July 30, 2019

Fresenius raises Group sales growth guidance after good second quarter

- Good organic sales growth across all business segments

- Growth investments well on track

- Fresenius Kabi successfully launched first biosimilar in Europe; continued excellent growth in Emerging Markets

- Fresenius Helios showing strong organic sales growth in Germany and enters successfully Colombian hospital market

- Fresenius Medical Care’s strategy reinforced by U.S. government’s plans for changes of kidney disease care

If no timeframe is specified, information refers to Q2/2019

1 Adjusted for IFRS 16 effect

2 Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities at Fresenius Medical Care (FMC)

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

Group sales growth guidance for 2019 raised

Based on the Group’s good H1/19 results and good prospects for the remainder of the year, Fresenius raises its 2019 Group sales growth guidance. Fresenius now projects sales growth1 of 4% to 7% in constant currency. Previously, Fresenius expected sales growth1 of 3% to 6% in constant currency. The company confirms its earnings guidance. Net income2,3 growth is expected to be ~0% in constant currency. The guidance for 2019 includes the related sales and dilutive earnings contributions of the NxStage acquisition.

Fresenius expects net debt/EBITDA4 at year-end to be around the upper-end of the original self-imposed target corridor of 2.5x to 3.0x. This includes the NxStage acquisition which is increasing the net debt/EBITDA ratio in 2019 by ~30 basis points and excludes IFRS 16 effects.

Due to the adoption of the IFRS 16 accounting standard (“IFRS 16 effect”), Fresenius’ self-imposed target corridor has shifted to 3.0x to 3.5x net debt/EBITDA on a reported basis.

1 On a comparable basis: FY/18 base: €33,009 million; FY/18 adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: adjusted for IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 On a comparable basis: FY/18 base: €1,872 million; FY/18 before special items and adjusted for divestitures of Care Coordination activities at FMC (H1/18); FY/19: before special items (transaction-related expenses, revaluations of biosimilars contingent liabilities, gain related to divestitures of Care Coordination activities at FMC, expenses associated with the cost optimization program at FMC), adjusted for IFRS 16 effect

4 Both net debt and EBITDA calculated at expected annual average exchange rates; excluding further potential acquisitions

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

6% sales growth1 in constant currency

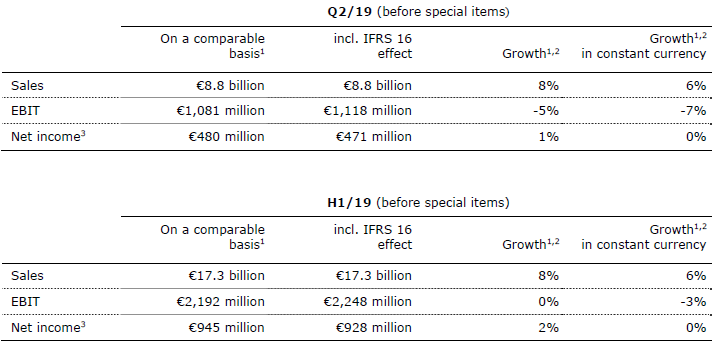

Group sales were €8,761 million including an IFRS 16 effect of -€18 million. Group sales1 on a comparable basis increased by 8% (6% in constant currency) to €8,779 million (Q2/18: €8,124 million). Organic sales growth was 5%. Acquisitions/divestitures contributed net 1% to growth. In H1/19, Group sales were €17,256 million including an IFRS 16 effect of -€40 million. Group sales1 on a comparable basis increased by 8% (6% in constant currency) to €17,296 million (H1/18: €15,994 million). Organic sales growth was 5%. Acquisitions/divestitures contributed net 1% to growth. Positive currency translation effects of 2% were mainly driven by the U.S. dollar strengthening against the euro.

Net income2,3 growth in constant currency

Group EBITDA before special items was €1,703 million including an IFRS 16 effect of €242 million. Group EBITDA2 on a comparable basis decreased by 2% (-5% in constant currency) to €1,461 million (Q2/18: €1,495 million). In H1/19, Group EBITDA before special items was €3,404 million including an IFRS 16 effect of €462 million. Group EBITDA2 on a comparable basis increased by 2% (-1% in constant currency) to €2,942 million (H1/18: €2,889 million).

