July 30, 2021

Fresenius raises Group earnings guidance after very strong Q2

-

Fresenius Medical Care with expected continued COVID-19 impact; patient excess mortality rates significantly reduced

-

Fresenius Kabi’s strong Emerging Markets business more than offsets persistent headwinds in North America

-

Helios Germany with gradually increasing elective treatment volumes; Helios Spain delivers outstanding sales and earnings growth based on strong activity levels and a weak prior-year quarter

-

Fresenius Vamed back to growth driven by good performance in the service business; growing order book in the project business

-

First savings from initiatives to improve efficiency already expected in 202

If no timeframe is specified, information refers to Q2/2021.

1Before special items

2Net income attributable to shareholders of Fresenius SE & Co. KGaA

Stephan Sturm, CEO of Fresenius, said: “Overall, our interim result for the 2021 business year is very strong. We have achieved very healthy sales and earnings growth, despite the ongoing impact of the pandemic. Our businesses are developing well, and we are making good progress on our initiatives for profitable growth and increased efficiency. The increased vaccination rates in many of our important markets are encouraging, but of course the pandemic is not over yet. We must remain vigilant and will continue to monitor the infection situation very closely. Nevertheless, there are reasons for us to be optimistic: Our growth drivers are intact, good health is and will remain of paramount importance to everyone. We will continue the review of our structures, and to drive efficiency measures along with our growth initiatives. The resulting benefits will allow us to sustainably develop our healthcare group even more successfully.”

COVID-19 assumptions for guidance FY/21

Whilst the pandemic exhibited a quite differentiated regional development, negative COVID-effects have - consistent with expectations - generally receded during Q2/21.

Fresenius had projected that the burdens and constraints caused by the pandemic will recede in the second half of the year. Now, however, the currently rising number of COVID-19 cases, the further evolution of COVID-19 virus mutations as well as stalling vaccination progress could all pose a threat to this assumption, and the company remains vigilant.

Whilst the risk of renewed far-reaching containment measures in one or more of Fresenius’ major markets currently appears less likely, it cannot be excluded. Any resulting significant and direct impact on the health care sector without appropriate compensation is not reflected in the Group’s FY/21 guidance. These assumptions are subject to considerable uncertainty.

FY/21 Group earnings guidance raised

Based on the Group’s strong Q2/21 and the progress in the program to improve Group-wide efficiencies, where the company expects first savings already this year, Fresenius raises its 2021 earnings guidance. The Company now projects net income1,2 to grow in a low single-digit percentage range in constant currency. Previously, Fresenius expected an at least broadly stable net income1,2 development in constant currency. The Company continues to project sales growth3 in a low-to-mid single-digit percentage range in constant currency.

Implicitly, net income1 for the Group excluding Fresenius Medical Care is now expected to grow in a high single-digit percentage range in constant currency. Previously, Fresenius expected mid-to-high single-digit percentage growth in constant currency.

The guidance implies ongoing COVID-19 related headwinds in the second half of the year. It reflects negative pricing effects related to tender activity at Fresenius Kabi in China as well as increasingly noticeable cost inflation effects across selected markets.

Fresenius projects net debt/EBITDA4 to be around the top-end of the self-imposed target corridor of 3.0x to 3.5x by the end of FY/21.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 FY/20 base: €1,796 million, before special items; FY/21: before special items

3 FY/20 base: €36,277 million

4 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures; excluding further potential acquisitions; before special items

For a detailed overview of special items please see the reconciliation table in the PDF document.

Progress on efficiency measures to sustainably improve profitability

To sustainably enhance profitability and operational excellence, Fresenius has launched group-wide efficiency initiatives. These measures are expected to gradually result in cost savings of more than €100 million p.a. after tax and minority interest in 2023, with some potential to increase thereafter.

While an update on the comprehensive operating model review at Fresenius Medical Care is expected to be provided in fall 2021, the three other Fresenius business segments have already identified and launched initiatives in defined areas.

At Fresenius Kabi, these initiatives comprise the optimization of its production network, reduction of product portfolio complexity, centralization of worldwide purchasing and review of organizational and cost structures.

Fresenius Helios will put a focus on its strategic review of the hospital portfolio and ambulatory care network as well as on the reduction of G&A costs.

