November 6, 2024

Fresenius Q3/24: Simplification and focus drives sustained performance – Outlook upgraded

- Group organic revenue growth of 9%1,2 to €5.3 billion2 driven by a strong Kabi performance and good organic growth at Helios.

- Strong bottom-line traction with Group EBIT2 increase in constant currency of 9%3 to €552 million and EPS growth of 7%2,3,4

- Group outlook for fiscal 2024 upgraded; Organic revenue growth1,2 is now expected to grow between 6% to 8% (previous: between 4% to 7%) and EBIT growth2 in constant currency is now targeted to be in the 8 to 11% range (previous: between 6% to 10%).

- Group-wide cost and productivity savings ahead of plan with target for FY/24 already achieved YTD.

- Excellent operating cash flow resulting from focused cash management.

- Deleveraging continued, and leverage ratio further improved to 3.24x2,5 driven by excellent cash flow; Leverage target corridor under review.

- Fresenius Kabi delivering above the top-end of the structural growth band with organic revenue growth of 11%1; strong EBIT margin at 15.9%2.

- Growth Vectors at Kabi show continued strong performance, led by dynamic growth at Biopharma, which had yet again positive EBIT in Q3. Tyenne is in line with expectations, building on strong momentum.

- Fresenius Helios with excellent organic revenue growth of 8% driven by solid performance in Spain and supported by some favorable technical reclassifications in Germany; EBIT margin of 7.9%2 in line with expectations due to anticipated lower seasonal demand in Spain; last quarter of energy relief funding support.

- Dedicated Helios performance program underway to drive further operational excellence and compensate ending energy relief funding in Germany.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

3 Growth rate adjusted for Argentina hyperinflation

4 Excluding Fresenius Medical Care

5 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

Michael Sen, CEO of Fresenius: "Team Fresenius delivered an excellent third quarter in 2024 – all financial metrics improved versus the prior year. Revenues grew strongly, with margin expansion across the Group, and significantly improved cash flow generation. Both Kabi and Helios continue to deliver consistent and sustained financial performance. We are more focused and stronger, deploying our cash to reduce debt further, while growing earnings per share and driving shareholder returns. Quarter after quarter we are showing how our #FutureFresenius strategy is paying off. Our mission remains at the core of our activities: saving and improving human lives. Fresenius is: Committed to Life.”

Sen continued, “Given the strength of our first nine months, we are upgrading our revenue and earnings guidance for the year.”

Group sales and earnings development

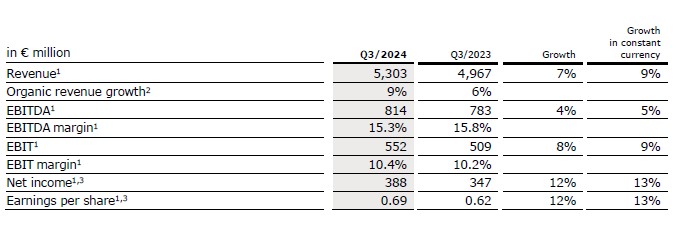

Group revenue before special items increased by 7% (9% in constant currency) to €5,303 million (Q3/23: €4,967 million). Organic growth was 9%2, driven by Kabi and Helios' ongoing strong performance. Currency translation had a negative effect of 2% on revenue growth.

Group EBITDA before special items increased by 4% (5% in constant currency) to €814 million (Q3/23: €783 million).

Group EBIT before special items increased by 8% (9% in constant currency) to €552 million (Q3/23: €509 million), mainly driven by the strong organic revenue growth at Kabi and Helios and the continued progress of the groupwide cost savings program. The EBIT margin before special items was 10.4% (Q3/23: 10.2%). Reported Group EBIT was €492 million (Q3/23: €362 million).

Group net interest before special items increased to -€116 million (Q3/23: -€102 million) mainly due to financing activities in a higher interest rate environment.

Group tax rate before special items was 24.5% (Q3/23: 23.1%).

1 Before special items

2 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

Net income1 from deconsolidated Fresenius Medical Care operations before special items increased by 38% (42% in constant currency) to €76 million (Q3/231: €55 million).

Group net income1 before special items increased by 12% (13% in constant currency) to €388 million (Q3/231: €347 million). The increase was driven by operating strength. Reported Group net income1 increased to €326 million (Q3/231: -€406 million) mainly due to Fresenius Medical Care's positive net income contribution. The negative net income in the prior year period was due to the non-cash valuation effect of Fresenius Medical Care in accordance with IFRS 5.