Group EBIT before special items was €1,118 million including an IFRS 16 effect of €37 million. Group EBIT2 on a comparable basis decreased by 5% (-7% in constant currency) to €1,081 million (Q2/18: €1,135 million). The EBIT margin2 on a comparable basis was 12.3% (Q2/18: 14.0%). A significant contributor was the reduction in patient attribution and a decreasing savings rate for ESCOs, based on recent reports for prior plan years (“ESCO effect”). Reported Group EBIT4 was €1,118 million. In H1/19, Group EBIT before special items was €2,248 million including an IFRS 16 effect of €56 million. Group EBIT2 on a comparable basis remained at previous year’s level (-3% in constant currency) at €2,192 million (H1/18: €2,185 million). The EBIT margin2 on a comparable basis was 12.7% (H1/18: 13.7%). Reported Group EBIT4 was €2,233 million.

Group net interest before special items was -€180 million including an IFRS 16 effect of -€58 million. On a comparable basis, net interest2 improved to -€122 million (Q2/18: -€140 million) mainly due to successful refinancing activities and lower interest rates. Reported Group net interest4 was -€179 million. In H1/19, Group net interest before special items was -€361 million including an IFRS 16 effect of -€106 million. On a comparable basis, net interest1 improved to -€255 million (H1/18: -€279 million). Reported Group net interest3 was -€363 million.

1 On a comparable basis: Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities at FMC;

Q2/19 and H1/19 adjusted for IFRS 16 effect

2 On a comparable basis: Q2/19 and H1/19 before special items and adjusted for IFRS 16 effect;

Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities at FMC

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

4 After special items and including IFRS 16 effect

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

The Group tax rate before special items and adopting IFRS 16 was 22.8%. Group tax rate1 on a comparable basis was 22.8% (Q2/18: 23.3%). In H1/19, the Group tax rate before special items and adopting IFRS 16 was 23.1%. In H1/19, Group tax rate1 on a comparable basis was 23.1% (H1/18: 22.1%).

Noncontrolling interest before special items was €253 million including an IFRS 16 effect of €7 million. Noncontrolling interest1 on a comparable basis was €260 million (Q2/18:

€290 million). In H1/19, Noncontrolling interest before special items was €524 million including an IFRS 16 effect of €20 million. Noncontrolling interest1 on a comparable basis was €544 million (H1/18: €560 million), of which 93% was attributable to the Noncontrolling interest in Fresenius Medical Care.

Group net income2 before special items was €471 million including an IFRS 16 effect of -€9 million. Group net income1,2 on a comparable basis increased by 1% (0% in constant currency) to €480 million (Q2/18: €473 million). Reported Group net income2,3 was €471 million. Earnings per share2 before special items were €0.85 including an IFRS 16 effect of -€0.01. Earnings per share1,2 on a comparable basis increased by 1% (0% in constant currency) to €0.86 (Q2/18: €0.85). Reported Earnings per share2,3 were €0.85.

In H1/19, Group net income2 before special items was €928 million including an IFRS 16 effect of -€17 million. Group net income1,2 on a comparable basis increased by 2% (0% in constant currency) to €945 million (H1/18: €924 million). Reported Group net income2,3 was €924 million. In H1/19, Earnings per share2 before special items were €1.67 including an IFRS 16 effect of -€0.03. Earnings per share1,2 on a comparable basis increased by 2% (0% in constant currency) to €1.70 (H1/18: €1.66). Reported Earnings per share2,3 were €1.66.

Continued investment in growth

2019 is an investment year for the Fresenius Group. Fresenius is making good progress in all of its investment initiatives to secure long-term sustainable growth. Spending on property, plant and equipment was €565 million (Q2/18: €451 million). This corresponds to 6% of sales. In H1/19, spending on property, plant and equipment was €1,006 million (H1/18: €831 million), primarily for the modernization and expansion of dialysis clinics, production facilities as well as hospitals and day clinics. This corresponds to 6% of sales.

Total acquisition spending was €234 million (Q2/18: €194 million) including the acquisition of Clínica Medellín in Colombia by Fresenius Helios, among others. In H1/19, total acquisition spending was €2,157 million (H1/18: €386 million), mainly for the acquisition of NxStage by Fresenius Medical Care.