Fresenius Vamed will implement some dedicated structural and organizational measures, comprising the optimization of its global subsidiary structure, the review of its assets and shareholdings portfolio and the optimization of procurement and G&A costs.

These activities specific to the business segments will be complemented and supported by initiatives on the Fresenius group level, for example, the implementation of new ways of working at the corporate headquarters as well as a group-wide review of the IT operating model.

Achieving these sustainable efficiencies will require significant up-front expenses. For the years 2021 to 2023, those expenses are expected to be more than €100 million p.a. after tax and minority interest on average, with the largest portion currently expected to materialize in 2022. They will be classified as special items, consistent with previous practice.

The company expects significant contributions from all four business segments and from the corporate center in the 2021 to 2023 period. Hence, it is expected that the savings contributed by Fresenius Medical Care will not be overproportional.

For FY/21, initial low double-digit million € savings after tax and minority interest from the Group’s above outlined cost and efficiency measures are expected to support the Group’s profitability. These savings and efficiency gains derive from activities in all four business segments.

Stephan Sturm, CEO of Fresenius, said: “We examine possible cost reductions with great care; and we implement them in a very targeted way, with a sense of proportion. We are saving because we have goals and want to realize them: We want to give ever more people access to ever better medicine. We want to contribute to keeping – or making – people healthy, to helping people enjoy their lives despite an illness. That is why we have a responsibility to use our valuable resources carefully. We will prioritize resources where they can have the biggest impact, remove duplication, and stop activities where results are not satisfying. This fitness program will benefit everyone: Our patients, the healthcare system, our employees and our shareholders.”

8% sales increase in constant currency

Group sales increased by 4% (8% in constant currency) to €9,246 million (Q2/20: €8,920 million). Organic growth was 6%. Acquisitions/divestitures contributed net 2% to growth. Currency translation reduced sales growth by 4%. Excluding estimated COVID-19 effects1, Group sales growth would have been 6% to 7% in constant currency. In H1/21, Group sales increased by 1% (6% in constant currency) to €18,230 million (H1/20: €18,055 million). Organic growth was 4%. Acquisitions/divestitures contributed net 2% to growth. Currency translation reduced sales growth by 5%. Excluding estimated COVID-19 effects1, Group sales growth would have been 5% to 6% in constant currency.

20% net income2,3 increase in constant currency

Group EBITDA before special items decreased by 5% (0% in constant currency) to €1,671 million (Q2/20: €1,762 million). Reported Group EBITDA was €1,662 million (Q2/20: €1,762 million).

In H1/21, Group EBITDA before special items decreased by 6% (-1% in constant currency) to €3,302 million (H1/20: €3,517 million). Reported Group EBITDA was €3,290 million (H1/20: €3,517 million).

Group EBIT before special items decreased by 8% (-4% in constant currency) to €1,030 million (Q2/20: €1,123 million). The constant currency decrease is primarily due to COVID-19 related headwinds at Fresenius Medical Care. The EBIT margin before special items was 11.1% (Q2/20: 12.6%). Reported Group EBIT was €1,021 million (Q2/20: €1,123 million).

In H1/21, Group EBIT before special items decreased by 9% (-5% in constant currency) to €2,039 million (H1/20: €2,248 million). The constant currency decrease is primarily due to COVID-19 related headwinds at Fresenius Medical Care. The EBIT margin before special items was 11.2% (Q1/20: 12.5%). Reported Group EBIT was €2,027 million (H1/20: €2,248 million).

1 For estimated COVID-19 effects please see table in the PDF document

2 Before special items

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items please see the reconciliation table in the PDF document.

Group net interest before special items and reported net interest improved to -€121 million (Q2/202: -€167 million) mainly due to successful refinancing activities, lower interest rates as well as currency translation effects. In H1/21, Group net interest before special items improved to -€258 million (H1/202: -€341 million). Reported Group net interest improved to -€258 million (H1/20: -€349 million).

Group tax rate before special items was 21.5% (Q2/202: 23.5%) while reported Group tax rate was 21.3% (Q2/20: 23.4%). In H1/21, Group tax rate before special items was 22.1% (H1/202: 23.1%) while reported Group tax rate was 22.0% (H1/20: 23.0%).

