February 20, 2019

Fresenius reports 15th consecutive record year – Significant investments into medium-term growth in FY/18 and FY/19 – Healthy medium-term growth targets

- Delivered on FY/18 Group targets

- Fresenius Kabi to show continued growth

- Helios Germany impacted by regulatory changes and initiatives to secure medium-term growth; Helios Spain to show continuous dynamic growth

- 26th consecutive dividend increase proposed

- Healthy growth targets for 2020 – 2023; consistent with expectations from December 2018

1 Growth rate adjusted for IFRS 15 adoption and divestitures of Care Coordination activities (Q4/17 base: €8,290 million; FY/17 base: €32,841 million)

2 Before special items and after adjustments

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 21-24 of the pdf file.

Group expectations for FY/19 confirmed

For FY/19, Fresenius projects sales growth1 of 3% to 6% in constant currency. Net income2,3 growth is expected to be ~0% in constant currency. NxStage is not included in this guidance because the acquisition is not closed yet and Fresenius does not expect a significant impact on its Group guidance metrics. This guidance is in line with the expectations announced on December 6, 2018.

Fresenius expects its year-end 2019 net debt/EBITDA4 ratio to be broadly stable over the year-end 2018 figure.

Fresenius intends to further increase its dividend for FY 2019.

Healthy growth targets5 for 2020 – 2023

Based on the expected financial results for FY/19, Group sales are projected to grow organically with a compounded annual growth rate (CAGR) of 4% to 7% in 2020 to 2023. Group net income2 is projected to increase organically with a CAGR of 5% to 9% in 2020 to 2023. Fresenius expects its launched and contemplated sales growth and efficiency improvement initiatives as well as the expected break-even of Fresenius Kabi’s biosimilars business to drive an acceleration of Group earnings growth over that period. Small and medium-sized acquisitions are expected to contribute an incremental CAGR of approx. 1%-point to both sales and net income growth.

1 FY/18 base: €33,009 million; FY/18 adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: adjusted for IFRS 16 effects; excluding effects from pending acquisition of NxStage by FMC

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/18 base: €1,872 million; FY/18 before special items and after adjustments; FY/19 before special items (transcation-related expenses, expenses associated with the cost optimization program at FMC, revaluations of biosimilars contingent liabilities); adjusted for IFRS 16 effects; excluding effects from pending acquisition of NxStage by FMC

4 Both net debt and EBITDA calculated at expected annual average exchange rates; excluding effects from pending acquisition of NxStage by FMC; excluding further potential acquisitions; adjusted for IFRS 16 effects

5 Before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 21-24 of the pdf file.

26th consecutive dividend increase proposed

Consistent with Fresenius’ stated dividend policy, the Management Board will propose to the Supervisory Board a 7% increase in the dividend for FY/18 to €0.80 per share (2017: €0.75). The proposed total dividend payout to Fresenius SE & Co. KGaA shareholders amounts to €445 million.