1 On a comparable basis: Q2/19 and H1/19 before special items and adjusted for IFRS 16 effect;

Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities at FMC

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 After special items and including IFRS 16 effect

Cash flow development

Group operating cash flow was €1,205 million including an IFRS 16 effect of €182 million. On a comparable basis, Group operating cash flow was €1,023 million (Q2/18: €1,020 million) with a margin of 11.7% (Q2/18: 12.2%). Free cash flow before acquisitions and dividends adjusted for IFRS 16 was €467 million (Q2/18: €580 million). Free cash flow after acquisitions and dividends adjusted for IFRS 16 was -€437 million (Q2/18: €1,331 million). The IFRS 16 effect amounts to €182 million respectively. Correspondingly, cash flow from financing activities decreased by €182 million.

In H1/19, Group operating cash flow was €1,494 million including an IFRS 16 effect of €353 million. On a comparable basis, Group operating cash flow was €1,141 million (H1/18: €1,256 million) with a margin of 6.6% (H1/18: 7.6%). Free cash flow before acquisitions and dividends adjusted for IFRS 16 was €128 million (H1/18: €425 million) mainly due to increasing investments. Free cash flow after acquisitions and dividends adjusted for IFRS 16 was -€2,719 million (H1/18: €942 million). The IFRS 16 effect amounts to €353 million respectively. Correspondingly, cash flow from financing activities decreased by €353 million.

Solid balance sheet structure

The Group’s total assets were €64,929 million including an IFRS 16 effect of €5,587 million. Adjusted for IFRS 16, Group total assets1 increased by 5% (4% in constant currency) to €59,342 million (Dec. 31, 2018: €56,703 million). Current assets1 remained flat (remained flat in constant currency) to €14,851 million (Dec. 31, 2018: €14,790 million). Non-current assets1 increased by 6% (6% in constant currency) to €44,491 million (Dec. 31, 2018: € 41,913 million).

Total shareholders’ equity was €25,382 million including an IFRS 16 effect of -€186 million. Adjusted for IFRS 16, total shareholders’ equity increased by 2% (2% in constant currency) to €25,568 million (Dec. 31, 2018: €25,008 million). The equity ratio was 39.1%. Adjusted for IFRS 16, the equity ratio was 43.1% (Dec. 31, 2018: 44.1%).

Group debt was €26,879 million including an IFRS 16 effect of €5,773 million. Adjusted for IFRS 16, Group debt increased by 11% to €21,106 million (11% in constant currency) (Dec. 31, 2018: € 18,984 million). Group net debt was €25,416 million including an IFRS 16 effect of €5,773 million. Adjusted for IFRS 16, Group net debt increased by 21% (21% in constant currency) to € 19,643 million (Dec. 31, 2018: € 16,275 million) mainly due to the acquisition of NxStage by Fresenius Medical Care.

As of June 30, 2019, the net debt/EBITDA ratio increased to 3.21x1,2,3,4 (December 31, 2018: 2.71x2,4). Including the IFRS 16 effect, the reported net debt/EBITDA ratio increased to 3.64x2,3,4.

1 Adjusted for IFRS 16 effect

2 At LTM average exchange rates for both net debt and EBITDA; pro forma closed acquisitions/divestitures

3 Including acquisition of NxStage

4 Before special items

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32.

Business Segments

Fresenius Medical Care (Figures according to Fresenius Medical Care press release)

Fresenius Medical Care is the world's largest provider of products and services for individuals with renal diseases. As of June 30, 2019, Fresenius Medical Care was treating 339,550 patients in 3,996 dialysis clinics. Along with its core business, the company provides related medical services in the field of Care Coordination.

- 5% sales1,2 growth in constant currency

- Underlying dialysis business development as expected; negative impact from ESCO adjustments for prior plan years

- FY/19 outlook confirmed

Adjusted for the Q2/18 contribution from the divested Care Coordination activities, the IFRS 16 effect and the contribution from NxStage, sales of Fresenius Medical Care increased by 8% (5% at constant currency) to €4,284 million (Q2/18: €3,956 million). Organic sales growth was 4%. Positive currency translation effects of 3% were mainly related to the U.S. dollar strengthening against the euro. In H1/19, sales adjusted for the H1/18 contribution from the divested Care Coordination activities, the IFRS 16 effect and the contribution from NxStage increased by 9% (5% at constant currency) to €8,409 million (H1/18: €7,680 million). Organic sales growth was 5%.