Group net income1 before special items excluding Medical Care increased by 7% (7% in constant currency) to €312 million (Q3/231: €292 million).

Earnings per share1 before special items increased by 12% (13% in constant currency) to €0.69 (Q3/231: €0.62). Reported earnings per share1 were €0.58 (Q3/231: -€0.72).

Group Cash flow development

Group operating cash flow (continuing operations) increased to €763 million (Q3/23: €603 million) mainly driven by the very good operational business development and improvements in working capital at Helios and Kabi. Group operating cash flow margin was 14.4% (Q3/23: 12.1%). Before acquisitions, dividends and lease liabilities, free cash flow (continuing operations) increased to €532 million (Q3/23: €346 million). After acquisitions, dividends and lease liabilities, free cash flow (continuing operations) improved to €623 million (Q3/23: €102 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Constant currency growth rates adjusted for Argentina hyperinflation. Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at Financial Results | FSE (fresenius.com)

Group leverage

Group debt decreased by -16% (-16% in constant currency) to €13,317 million (Dec. 31, 2023: € 15,830 million) mainly related to the repayment of debt based on the excellent cash flow development and the around €400 million reduction of the leasing liabilities related to the Vamed exit. Group net debt decreased by -11% (-11% in constant currency) to € 11,823 million (Dec. 31, 2023: € 13,268 million).

As of September 30, 2024, the net debt/EBITDA ratio was 3.24x1,2 (Dec. 31, 2023: 3.76x1,2) corresponding to a reduction of 52 bps compared to Dec. 31, 2023. This achievement is due to a combination of better EBITDA and Free cash flow. The legally required suspension of dividend payments and the Vamed exit further supported the positive development. Compared to Q3/23 (4.03x1,2) this is a 79 bps reduction.

Fresenius anticipates improving net debt/EBITDA ratio further3 towards the lower end of the self-imposed corridor of 3.0 to 3.5x by year-end 2024. This is expected to be driven by further reducing net debt and operational performance of the Operating Companies.

Structural productivity improvements: Target achieved ahead of plan

The Group-wide cost and efficiency measures are progressing faster than planned. The target for annual sustainable cost savings of ~€400 million at EBIT level has already been achieved with accumulative savings totaling €408 million until the end of Q3/24. Originally, it was expected to achieve the target by year-end 2025.

Fresenius will continue its efforts to increase structural productivity. So far, Kabi has delivered the majority of the savings. Going forward, it will be Fresenius Helios with its dedicated efficiency program focused on operations excellence including reduction of process and waiting times and digitalization of processes, resource optimization and synergies in particular in logistics and procurement. An update will be provided as part of the FY/24 results in February 2025.

Further efforts to enhance structural efficiency will, however, also be driven forward by Fresenius Kabi and the Corporate Center. Key elements include measures to reduce complexity, optimize supply chains and improve procurement processes.

1 At average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures, including lease liabilities, including Fresenius Medical Care dividend

2 Before special items

3 At expected average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions/divestitures; before special items; including lease liabilities, including Fresenius Medical Care dividend

For a detailed overview of special items please see the reconciliation tables at Financial Results | FSE (fresenius.com)

Operating Company Fresenius Kabi

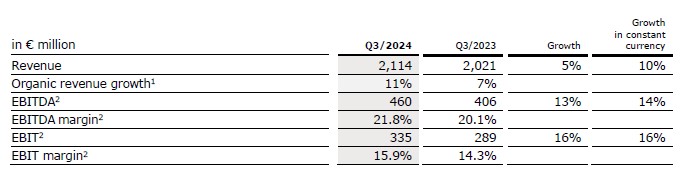

Revenue increased by 5% (10% constant currency) to €2,114 million (Q3/23: €2,021 million). Organic growth was 11%1. This performance was driven by positive pricing effects, particularly in Argentina, and the excellent operating performance of the Growth Vectors.

Revenue of the Growth Vectors (MedTech, Nutrition and Biopharma) increased by 9% (16% in constant currency) to €1,158 million (Q3/23: €1,067 million). Organic growth was excellent at 16%1.

In Nutrition, organic growth of 11%1 benefited from positive pricing effects in Argentina and the good development in the US, driven by the ongoing roll-out of lipid emulsions. China continued to be impacted by a general economic weakness, price declines in connection with tenders, and indirect effects of the government’s countrywide anti-corruption campaign. Biopharma showed excellent organic growth of 66%1 driven by the overall good Biosimilars rollout in Europe and the U.S., with Tyenne standing out. Moreover, mAbxience also performed strongly, driven by bevacizumab and milestone payments. In MedTech, organic growth was of 7%1 driven by a broad-based positive development in the US, Europe and International, reflecting strong performances for infusion and nutrition systems.