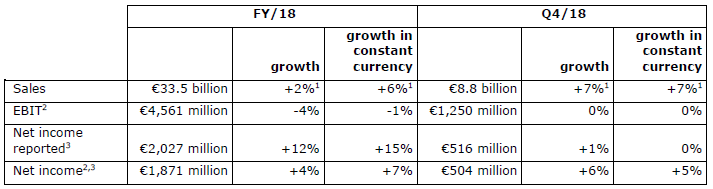

6% sales growth in constant currency1

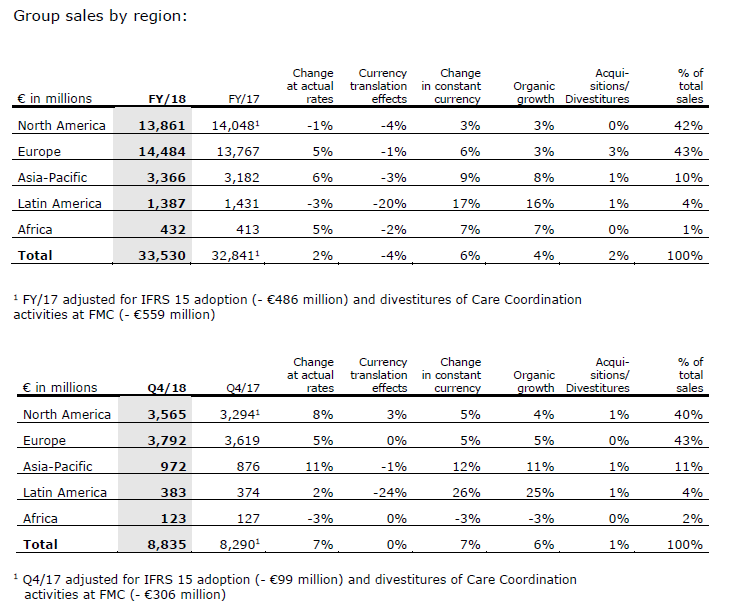

Group sales1 increased by 2%1 (6%1 in constant currency) to €33,530 million (FY/17: €32,841 million). Organic sales growth was 4%1. Acquisitions/divestitures contributed net 2%1 to growth. Negative currency translation effects of 4%1 were mainly driven by the devaluation of the U.S. dollar and the Argentinian peso against the euro.

In Q4/18, Group sales1 increased by 7%1 (7%1 in constant currency) to €8,835 million (Q4/17: €8,290 million). Organic sales1 growth was 6%1. Acquisitions/divestitures contributed net 1%1 to growth. There were no meaningful currency translation effects.

7% net income1,2 growth in constant currency

Group EBITDA2 decreased by 3%2 (0%2 in constant currency) to €5,991 million (FY/17: €6,174 million). Group EBIT2 decreased by 4%2 (-1%2 in constant currency) to €4,561 million (FY/17: €4,746 million). The EBIT margin2 was 13.6% (FY/17: 14.5%). Group EBIT2 before expenses for the further development of the biosimilars business decreased by 2%2 (increased by 1%2 in constant currency) to €4,727 million. In FY/17, the compensation for treatments of U.S. war veterans (“VA agreement”) had contributed €87 million as a one-time effect. Group EBIT2 excluding the VA agreement and expenses for the further development of the biosimilars business increased by 3% in constant currency.

In Q4/18, Group EBIT2 was broadly stable year-over-year2 (broadly stable2 in constant currency) at €1,250 million (Q4/17: €1,244 million), with an EBIT margin2 of 14.1% (Q4/17: 15.0%). Group EBIT2 excluding the prior-year VA agreement and expenses for the further development of the biosimilars business was also broadly stable year-over-year2 in constant currency.

Group net interest2 was -€570 million (FY/17: -€630 million). The decrease was mainly driven by refinancings at lower rates, lower debt, currency effects as well as proceeds from the divestitures of Care Coordination activities at Fresenius Medical Care.

The decrease of the Group tax rate2 to 22.0% (FY/17: 27.9%) was mainly due to the U.S. tax reform and some related one-time effects at Fresenius Medical Care and Fresenius Kabi. In Q4/18, the Group tax rate2 was 22.6% (Q4/17: 28.0%).

Noncontrolling interest2 was €1,240 million (2017: €1,164 million), of which 94% was attributable to the noncontrolling interest in Fresenius Medical Care.

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

2Before special items and after adjustments

Group net income1,2 increased by 12% (15% in constant currency) to €2,027 million (FY/17: €1,814 million), mainly due to gains related to divestitures of Care Coordination activities at Fresenius Medical Care. Earnings per share1,2 increased by 12% (15% in constant currency) to €3.65 (FY/17: €3.27). In Q4/18, Group net income1,2 increased by 1% (0% in constant currency) to €516 million (Q4/17: €511 million). Earnings per share1,2 increased by 1% (0% in constant currency) to €0.93 (Q4/17: €0.92).

Group net income1,3 before special items increased by 3% (6% in constant currency) to €1,871 million (FY/17: €1,816 million). Earnings per share1,3 increased by 3% (6% in constant currency) to €3.37 (FY/17: €3.28). In Q4/18, Group net income1,3 increased by 3% (3% in constant currency) to €504 million (Q4/17: €487 million). Earnings per share1,3 increased by 3% (3% in constant currency) to €0.91 (Q4/17: €0.88).