EBIT4 decreased by 12% (-17% in constant currency) to €491 million (Q2/19: €558 million) The EBIT margin4 decreased to 11.5% (Q2/18: 14.1%). A significant contributor was the reduction in patient attribution and a decreasing savings rate for ESCOs, based on recent reports for prior plan years (“ESCO effect”).

1 On an adjusted basis: before special items (transaction-related expenses, gain related to divestitures of Care Coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

2 Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities

3 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

4 Q2/18 and H1/18 before special items and after adjustments; Q2/19 and H1/19 before special items (transaction-related expenses, gain related to divestitures of Care Coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32.

In H1/19, EBIT6 decreased by 2% (-7% in constant currency) to €1,042 million (H1/18: €1,064 million). The EBIT margin4 decreased to 12.4% (H1/18: 13.9%).

Net income1,2 decreased by 9% (-14% in constant currency) to €279 million (Q2/18: €308 million). A significant contributor was the ESCO effect. In H1/19, net income1,2 decreased by 1% (-6% in constant currency) to €597 million (H1/18: €604 million).

Operating cash flow was €700 million3 (Q2/18: €656 million) with a margin of 16.0% (Q2/18: 15.6%). In H1/19, operating cash flow was €635 million (H1/18: €611 million) with a margin of 7.6% (H1/18: 7.5%).

For FY/19, Fresenius Medical Care expects adjusted sales to grow by 3% to 7%5,6 in constant currency. Adjusted net income1 is expected to develop in the range of -2% to +2%5,7 in constant currency.

For further information on the IFRS 16 reconciliation of Fresenius Medical Care, please see page 18 in the PDF document.

For further information, please see Fresenius Medical Care’s press release at www.freseniusmedicalcare.com.

1 Net income attributable to shareholders of Fresenius Medical Care AG & Co. KGaA

2 Q2/18 and H1/18 before special items and after adjustments; Q2/19 and H1/19 before special items (transaction-related expenses, gain related to divestitures of care coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effect, excluding effects from NxStage transaction

3 €852 million including an IFRS 16 effect of €152 million

4 €928 million including an IFRS 16 effect of €293 million

5 FY/18 before special items, Q2/18 and H1/18 adjusted for divestitures of Care Coordination activities;

FY/19 before special items (transaction-related expenses, gain related to divestitures of care coordination activities, expenses associated with the cost optimization program), adjusted for IFRS 16 effects, excluding effects from NxStage transaction

6 FY/18 base: €16,026 million

7 FY/18 base: €1,341 million

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 in the PDF document.

Fresenius Kabi

Fresenius Kabi offers intravenously administered generic drugs, clinical nutrition and infusion therapies for seriously and chronically ill patients in the hospital and outpatient environments. The company is also a leading supplier of medical devices and transfusion technology products. In the biosimilars business, Fresenius Kabi develops products with a focus on oncology and autoimmune diseases.

- 4% organic sales growth and 4% EBIT1 growth in constant currency

- Excellent growth in Emerging Markets

- FY/19 outlook confirmed

Sales of Fresenius Kabi increased by 5% (5% in constant currency) to €1,691 million (Q2/18: €1,604 million). Organic sales growth was 4%. In H1/19, sales increased by 6% (4% in constant currency) to €3,392 million (H1/18: €3,207 million). Organic sales growth was 4%. Positive currency translation effects of 2% were mainly related to the U.S. dollar strengthening against the euro.

Sales in North America increased by 4% (organic growth: -1%) to €573 million (Q2/18: €549 million). In H1/19, sales in North America increased by 5% (organic growth:

-1%) to €1,196 million (H1/18: €1,140 million). The anticipated easing of shortage situations, intensified competition in individual molecules, and a prescribing trend towards non-opioids pain management were the main headwinds.

Sales in Europe grew by 2% (organic growth: 1%) to €572 million (Q2/18: €563 million). In H1/19, sales in Europe increased by 2% (organic growth: 2%) to €1,145 million (H1/18: €1,120 million).

Sales in Asia-Pacific increased by 15% (organic growth: 15%) to €374 million (Q2/18: €326 million). In H1/19, sales in Asia-Pacific increased by 14% (organic growth: 13%) to €715 million (H1/18: €627 million).

Sales in Latin America/Africa increased by 4% (organic growth: 13%) to €172 million (Q2/18: €166 million). In H1/19, sales in Latin America/Africa increased by 5% (organic growth: 15%) to €336 million (H1/18: €320 million).