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Constant currency growth rates adjusted for Argentina hyperinflation.

For a detailed overview of special items please see the reconciliation tables at Financial Results | FSE (fresenius.com)

Revenue in the Pharma (IV Drugs & Fluids) business increased by 2% (3% in constant currency; organic growth: 6%1) and amounted to €957 million (Q3/23: €941 million). Organic growth was mainly driven by a strong performance in Europe and International and solid growth in the U.S., driven by an improved backorder situation, compensating the softer development in China.

EBIT2 of Fresenius Kabi increased by 16% (16% in constant currency) to €335 million (Q3/23: €289 million) mainly due to the good revenue development, the positive EBIT result of the Biopharma business, and ongoing progress of the cost saving initiatives. EBIT margin2 was 15.9% (Q3/23: 14.3%) and thus at the upper end of 2024 outlook.

EBIT2 of the Growth Vectors increased by 62% (constant currency: 53%) to €168 million (Q3/23: €104 million) due to the positive EBIT of the Biopharma business and the good revenue development. EBIT margin2 was 14.5% (Q3/23: 9.8%). The Biopharma business is now expected to be EBIT break-even also in the FY/24.

EBIT2 in the Pharma business decreased by -9% (constant currency: -8%) to €182 million (Q3/23: €200 million) primarily driven by additional costs due to the start of production at the main US plants in Wilson and Melrose Park. EBIT margin2 was 19.0% (Q3/23: 21.3%).

Operating Company Fresenius Helios

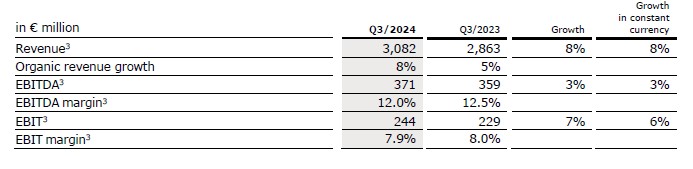

Revenue before special items increased by 8% (8% in constant currency) to €3,082 million (Q3/23: €2,863 million). Organic growth was 8%.

Revenue of Helios Germany increased by 8% (in constant currency: 8%) to €1,940 million (Q3/23: €1,800 million) due to pricing effects coupled with volume growth and supported by some favourable technical reclassifications. Organic growth was 8%.

Revenue of Helios Spain before special items increased by 8% (8% in constant currency) to €1,142 million (Q3/23: €1,062 million) driven by solid activity levels despite the anticipated lower seasonal demand, and favourable price effects. Organic growth was 8%. The clinics in Latin America also showed a good performance, additionally supported by currency exchange rate effects.

EBIT1 of Fresenius Helios increased by 7% (6% in constant currency) to €244 million (Q3/23: €229 million) with an EBIT margin1 of 7.9% (Q3/23: 8.0%).

EBIT1 of Helios Germany increased by 8% to €170 million (Q3/23: €157 million) with an EBIT margin1 of 8.8% (Q3/23: 8.7%). Q3/24 marked the last quarter in which energy relief funding was recognized in the income statement supporting profitability.

EBIT1 of Helios Spain decreased by -3% (0% in constant currency) to €73 million (Q3/23: €75 million) due to the expected seasonal softness and some phasing effects. The EBIT margin1 was 6.4% (Q3/23: 7.1%). On a more comparable nine-months basis, the EBIT margin1 was 11.2% (Q1-3/23: 11.2%).

1 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation.

2 Before special items

Constant currency growth rates adjusted for Argentina hyperinflation.

3 Before special items

Financial figures and growth rates adjusted for the divestment of the fertility services group Eugin and the hospital stake in Peru.

For a detailed overview of special items please see the reconciliation tables at Financial Results | FSE (fresenius.com)

Implications of the Fresenius Vamed exit

As of Q2 2024, Vamed is no longer a reporting segment of Fresenius. The company’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, is included under Corporate / Other in the Group consolidated segment reporting.

In Q1-3/24, the divestment of the rehabilitation business and the Vamed operations in Austria led to non-cash special items of €406 million at Group net income level.

Special items related to the gradual scale back of the international project business amounted to €441 million at Group EBIT level in Q1-3/24, and to €357 million1 at Group net income level. A total amount of high triple-digit million euros of special items is expected, which is spread over the next few years and will be mostly cash-effective.