Noncontrolling interests before special items were -€240 million (Q2/20: -€321 million) of which 89% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€237 million (Q2/20: -€321 million). In H1/21, noncontrolling interests before special items were -€477 million (H1/20: -€592 million) of which 92% were attributable to the noncontrolling interests in Fresenius Medical Care. Reported noncontrolling interests were -€473 million (Q2/20: -€592 million).

Group net income1 before special items increased by 16% (20% in constant currency) to €474 million (Q2/202: €410 million) driven by Helios Spain, Kabi’s Emerging Markets business as well as the favorable net interest development. Excluding estimated COVID-19 effects3, Group net income1 before special items would have grown 10% to 14% in constant currency. Reported Group net income1 increased to €471 million (Q2/20: €411 million).

In H1/21, Group net income1 before special items increased by 4% (8% in constant currency) to €910 million (H1/202: €875 million). Excluding estimated COVID-19 effects3, Group net income1 before special items would have grown 4% to 8% in constant currency. Reported Group net income1 increased to €906 million (H1/20: €870 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before special items

3 For estimated COVID-19 effects please see table in the PDF document.

For a detailed overview of special items please see the reconciliation table in the PDF document.

Earnings per share1 before special items increased by 15% (19% in constant currency) to €0.85 (Q2/202: €0.74). Reported earnings per share1 were €0.84 (Q2/20: €0.74). In H1/21, earnings per share1 before special items increased by 4% (8% in constant currency) to €1.63 (H1/202: €1.57). Reported earnings per share1 were €1.62 (H1/20: €1.56).

Continued investment in growth

Spending on property, plant and equipment was €509 million corresponding to 6% of sales (Q2/20: €474 million; 5% of sales). These investments served primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. In H1/21, spending on property, plant and equipment was €893 million corresponding to 5% of sales (H1/20: €1,021 million; 6% of sales).

Total acquisition spending was €491 million (Q2/20: €97 million) mainly for the acquisition of Eugin Group at Fresenius Helios which has been consolidated since April 1, 2021, and the acquisition of dialysis clinics at Fresenius Medical Care. In H1/21, total acquisition spending was €640 million (H1/20: €509 million).

Cash flow development

Group operating cash flow decreased to €1,451 million (Q2/20: €3,082 million) with a margin of 15.7% (Q2/20: 34.6%). The decline was mainly due to the U.S. federal government’s payments in Q2/20 under the CARES Act, the start of recoupment of these advanced payments in Q2/21 as well as the timing of certain other expense payments in 2021 at Fresenius Medical Care. Free cash flow before acquisitions and dividends decreased correspondingly to €952 million (Q2/20: €2,606 million). Free cash flow after acquisitions and dividends decreased to -€359 million (Q2/20: €2,374 million).

In H1/21, Group operating cash flow decreased to €2,103 million (H1/20: €3,960 million) with a margin of 11.5% (H1/20: 21.9%). Free cash flow before acquisitions and dividends decreased to €1,193 million (H1/20: €2,911 million). Free cash flow after acquisitions and dividends decreased to -€242 million (H1/20: €2,334 million).

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 Before Special items

Solid balance sheet structure

Group total assets increased by 5% (3% in constant currency) to €69,655 million (Dec. 31, 2020: €66,646 million) given the expansion of business activities and currency effects. Current assets increased by 7% (6% in constant currency) to €16,901 million (Dec. 31, 2020: €15,772 million) mainly driven by the increase of trade accounts receivables, cash and cash equivalents and inventories. Non-current assets increased by 4% (2% in constant currency) to €52,754 million (Dec. 31, 2020: €50,874 million).

Total shareholders’ equity increased by 4% (2% in constant currency) to €27,131 million (Dec. 31, 2020: €26,023 million). The equity ratio was 39.0% (Dec. 31, 2020: 39.0%).

Group debt increased by 5% (4% in constant currency) to €27,289 million (Dec. 31, 2020: € 25,913 million). Group net debt increased by 4% (3% in constant currency) to € 25,039 million (Dec. 31, 2020: € 24,076 million).

