%).

EBIT1 grew by 8% to €332 million (H1/2015: €307 million). The EBIT margin1 increased to 11.4% (H1/2015: 11.1%). In Q2/2016, EBIT1 increased by 8% to €173 million (Q2/2015: €160 million). Sequentially, the EBIT margin increased by 60 bps to 11.7%.

Net income2 increased by 16% to €262 million (H1/2015: €226 million). In Q2/2016, net income2 increased by 16% to €138 million (Q2/2015: €119 million).

Fresenius Helios confirms its outlook for 2016 and projects organic sales growth of 3% to 5%. EBIT is expected to increase to €670 to €700 million.

12015 before special items2Net income attributable to shareholders of HELIOS Kliniken GmbH; 2015 before special items

For a detailed overview of special items please see the reconciliation tables on page 13-14 of the pdf file.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management, to total operational management.

- Sales development reflects typical quarterly fluctuations in the project business

- Strong order intake of €228 million in Q2

- 2016 outlook confirmed

Sales increased by 2% (2% in constant currency) to €472 million (H1/2015: €463 million). Organic sales growth was 3%. Sales in the project business decreased by 3% to €195 million (H1/2015: €202 million). Sales in the service business grew by 6% to €277 million (H1/2015: €261 million). In Q2/2016, sales remained nearly unchanged at €254 million (Q2/2015: €255 million). Organic sales growth was 1%.

EBIT remained unchanged at €16 million (H1/2015: €16 million). The EBIT margin was 3.4% (H1/2015: 3.5%). In Q2/2016, EBIT remained unchanged at €9 million (Q2/2015: €9 million). The EBIT margin of 3.5% was at prior-year level.

Net income1 grew by 10% to €11 million (H1/2015: €10 million). In Q2/2016, net income1 of €6 million was at prior-year level.

Order intake increased by 64% to €465 million (H1/2015: €284 million). As of June 30, 2016, order backlog grew to €1,917 million (December 31, 2015: €1,650 million).

Fresenius Vamed confirms its outlook for 2016 and expects organic sales growth in the range of 5% to 10% and EBIT growth of 5% to 10%.

1Net income attributable to shareholders of VAMED AG

Conference Call

As part of the publication of the results for the first half of 2016, a conference call will be held on August 2, 2016 at 2 p.m. CEDT (8 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to pages 25, 40, 56f., 100f. and 194 of the Annual Report 2015 of Fresenius SE & Co. KGaA. Constant currencies for income and expenses are calculated using prior year average rates; constant currencies for assets and liabilities are calculated using the mid-closing rate on the date of the respective statement of financial position (cf. Annual Report 2015, page 111). (https://www.fresenius.com/financial_reporting/Fresenius_GB_US_GAAP_2015_englisch.pdf).

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.

The “Wir für Gesundheit” hospital network in Germany continues to grow: PlusCard, a supplementary company health insurance, will be accepted starting immediately at Klinikum Ingolstadt. With more than 1,000 beds, this hospital is one of the largest in the state of Bavaria. PlusCard offers employers various coverage options to provide employees with different levels of service and comfort. “Wir für Gesundheit” was formed by hospital operators Asklepios, Fresenius Helios and Rhön, and has more than 120 partner hospitals in Germany committed to comply with quality standards far higher than those required by law.

Fitch has upgraded the corporate credit rating of Fresenius from BB+ to BBB- with a stable outlook. The upgrade reflects Fitch's view that Fresenius' business profile has improved over the last years driven by increasing scale and diversification as well as strong profitability and cash generation. In addition, Fitch considers the underlying operations to be mature and defensive with low cyclicality and low volatility of earnings. Standard & Poor’s and Moody’s have upgraded the corporate credit rating of Fresenius to investment grade in 2015.

Fresenius Helios has celebrated the official groundbreaking for a new main building at HELIOS Hospital Dr. Horst Schmidt Kliniken in the German city of Wiesbaden. HELIOS is providing almost €200 million of the approximately €265 million total investment, with the rest coming from the state of Hesse. The seven-story structure will have some 96,000 square meters – about 1 million square feet – of floor space. The departments will be arranged using a functional design concept that minimizes distances for patients and staff. This will reduce waiting times. Completion is scheduled for 2020.

September 19, 2016

London, UK

Barclays European High Yield and Leveraged Finance Conference

September 19 – 21, 2016

September 07, 2016

London, UK

Bank of America Merrill Lynch – European Credit Loans Conference

September 7 – 9, 2016

Fresenius Helios has opened the new building at its hospital in the northern German city of Schleswig. The 32,000-square-meter (344,000-square-foot) structure will accommodate up to 400 inpatients. Construction took two and a half years, with Fresenius Helios providing €30 million of the total investment sum of €80 million. The move from the existing facility into the new building will take place in mid-July.

The Supervisory Board of Fresenius Management SE has unanimously appointed Stephan Sturm (52) as Chief Executive Officer of Fresenius as of July 1, 2016. Stephan Sturm succeeds Ulf Mark Schneider (50), who has decided to leave the company effective June 30, 2016 to pursue another opportunity.

Ulf Mark Schneider assumed his current position as CEO of Fresenius on May 28, 2003. Under his leadership, the company has seen significant growth. Group sales have increased fourfold and net income rose more than twelvefold.

Gerd Krick, Chairman of Fresenius Management SE’s Supervisory Board, commented: “On behalf of the Supervisory Board I would like to thank Ulf Mark Schneider for his extraordinary leadership and tremendous accomplishments over the past 13 years. He has led Fresenius through a period of exciting and sustainable growth and has truly transformed the company. While we regret his departure we wish him the very best for his future endeavors.”

Stephan Sturm has served as Fresenius Group’s Chief Financial Officer since January 1, 2005. In this capacity he has made significant contributions to develop Fresenius into a leading global healthcare group. He has played a key role in major acquisitions. His innovative and highly successful financing activities facilitated the company’s strong and sustainable growth. Stephan Sturm has also assured the company’s overall efficiency and profitability during this major expansion.

Gerd Krick said: “We are delighted to appoint Stephan Sturm as our new CEO. The Supervisory Board could not have wished for a better qualified and experienced leader to succeed Ulf Mark Schneider in this role. Stephan Sturm has been a member of the Fresenius Management Board for more than 11 years. He has a highly successful track-record as the Group’s CFO and has made major contributions towards executing our successful growth strategy. The appointment of Stephan Sturm as the Fresenius Group’s new CEO demonstrates continuity at the helm of the company. He has the full support of the Supervisory Board and we look forward to working with him as we continue to grow our business.”

Stephan Sturm said: “I am approaching my new role with both excitement and respect. The future of Fresenius continues to look bright. I am fully committed to meeting our targets, executing on our growth strategy and contributing to affordable high-quality healthcare around the globe.”

Fresenius confirms its guidance for 2016. Sales are expected to increase by 6% to 8% in constant currency. Net income* is expected to grow by 8% to 12% in constant currency. The company also confirms its mid-term outlook: For 2019, Group sales are expected to reach €36 billion to €40 billion**. Group net income*** is expected to increase to €2.0 billion to €2.25 billion**.

* Net income attributable to shareholders of Fresenius SE & Co. KGaA; 2015 before special items

** At comparable exchange rates; including small and mid-size acquisitions

*** Net income attributable to shareholders of Fresenius SE & Co. KGaA

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.