Group and segment outlook for 20242

Fresenius upgrades its outlook for FY/24. Based on the excellent first nine months of 2024, Group organic revenue growth3,5,6 is now expected to grow between 6% to 8% (previous: between 4% to 7%) in 2024 and Group constant currency EBIT4,5 is anticipated to grow in an 8% to 11% range (previous: between 6% to 10%).

Fresenius Kabi expects organic revenue growth6 in a mid-to high-single-digit percentage range in 2024. The EBIT margin5 is expected to be in a range of 15% to 16% (structural margin band: 14% to 17%).

Fresenius Helios expects organic revenue5 to grow in mid-single digit percentage range in 2024. The EBIT margin5 is expected to be within 10% to 11% (structural margin band: 10% to 12%).

The Group outlook is given without Fresenius Vamed, i.e. exclusively for the Operating Companies Fresenius Kabi and Fresenius Helios.

1 According to ownership share

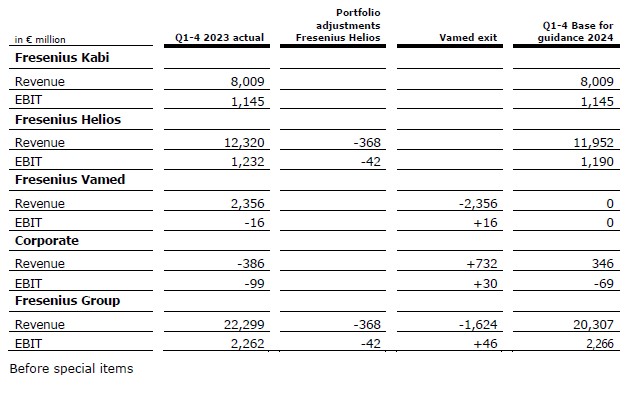

2 For the prior-year basis please see table “Basis for Guidance for 2024”

3 2023 base: €20,307 million

4 2023 base: €2,266 million

5 Before special items

6 Organic growth rate adjusted for accounting effects related to Argentina hyperinflation

Basis for Guidance for 2024

# # #

If no timeframe is specified, information refers to Q3/2024.

An overview of the results for Q3/2024 - before and after special items – is available on our website.

Consolidated results for Q3/24 as well as for Q3/23 include special items. These concern: divestment of the fertility services group Eugin and the hospital stake in Peru, Vamed exit, expenses associated with the Fresenius cost and efficiency program, transaction costs for mAbxience and Ivenix, costs in relation to the change of legal form of Fresenius Medical Care, legacy portfolio adjustments, IT transformation, transformation/exit Vamed, discontinued operations Vamed, special items at Fresenius Medical Care, and impact of PPA due to the application of the equity method to the Fresenius Medical Care investment. The special items shown within the reconciliation tables are reported in the Corporate/Other segment.

Note on the deconsolidation of Fresenius Medical Care

Following the deconsolidation of Fresenius Medical Care, Group financial figures are presented in accordance with IAS 28 (at equity method) since December 1, 2023. The proportionate share of 32% of Fresenius Medical Care is presented as a separate line in Fresenius Group’s P&L and balance sheet. Dividends received from Fresenius Medical Care are reported as a separate line as part of the cash flow statement. Moreover, IAS 28 requires a full purchase price allocation (PPA). The accounting for the PPA is treated as special item. For reasons of simplification and comparability, Fresenius presents net income with and without Fresenius Medical Care`s equity result.

Note on the portfolio optimization at Fresenius Helios

As part of the portfolio optimization, the sale of the fertility services group Eugin was completed on January 31, 2024. The divestment of the majority stake in the hospital Clínica Ricardo Palma hospital in Lima, Peru, was completed on April 23, 2024. Therefore, results of Fresenius Helios and accordingly of the Fresenius Group for Q3/24 and Q3/23 are adjusted.

Note on the growth rates Fresenius Kabi

Growth rates in constant currency of Fresenius Kabi are adjusted. Adjustments relate to the hyperinflation in Argentina. Accordingly, in constant currency growth rates of the Fresenius Group are also adjusted.

Note on the Vamed exit

Due to the application of IFRS 5, the prior year and prior quarter figures of the current year have been adjusted in the consolidated statement of income and the consolidated statement of cash flows. Vamed’s High-End-Services (HES) which offers services for Fresenius Helios and other hospitals, will be transferred to Fresenius and is included under Corporate / Other in the Group consolidated segment reporting. Details on the financial and accounting implications of the Vamed exit and the portfolio adjustments at Fresenius Helios are available on our website.

Information on the performance indicators are available on our website at https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, the availability of financing and unforeseen impacts of international conflicts. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.