Group net income1,4 before special items and after adjustments increased by 4% (7% in constant currency) to €1,871 million (FY/17: €1,804 million). Earnings per share1,4 increased by 3% (6% in constant currency) to €3.37 (FY/17: €3.26). In Q4/18, Group net income1,4 increased by 6% (5% in constant currency) to €504 million (Q4/17: €477 million). Earnings per share1,4 increased by 6% (5% in constant currency) to €0.91 (Q4/17: €0.86).

Group net income1,4,5 before expenses for the further development of the biosimilars business increased by 8% (11% in constant currency) to €1,991 million (2017: €1,847 million). Earnings per share1,4,5 increased by 8% (11% in constant currency) to €3.58 (2017: €3.33). In Q4/18, Group net income1,4,5 increased by 6% (6% in constant currency) to €542 million (Q4/17: €510 million). Earnings per share1,4,5 increased by 5% (5% in constant currency) to €0.97 (Q4/17: €0.92).

1Net income attributable to shareholders of Fresenius SE & Co. KGaA

2After special items

3Before special items

4Before special items and after adjustments

5Before expenses for the further development of the biosimilar business

Continued investment in growth

Spending on property, plant and equipment was €2,163 million (FY/17: €1,828 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. This corresponds to 6% of sales.

Total acquisition spending was €1,086 million (FY/17: €6,852 million). FY/17 spending had included the acquisition of Quirónsalud as well as the acquisition of the biosimilars business of Merck KGaA.

Cash flow development

Group operating cash flow decreased by 5% to €3,742 million (FY/17: €3,937 million) with a margin of 11.2% (FY/17: 11.6%). In FY/17 Fresenius Medical Care had received a ~€200 million payment under the VA agreement. The FY/18 cash flow was impacted by a change in working capital items at Fresenius Helios, the earnings decrease at Helios Germany and negative currency translation effects. Operating cash flow in Q4/18 increased by 7% to €1,193 million (Q4/17: €1,116 million) with a margin of 13.5% (Q4/17: 12.8%).

Given the effects described above in combination with growing investments, free cash flow before acquisitions and dividends decreased to €1,665 million (FY/17: €2,232 million). Free cash flow after acquisitions and dividends was €1,374 million (FY/17: -€4,557 million).

Solid balance sheet structure

The Group’s total assets increased by 7% (5% in constant currency) to €56,703 million (Dec. 31, 2017: €53,133 million). Current assets grew by 17% (17% in constant currency) to €14,790 million (Dec. 31, 2017: €12,604 million). Non-current assets increased by 3% (2% in constant currency) to €41,913 million (Dec. 31, 2017: €40,529 million).

Total shareholders’ equity increased by 15% (13% in constant currency) to €25,008 million (Dec. 31, 2017: €21,720 million). The equity ratio increased to 44.1% (Dec. 31, 2017: 40.9%).

Group debt was broadly stable (decreased by 2% in constant currency) at €18,984 million (Dec. 31, 2017: €19,042 million). Group net debt decreased by 6% (-8% in constant currency) to €16,275 million (Dec. 31, 2017: €17,406 million) mainly due to the proceeds from divestitures of Care Coordination activities at Fresenius Medical Care.

As of December 31, 2018, the net debt/EBITDA ratio was 2.711,2 (December 31, 2017: 2.841,2). Excluding the proceeds from divestitures of Care Coordination activities the net debt/EBITDA ratio was 2.911,2.

1At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, excluding effects from pending acquisition of NxStage by FMC

2Before special items

Business Segments

Fresenius Medical Care

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of December 31, 2018, Fresenius Medical Care was treating 333,331 patients in 3,928 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- 7% comparable sales growth in constant currency in Q4/18

- 9% comparable2 net income increase in constant currency in Q4/18

- Attractive share buyback program for 2019 and 2020

- Outlook for FY/19 (in constant currency): 3% to 7% adjusted sales growth3 and adjusted net income development4 in range of -2% to +2% expected

1Excluding VA agreement Q4/18: 6%; FY/18: 4%

2Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

3FY/18 base: €16,026 million; FY/18 adjusted for divestitures of Care Coordination activities; FY/19 adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