As of June 30, 2021, the net debt/EBITDA ratio increased to 3.60x1,2 (Dec. 31, 2020: 3.44x1,2) driven by COVID-19 effects weighing on EBITDA as well as increased net debt.

1 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

2 Before special items

For a detailed overview of special items please see the reconciliation table in the PDF document.

Number of employees

As of June 30, 2021, the Fresenius Group had 312,734 employees worldwide (December 31, 2020: 311,269).

Business Segments

Fresenius Medical Care (Financial data according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of June 30, 2021, Fresenius Medical Care was treating approximately 346,000 patients in more than 4,100 dialysis clinics. Along with its core business, the Renal Care Continuum, the company focuses on expanding in complementary areas and in the field of critical care.

- As assumed, COVID-19 pandemic continued to impact organic growth in dialysis and downstream businesses; patient excess mortality rates significantly reduced

- Negative exchange rate effects continue

- Earnings development impacted by phasing and strong prior-year base, as indicated

- Financial targets for FY 2021 confirmed

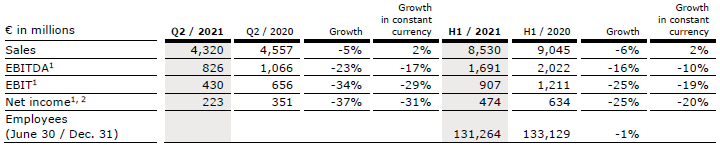

Sales of Fresenius Medical Care decreased by 5% (increased by 2% in constant currency) to €4,320 million (Q2/20: €4,557 million). Thus, currency translation had a negative effect of 7%. Organic growth was 1%. In H1/21, sales of Fresenius Medical Care decreased by 6% (increased by 2% in constant currency) to €8,530 million (H1/20: €9,045 million). Thus, currency translation had a negative effect of 8%. Organic growth was 1%.

EBIT decreased by 35% (-30% in constant currency) to €424 million (Q2/20: €656 million) resulting in a margin of 9.8% (Q2/20: 14.4%). EBIT before special items declined by 34% to €430 million (-29% in constant currency; Q2/20: €656 million), resulting in a margin of 10.0% (Q2/20: 14.4%). The decrease was mainly due to the adverse impact of the COVID-19 pandemic, including a high prior-year base as a result of government relief funding, the expected phasing and increase in Sales, General and Administrative expense, negative exchange rate effects and higher direct costs. These effects were partially offset in particular by an improved Medicare Advantage payor mix in the U.S.

1 Before special items

2 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

For a detailed overview of special items please see the reconciliation table in the PDF document.

In H1/21, EBIT decreased by 26% (-20% in constant currency) to €898 million (H1/20: €1,211 million) resulting in a margin of 10.5% (H1/20: 13.4%). EBIT before special items decreased by 25% (-19% in constant currency) to €907 million (Q2/20: €1,211 million) resulting in an EBIT margin excluding special items of 10.6% (H1/20: 13.4%).

Net income1 decreased by 38% (-33% in constant currency) to €219 million (Q2/20: €351 million). Net income1 before special items decreased by 37% (-31% in constant currency) to €223 million (Q2/20: €351 million).

In H1/21, net income1 decreased by 26% (-21% in constant currency) to €468 million (H1/20: €634 million). Net income1 before special items decreased by 25% (-20% in constant currency) to €474 million (H1/20: €634 million).

Operating cash flow was €921 million (Q2/20: €2,319 million) with a margin of 21.3% (Q2/20: 50.9%). The decline was mainly due to the U.S. federal government’s payments in Q2/20 under the CARES Act, the start of recoupment of these advanced payments in Q2/21 as well as the timing of certain other expense payments in 2021. In H1/21, operating cash flow was €1,129 million (H1/20: €2,903 million) with a margin of 13.2% (H1/20: 32.1%).

For FY/21, Fresenius Medical Care confirms its outlook as outlined in February 2021. The Company expects revenue2 to grow at a low-to-mid single-digit percentage range and net income1,3 to decline at a high-teens to mid-twenties percentage range against the 2020 base4. This outlook is based on the assumption of a return to normalized mortality rates in H2/21.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 FY/20 base: €17,859 million

3 FY/20 base: €1,359 million, before special items; FY/21: before special items

4 These targets are based on the 2020 results excluding the impairment of goodwill and trade names in the Latin America Segment of €195 million. They are inclusive of anticipated COVID-19 effects, in constant currency and exclude special items. Special items include costs related to FME25 and other effects that are unusual in nature and have not been foreseeable or not foreseeable in size or impact at the time of giving guidance.