EBIT1 increased by 7% (4% in constant currency) to €308 million (Q2/18: €289 million) with an EBIT margin1 of 18.2% (Q2/18: 18.0%). In H1/19, EBIT1 increased by 10% (6% in constant currency) to €611 million (H1/18: €557 million) with an EBIT margin1 of 18.0% (H1/18: 17.4%).

Net income1,2 increased by 14% (12% in constant currency) to €211 million (Q2/18: €185 million). In H1/19, net income1,2 increased by 17% (12% in constant currency) to €414 million (H1/18: €355 million).

Operating cash flow3 was €201 million (Q2/18: €228 million). The cash flow margin was 11.9% (Q2/18: 14.2%). In H1/19, operating cash flow3 was €333 million (H1/18: €454 million). The cash flow margin was 9.8% (H1/18: 14.2%).

Fresenius Kabi confirms its outlook for FY/19 and expects organic sales growth4 of 3% to 6% and EBIT growth5 in constant currency of 3% to 6%.

For further information on the IFRS 16 reconciliation of Fresenius Kabi, please see page 18 of the PDF document.

1 On a comparable basis: before special items and adjusted for IFRS 16 effect

2 Net income attributable to shareholders of Fresenius SE & Co. KGaA

3 Adjusted for IFRS 16 effect (operating cash flow after special items)

4 On a comparable basis: FY/18 base: €6,544 million; FY/19 before special items (acquisition-related expenses, revaluations of biosimilars contingent liabilities) and adjusted for IFRS 16 effect

5 On a comparable basis: FY/18 base: €1,139 million; FY/18 before special items; FY/19 before special items (acquisition-related expenses, revaluations of biosimilars contingent liabilities) and adjusted for IFRS 16 effect.

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

Fresenius Helios

Fresenius Helios is Europe's leading private hospital operator. The company comprises Helios Germany and Helios Spain (Quirónsalud). Helios Germany operates 86 hospitals, ~125 outpatient centers and treats approximately 5.3 million patients annually. Quirónsalud operates 50 hospitals, 62 outpatient centers and around 300 occupational risk prevention centers, and treats approximately 13.3 million patients annually.

- Strong organic sales growth of 5%

- Helios Germany further stabilized; Helios Spain with solid growth despite Easter effect

- FY/19 outlook confirmed

Sales of Fresenius Helios remained at previous year’s level (increased by 6%1 organic growth: 5%) to €2,349 million (Q2/18: €2,343 million). In H1/19, sales also remained at previous year’s level (increased by 5%1; organic growth: 4%) to €4,660 million (H1/18: €4,674 million).

Sales of Helios Germany decreased by 3% (increased by 5%1; organic growth: 5%) to €1,506 million (Q2/18: €1,547 million). Organic sales growth was positively influenced by pricing effects and a strong case mix. In H1/19, sales of Helios Germany decreased by 4% (increased by 3%1; organic growth: 3%) to €2,991 million (H1/18: €3,121 million).

Sales of Helios Spain increased by 6% (organic growth: 4%) to €842 million (Q2/18: €796 million) despite the negative effect related to the Easter holidays. In H1/19, sales of Helios Spain increased by 7% (organic growth: 6%) to €1,668 million (H1/18: €1,553 million).

1 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

EBIT1 of Fresenius Helios decreased by 6% (-4% ) to €274 million (Q2/18: €293 million) with an EBIT margin of 11.7% (Q2/18: 12.5%). In H1/19, EBIT1 of Fresenius Helios decreased by 5% (-4%2) to €540 million (H1/18: €571 million) with an EBIT margin of 11.6% (H1/18: 12.2%).

EBIT1 of Helios Germany decreased by 8% (-4%2) to €154 million (Q2/18: €168 million) with an EBIT margin of 10.2% (Q2/18: 10.9%). In H1/19, EBIT1 of Helios Germany decreased by 12% (-10%2) to €303 million (H1/18: €345 million) with an EBIT margin of 10.1% (H1/18: 11.1%). Whilst EBIT and margin have further stabilized, investments for preparatory structural measures continue to weigh on Helios Germany’s financial performance.

Despite the negative Easter effect, EBIT1 of Helios Spain increased by 1% to €125 million (Q2/18: €124 million) with an EBIT margin of 14.8% (Q2/18: 15.6%). In H1/19, EBIT1 of Helios Spain increased by 7% to €244 million (H1/18: €227 million).