4FY/18 base: €1,341 million; FY/18 before special items and after adjustments; FY/19 before special items (before transcation-related expenses, expenses associated with the cost optimization program), adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

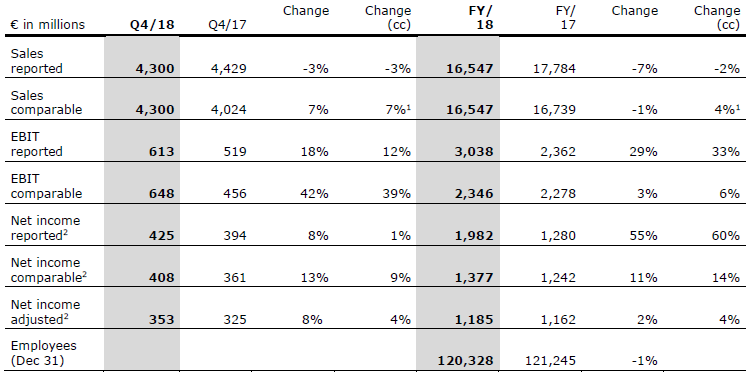

Sales decreased by 7% (-2% in constant currency) to €16,547 million (FY/17: €17,784 million). Organic sales growth was 4%. Currency translation effects reduced sales by 5%. The adoption of IFRS 15 reduced sales by 3%.

With the FY/17 base additionally adjusted for divestitures of Care Coordination activities, sales decreased by 1% (increased by 4% in constant currency).

In Q4/18, sales decreased by 3% (-3% in constant currency) to €4,300 million (Q4/17: €4,429 million). Organic sales growth was 6%. The adoption of IFRS 15 reduced sales by 2%. Q4/17 base additionally adjusted for divestitures of Care Coordination activities, sales in Q4/18 increased by 7% (7% in constant currency).

Health Care services sales1 (dialysis services and care coordination) decreased by 2% (increased by 4% in constant currency) to €13,264 million (FY/17: €13,487 million). Health Care product sales increased by 1% (5% in constant currency) to €3,283 million (FY/17: €3,252 million).

In North America, sales1 decreased by 2% (increased by 2% in constant currency) to €11,570 million (FY/17: €11,834 million). Health Care services sales1 decreased by 2% (increased by 2% in constant currency) to €10,725 million (FY/17: €10,991 million). Excluding the FY/17 effect from the VA Agreement (€94 million), Health Care services sales1 increased by 3% in constant currency. Health Care product sales of €845 million (FY/17: €843 million) were on the prior-year level (increased by 5% in constant currency).

1On a comparable basis

Sales outside North America increased by 1% (8% in constant currency) to €4,962 million (FY/17: €4,890 million). Health Care services sales increased by 2% (11% in constant currency) to €2,539 million (FY/17: €2,496 million). Health Care product sales increased by 1% (5% in constant currency) to €2,423 million (FY/17: €2,394 million).

Fresenius Medical Care’s EBIT increased by 29% (33% in constant currency) to €3,038 million (FY/17: €2,362 million), mainly driven by gains related to divestitures of Care Coordination activities. The EBIT margin increased to 18.4% (FY/17: 13.3%). EBIT on a comparable basis increased by 6% in constant currency and EBIT margin increased to 14.2% (FY/17: 13.6%).

In Q4/18, EBIT increased by 18% (12% in constant currency) to €613 million (Q4/17: €519 million). The EBIT margin increased to 14.3% (Q4/17: 11.7%). EBIT on a comparable basis increased by 42% (increased by 39% in constant currency) and EBIT margin increased to 15.1% (Q4/17: 11.3%).

Net income1 increased by 55% (60% in constant currency) to €1,982 million (FY/17: €1,280 million). Net income1 growth on a comparable basis was 14% in constant currency. Adjusted net income1 growth was 4% in constant currency.

In Q4/18, net income1 increased by 8% (1% in constant currency) to €425 million (Q4/17: €394 million). Net income1 growth on a comparable basis was 9% in constant currency. Adjusted net income1 growth was 4% in constant currency.