For a detailed overview of special items please see the reconciliation table in the PDF document.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- North America performance impacted by COVID-19 and competitive pressure; effects of temporary manufacturing issues receding

- Normalizing demand in Europe driving strong growth over a COVID-impacted base

- Very strong Emerging Markets growth; China with strong performance given more normalized elective treatment activity

- Outlook improved to low single-digit constant currency EBIT percentage growth

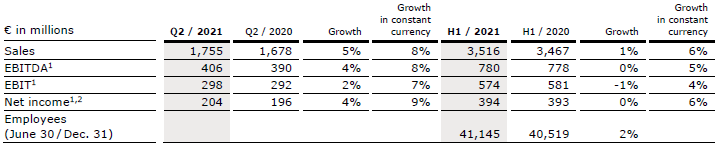

Sales increased by 5% (8% in constant currency) to €1,755 million (Q2/20: €1,678 million). Organic growth was 7%. In H1/21, sales increased by 1% (6% in constant currency) to €3,516 million (H1/20: €3,467 million). Organic growth was 5%. Negative currency translation effects of 3% in Q2 and 5% in H1 were mainly related to the weakness of the US dollar, the Argentinian peso and the Brazilian real.

Sales in North America decreased by 13% (organic growth: -6%) to €522 million (Q2/20: €600 million). The decrease was driven by reduced volume demand given fewer elective treatments, consequential competitive pressure and, albeit receding, temporary manufacturing issues. These negative effects outweighed extra demand for COVID-19 related products. In H1/21, sales in North America decreased by 15% (organic growth: -8%) to €1,080 million (H1/20: €1,269 million).

Sales in Europe increased by 12% (organic growth: 10%) to €634 million (Q2/20: €566 million) supported by a low prior-year basis meaningfully impacted by COVID-19. In H1/21, sales in Europe increased by 5% (organic growth: 4%) to €1,260 million (H1/20: €1,197 million).

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

Sales in Asia-Pacific increased by 17% (organic growth: 17%) to €409 million (Q2/20: €351 million). The growth is mainly due to more normalized elective treatment activity in China as well as a recovery in other Asian markets. In H1/21, sales in Asia-Pacific increased by 20% (organic growth: 21%) to €801 million (H1/20: €670 million).

Sales in Latin America/Africa increased by 18% (organic growth: 24%) to €190 million (Q2/20: €161 million) due to ongoing COVID-19 related extra demand. In H1/21, sales in Latin America/Africa increased by 13% (organic growth: 26%) to €375 million (H1/20: €331 million).

EBIT1 increased by 2% (7% in constant currency) to €298 million (Q2/20: €292 million) with an EBIT margin of 17.0% (Q2/20: 17.4%). The increase in constant currency was tempered by underutilized production capacities in the US and competitive pressure coupled with selective supply constraints due to temporary, however receding, manufacturing issues. EBIT was supported by positive COVID-19 effects, lower corporate costs due to travel restrictions and phasing of projects. In H1/21, EBIT1 decreased by 1% (increased by 4% in constant currency) to €574 million (H1/20: €581 million) with an EBIT margin of 16.3% (H1/20: 16.8%).

Net income1,2 increased by 4% (9% in constant currency) to €204 million (Q2/201: €196 million). In H1/21, net income1,2 remained stable (increased by 6% in constant currency) at €394 million (H1/201: €393 million).

Operating cash flow decreased to €197 million (Q2/20: €437 million) with a margin of 11.2% (Q2/20: 26.0%) mainly due to the phasing of tax payments and payments for legal proceedings. In H1/21, operating cash flow decreased to €475 million (H1/20: €611 million) with a margin of 13.5% (H1/20: 17.6%).