Operating cash flow was €2,062 million (FY/17: €2,192 million). The cash flow margin increased to 12.5% (FY/17: 12.3%). In Q4/18, operating cash flow was €698 million (Q4/17: €528 million). The cash flow margin increased to 16.2% (Q4/17: 11.9%).

For FY/19, Fresenius Medical Care expects adjusted sales to grow by 3% to 7%2 in constant currency. Net income1 is expected to develop in the range of -2% to +2%3 in constant currency in 2019.

For 2020, Fresenius Medical Care expects adjusted sales as well as adjusted net income to grow at a mid to high single digit rate, both at constant currency.

For further information, please see Fresenius Medical Care’s Press Release at www.freseniusmedicalcare.com.

1Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2FY/18 base: €16,026 million; FY/18 adjusted for divestitures of Care Coordination activities (H1/18); FY/19 adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

3FY/18 base: €1,341 million; FY/18 before special items and after adjustments; FY/19 before special items (before transaction-related expenses, expenses associated with the cost optimization program), adjusted for IFRS 16 effects, excluding effects from pending NxStage transaction

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, we are developing products with a focus on oncology and autoimmune diseases.

- 7% organic sales growth and 10% EBIT1 growth in constant currency (excl. biosimilars expenses) in FY/18

- Operating cash flow at all-time high

- FY/19 outlook: 3% to 6% organic sales growth5 and 3% to 6% EBIT6 growth in constant currency expected

1Before special items

2Before expenses for the further development of the biosimilars business: Q4/18: 8%; FY/18: 10%

3Net income attributable to shareholders of Fresenius SE & Co. KGaA

4Before expenses for the further development of the biosimilars business: Q4/18: 20%; FY/18: 21%

5FY/18 base: €6,544 million; FY/19 adjusted for IFRS 16 effects

6FY/18 base: €1,139 million; FY/18 before special items including expenditures for further development of biosimilars business (€120 million after tax); FY/19 before special items (before transaction-related expenses, revaluations of biosimilars contingent liabilities), adjusted for IFRS 16 effects

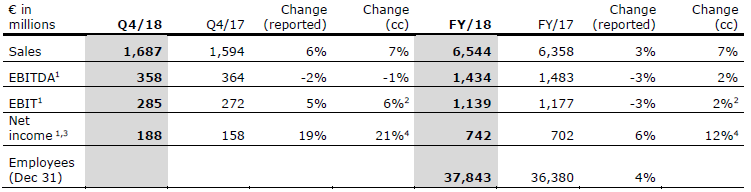

Sales increased by 3% (7% in constant currency) to €6,544 million (FY/17: €6,358 million). Organic sales growth was 7%. Strong negative currency translation effects of 4% were mainly related to the devaluation of the U.S. dollar, the Argentinian peso and the Brazilian real against the euro. In Q4/18, sales increased by 6% (7% in constant currency) to €1,687 million (Q4/17: €1,594 million). Organic sales growth was 7%.

Sales in Europe grew by 2% (organic growth: 3%) to €2,248 million (FY/17: €2,214 million). In Q4/18, sales in Europe increased by 2% (organic growth: 3%) to €590 million.

Sales in North America increased by 3% (organic growth: 8%) to €2,359 million (FY/17: €2,290 million). In Q4/18, sales increased by 8% (organic growth: 5%) to €599 million (Q4/17: €554 million).

Sales in Asia-Pacific increased by 9% (organic growth: 12%) to €1,300 million (FY/17: €1,196 million). In Q4/18, sales increased by 11% (organic growth: 13%) to €336 million (Q4/17: €302 million).

Sales in Latin America/Africa decreased by 3% (increased organically by 13%) to €637 million (FY/17: €658 million). In Q4/18, sales increased by 2% (organical growth: 18%) to €162 million (Q4/17: €159 million).

EBIT1 decreased by 3% (increased by 2% in constant currency) to €1,139 million (FY/17: €1,177 million) with an EBIT margin1 of 17.4% (FY/17: 18.5%). In Q4/18, EBIT1 increased by 5% (6% in constant currency) to €285 million (Q4/17: €272 million) with an EBIT margin1 of 16.9% (Q4/17: 17.1%).

EBIT1 before expenses for the further development of the biosimilars business increased by 5% (10% in constant currency) to €1,305 million (FY/17: €1,237 million) with an EBIT margin1 of 19.9% (FY/17: 19.5%). In Q4/18, EBIT1 before expenses for the further development of the biosimilars business increased by 6% (8% in constant currency) to €338 million (Q4/17: €318 million) with an EBIT margin1 of 20.0% (Q4/17: 19.9%).

Net income1,2 increased by 6% (12% in constant currency) to €742 million (FY/17: €702 million). In Q4/18, net income1,2 increased by 19% (21% in constant currency) to €188 million (Q4/17: €158 million).

Operating cash flow increased by 3% to on an all-time-high of €1,040 million (2017: €1,010 million), mainly driven by a strong operational performance. The cash flow margin was 15.9% (2017: 15.9%).

For FY/19, Fresenius Kabi expects organic sales growth3 of 3% to 6% and EBIT growth4 in constant currency of 3% to 6%.

1Before special items

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

3FY/18 base: €6,544 million; FY/19 adjusted for IFRS 16 effects

4FY/18 base: €1,139million; FY/18 before special items including expenditures for further development of biosimilars business (€120 million after tax); FY/19 before special items (before acquisition-related expenses, revaluations of biosimilars contingent liabilities), adjusted for IFRS 16 effects

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 86 hospitals, ~125 outpatient centers and treats approximately 5.3 million patients annually. Quirónsalud operates 47 hospitals, 57 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 13.3 million patients annually.

- 4% organic sales growth in Q4/18

- DRG catalogue effects and preparatory initiatives for regulatory changes continue to weigh on Helios Germany

- Helios Spain with dynamic growth

- FY/19 outlook3: 2% to 5% organic sales growth and EBIT decline of -5% to -2% expected

As of July 1, 2018 Fresenius Helios transferred its German post-acute care business to Fresenius Vamed. To allow a like-for-like comparison, we also provide sales and EBIT growth rates adjusted for the effects of this transaction.

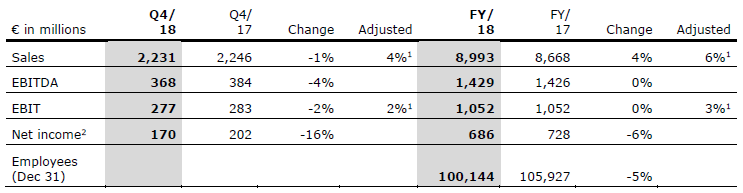

Fresenius Helios increased sales by 4% (6%1) to €8,993 million (FY/17: €8,668 million). Organic sales growth was 3%. In Q4/18, sales decreased by 1% (increased by 4%1; organic growth: 4%) to €2,231 million (Q4/17: €2,246 million).

Sales of Helios Germany decreased by 2% (increased by 2%1; organic growth: 2%) to €5,970 million (FY/17: €6,074 million). In Q4/18, sales decreased by 5% (increased by 3%1; organic growth: 3%) to €1,439 million (Q4/17: €1,512 million). Sales were impacted by a decline in admissions, inter alia due to an unexpectedly high fluctuation among doctors and a shortage of nursing staff as well as a trend towards outpatient treatments. The volume decline was offset by DRG inflator increases and better results from the negotiations with our payors.

Helios Spain increased sales by 17% (organic growth: 6%) to €3,023 million (FY/17: €2,594 million), mainly due to an excellent operating performance and an additional month of consolidation (Quirónsalud is consolidated since February 1, 2017). In Q4/18 Helios Spain increased sales by 8% (organic growth: 7%) to €792 million (Q4/17: €734 million).

Fresenius Helios EBIT remained unchanged (increased by 3%1) at €1,052 million (FY/17: €1,052 million) with a margin of 11.7% (FY/17: 12.1%). In Q4/18, EBIT decreased by 2% (increased by 2%1) to €277 million (Q4/17: €283 million) with a margin of 12.4% (Q4/17: 12.6%).