For FY/21, Fresenius Kabi improves its EBIT outlook. The company now projects EBIT3 to grow in a low single-digit percentage range in constant currency. Previously, Fresenius Kabi expected a stable EBIT3 development up to low single-digit percentage growth. The company continues to expect organic sales growth4 in a low-to-mid single-digit percentage range. Both sales and EBIT outlook include expected COVID-19 effects.

1 Before special items

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 FY/20 base: €1,095 million, before special items; FY/21: before special items

4 FY/20 base: €6,976 million

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain. Helios Germany operates 89 hospitals, ~130 outpatient centers and 6 prevention centers. Helios Spain operates 47 hospitals, 74 outpatient centers and around 300 occupational risk prevention centers. In addition, the company is active in Latin America with 6 hospitals and as a provider of medical diagnostics and reproduction medicine worldwide.

- Gradually recovering elective treatments at Helios Germany

- Excellent treatment activity at Helios Spain results in outstanding organic sales and earnings growth over a weak prior year quarter

- Growth additionally fueled by contributions from acquisitions in Germany and Latin America as well as from the acquired fertility business

- Outlook improved for organic sales and constant currency EBIT growth

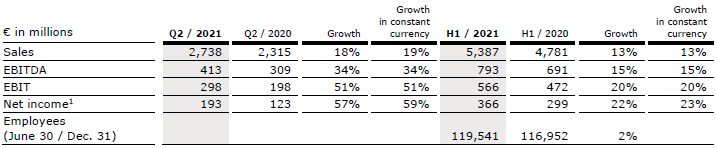

Sales increased by 18% (19% in constant currency) to €2,738 million (Q2/20: €2,315 million). Organic growth was 14%. Acquisitions, including the fertility business Eugin, (consolidated as from 1 April 2021), contributed 5% to sales growth. In H1/21, sales increased by 13% (13% in constant currency) to €5,387 million (H1/20: €4,781 million). Organic growth was 9%. Acquisitions contributed 4% to sales growth.

Sales of Helios Germany increased by 7% (organic growth: 3%) to €1,675 million (Q2/20: €1,571 million) driven by a gradual recovery of elective treatments and positive case mix effects. The hospital acquisitions from the Order of Malta contributed 4% to sales growth. In H1/21, sales of Helios Germany increased by 5% (organic growth: 1%) to €3,348 million (H1/20: €3,174 million). COVID-19 effects were mostly mitigated by government compensation.

Sales of Helios Spain increased by 37% (38% in constant currency) to €1,020 million (Q2/20: €743 million) over a weak COVID-19 impacted prior-year quarter. Organic growth of 38% was driven by a consistently high level of treatments and ongoing demand for occupational risk prevention (ORP) services. The Latin American hospitals contributed 5% to sales growth. In H1/21, sales of Helios Spain increased by 24% (26% in constant currency) to €1,996 million (H1/20: €1,606 million). Organic growth was 24%.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

EBIT of Fresenius Helios increased by 51% (51% in constant currency) to €298 million (Q2/20: €198 million) with an EBIT margin of 10.9% (Q2/20: 8.6%). In H1/21, EBIT of Fresenius Helios increased by 20% (20% in constant currency) to €566 million (H1/20: €472 million) with an EBIT margin of 10.5% (H1/20: 9.9%).

EBIT of Helios Germany increased by 3% to €152 million (Q2/20: €147 million) with an EBIT margin of 9.1% (Q2/20: 9.4%). In H1/21, EBIT of Helios Germany decreased by 3% to €302 million (H1/20: €312 million) with an EBIT margin of 9.0% (H1/20: 9.8%). Government compensation broadly mitigated COVID-19 effects.

EBIT of Helios Spain increased by 172% (174% in constant currency) to €147 million (Q2/20: €54 million) over a weak COVID-19 impacted prior-year quarter. EBIT margin improved to 14.4% (Q2/20: 7.3%). Healthy organic sales growth led to an improved coverage of the fixed cost base. The hospital acquisitions in Colombia contributed nicely. In H1/21, EBIT of Helios Spain increased by 64% (66% in constant currency) to €273 million (H1/20: €166 million) with an EBIT margin of 13.7% (H1/20: 10.3%).