EBIT of Helios Germany decreased by 14% (-10%1) to €625 million (FY/17: €725 million) with a margin of 10.5% (FY/17: 11.9%). In Q4/18, EBIT decreased by 22% (-15%1) to €137 million (Q4/17: €176 million) with a margin of 9.5% (Q4/17: 11.6%). The significant fixed cost base in the hospital business has a strong operating leverage effect on EBIT as market dynamics and sales development slow down. The development of Helios Germany is impacted by additional catalogue effects, preparatory structural measures for expected regulatory requirements (e.g. clustering) and a lack of privatization opportunities in the German market. An unexpectedly high fluctuation among doctors and a shortage of nursing staff have an additional negative impact on the earnings development.

EBIT of Helios Spain increased by 26% to €413 million (FY/17: €327 million), mainly due to the strong operating performance and the additional month of consolidation, with a margin of 13.7% (FY/17: 12.6%). In Q4/18, EBIT increased by 19% to €127 million (Q4/17: €107 million) with a margin of 16.0% (Q4/17: 14.6%).

Net income2 of Fresenius Helios decreased by 6% to €686 million (FY/17: €728 million). In Q4/18, net income2 decreased by 16% to €170 million (Q4/17: €202 million).

Operating cash flow was €554 million (FY/17: €733 million) with a margin of 6.2% (FY/17: 8.5%). The decrease is mainly attributable to the earnings decrease at Helios Germany and the changes in working capital.

For FY/19, Fresenius Helios expects organic sales growth of 2% to 5% and an EBIT3 decline of -5% to -2%.

1Adjusted for German post-acute care business transferred to Fresenius Vamed

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

3Adjusted for IFRS 16 effects

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Excellent organic sales growth of 16% in FY/18

- Order intake at all-time high - strong foundation for future growth

- FY/19 outlook: ~10% organic sales growth and 15% to 20% EBIT growth3 expected

As of July 1, 2018 Fresenius Helios transferred its German post-acute care business to Fresenius Vamed. To allow for a like-for-like comparison, we also provide sales and EBIT growth rates adjusted for the effects of this transaction.

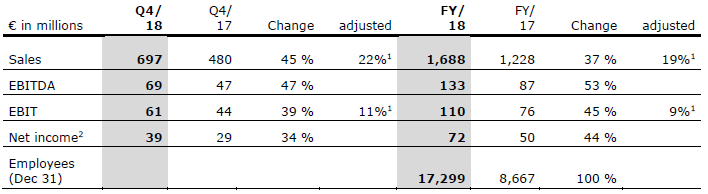

Sales increased by 37% (19%1) to €1,688 million (FY/17: €1,228 million). Organic sales growth was 16% with a strong momentum in both the project and service businesses as well as increased sales from services for Fresenius Helios. Sales of the project business increased by 17% to €712 million (FY/17: €606 million). Sales in the service business grew by 57% (20%1) to €976 million (FY/17: €622 million). In Q4/18, sales increased by 45% (22%1; organic growth: 20%) to €697 million (Q4/17: €480 million).

EBIT increased by 45% (9%1) to €110 million (FY/17: €76 million) with a margin of 6.5% (FY/17: 6.2%). In Q4/18, EBIT increased by 39% (11%1) to €61 million (Q4/17: €44 million) with a margin of 8.8% (Q4/17: 9.2%).

Net income2 increased by 44% to €72 million (FY/17: €50 million). In Q4/18, net income2 increased by 34% to €39 million (FY/17: €29 million).

Order intake increased by 12% to €1,227 million (FY/17: €1,096 million) and reached a new all-time high. As of December 31, 2018, order backlog was €2,420 million (December 31, 2017: €2,147 million).

For FY/19, Fresenius Vamed expects organic sales growth in the range of ~10% and EBIT growth3 of 15% to 20%.

1Without German post-acute care business acquired from Fresenius Helios

2Net income attributable to shareholders of VAMED AG

3Including the German post-acute care business acquired from Fresenius Helios, adjusted for IFRS 16 effects

Conference Call

As part of the publication of the results for fiscal year 2018, a conference call will be held on February 20, 2019 at 2 p.m. CET (8 a.m. EST). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.