Net income1 increased by 57% (59% in constant currency) to €193 million (Q2/20: €123 million). In H1/21, net income1 increased by 22% (23% in constant currency) to €366 million (H1/20: €299 million).

Operating cash flow decreased to €223 million (Q2/20: €295 million) with a margin of 8.1% (Q1/20: 12.7%) resulting from the strong cash collection in Q2/20 related to accelerated payments of treatment invoices under the German law to ease the financial burden on hospitals. In H1/21, operating cash flow was on prior year level at €438 million (H1/20: €440 million) with a margin of 8.1% (H1/20: 9.2%).

For FY/21, Fresenius Helios improves its outlook: The company now expects organic sales2 growth in a mid single-digit percentage range. Previously, organic sales2 were expected to grow in a low-to-mid single-digit percentage range. Moreover, Fresenius Helios now projects EBIT3 to grow in a high single-digit percentage range in constant currency. Previously, EBIT3 was expected to grow in a mid- to high single-digit percentage range in constant currency. Both sales and EBIT outlook include expected COVID-19 effects.

1 Net income attributable to shareholders of Fresenius SE & Co. KGaA

2 FY/20 base: €9,818 million

3 FY/20 base: €1,025 million; FY/21 before special items

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Back to sales and earnings growth despite negative COVID-19 effects

- Project business still marked by COVID-19 but showing clear signs of recovery

- Good performance in the service business; rehabilitation business improving as number of elective surgeries increased

- Excellent order intake

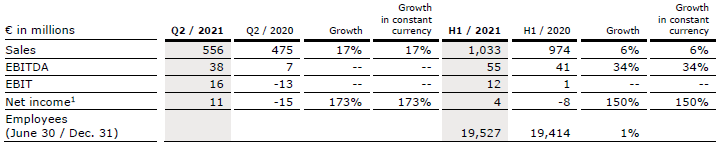

Sales increased by 17% (17% in constant currency) to €556 million (Q2/20: €475 million). Organic growth was 17%. In H1/21, sales increased by 6% (6% in constant currency) to €1,033 million (H1/20: €974 million). Organic growth was 6%.

Sales in the service business improved by 19% (19% in constant currency) to €392 million (Q2/20: €329 million), in particular driven by growing case numbers in the rehabilitation business. Sales in the project business increased by 12% (12% in constant currency) to €164 million (Q2/20: €146 million). In H1/21, sales in the service business increased by 10% (10% in constant currency) to €755 million (H1/20: €686 million). Sales in the project business decreased by 3% (-3% in constant currency) to €278 million (H1/20: €288 million).

EBIT increased to €16 million (Q2/20: -€13 million) with an EBIT margin of 2.9% (Q2/20:

-2.7%). In H1/21, EBIT increased to €12 million (H1/20: €1 million) with an EBIT margin of 1.2% (H1/20: 0.1%).

Net income1 increased to €11 million (Q2/20: -€15 million). In H1/21, net income1 increased to €4 million (H1/20: -€8 million).

1 Net income attributable to shareholders of VAMED AG

Order intake was outstanding with €713 million (Q2/20: €50 million) and €851 million in H1/21 (H1/20: €174 million), particularly driven by a turnkey project for a hospital in Wiener Neustadt, Austria. As of June 30, 2021, order backlog was at €3,635 million (December 31, 2020: €3,055 million).

Operating cash flow increased to €58 million (Q2/20: €28 million) with a margin of 10.4% (Q1/20: 5.9%) mainly due to payments from the international project business. In H1/21, operating cash flow increased to €14 million (H1/20: €8 million) with a margin of 1.4% (H1/20: 0.8%).

For FY/21, Fresenius Vamed confirms its outlook and expects organic sales1 growth in a mid-to-high single-digit percentage range and EBIT2 to grow to a high double-digit Euro million amount. Both sales and EBIT outlook include expected COVID-19 effects.

1 FY/20 base: €2,068 million

2 FY/20 base: €29 million; FY/21 before special items

Conference Call

As part of the publication of the results for Q2/2021, a conference call will be held on July 30, 2021 at 1:30 p.m. CEDT (7:30 a.m. EDT).You are cordially invited to follow the conference call in a live broadcast over the Internet at https://www.fresenius.com/media-calendar. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to our website https://www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.