Net income1,3 decreased by 7% to €183 million (Q2/18: €197 million). In H1/19, net income1,3 also decreased by 7% to €359 million (H1/18: €388 million).

Operating cash flow1 was €197 million (Q2/18: €162 million) with a margin of 8.4% (Q2/18: 6.9%). In H1/19, operating cash flow1 was €288 million (H1/18: €259 million) with a margin of 6.2% (H1/18: 5.5%). The increase is mainly attributable to the decrease in days sales outstanding (DSO) at Helios Spain.

Fresenius Helios confirms its outlook for FY/19 and expects organic sales growth of 2% to 5% and an EBIT1 growth of -5% to -2%.

For further information on the IFRS 16 reconciliation of Fresenius Helios, please see page 18.

1 Adjusted for IFRS 16 effect

2 Adjusted for the post-acute care business transferred to Fresenius Vamed as of July 1, 2018

3 Net income attributable to shareholders of Fresenius SE & Co. KGaA

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

Fresenius Vamed

Fresenius Vamed manages projects and provides services for hospitals and other health care facilities worldwide and is a leading post-acute care provider in Central Europe. The portfolio ranges along the entire value chain: from project development, planning, and turnkey construction, via maintenance and technical management to total operational management.

- Very strong organic sales growth of 27%

- Intensified collaboration with Fresenius Helios contributes to sales growth

- FY/19 outlook confirmed

Sales of Fresenius Vamed increased by 76% (31%1) to €467 million (Q2/18: €266 million). Organic sales growth was 27%, acquisitions contributed 3%1 to growth. Positive currency translation effects increased sales by 1%. Sales in the service business grew by 106% (35%1) to €344 million (Q2/18: €167 million), supported by an intensified collaboration with Fresenius Helios. Sales of the project business increased by 24% to €123 million (Q2/18: €99 million). In H1/19, sales increased by 76% (32%1) to €907 million (H1/18: €515 million). Organic sales growth was 29%, acquisitions contributed 3%1 to growth. Both the service and the project business showed strong growth momentum.

EBIT2 increased by 67% to €20 million (Q2/18: €12 million) with an EBIT margin of 4.3% (Q2/18: 4.5%). EBIT2 additionally adjusted for the acquisition of Helios’ German post-acute care business was €8 million (-33% YoY) with an EBIT margin of 2.3% - the decrease was mainly driven by phasing effects in the project business. In H1/19, EBIT2 increased by 72% to €31 million (H1/18: €18 million) with an EBIT margin of 3.4% (H1/18: 3.5%). EBIT2 additionally adjusted for the acquisition of Helios’ German post-acute care business was €15 million (-17% YoY) with an EBIT margin of 2.2%.

Net income2,3 increased by 86% to €13 million (Q2/18: €7 million). In H1/19, net income2,3 increased by 73% to €19 million (H1/18: €11 million).

Order intake decreased by -41% to €115 million (Q2/18: €195 million) but increased by 9% to €498 million in H1/19 (H1/18: €455 million). As of June 30, 2019, order backlog was at €2,690 million (Dec 31, 2018: €2,420 million).

Operating cash flow2 decreased to -€42 million (Q2/18: -€14 million) with a margin of -9.0% (Q2/18: -5.3%). In H1/19, Operating cash flow2 decreased to -€65 million (H1/18:

-€56 million) with a margin of -7.2% (H1/18: -10.9%).

Fresenius Vamed confirms its outlook for FY/19 and expects organic sales growth of ~10% and EBIT growth2 of 15% to 20%.

For further information on the IFRS 16 reconciliation of Fresenius Vamed, please see page 18 of the PDF document.

1 Adjusted for German post-acute care business acquired from Fresenius Helios as of July 1, 2018

2 Adjusted for IFRS 16 effect

3 Net income attributable to shareholders of VAMED AG

For a detailed overview of special items and adjustments please see the reconciliation tables on pages 20-32 of the PDF document.

Conference Call

As part of the publication of the results for the second quarter / first half of 2019, a conference call will be held on July 30, 2019 at 1:30 p.m. CEDT (7:30 a.m. EDT). All investors are cordially invited to follow the conference call in a live broadcast over the Internet at www.fresenius.com/investors. Following the call, a replay will be available on our website.

For additional information on the performance indicators used please refer to our website www.fresenius.com/alternative-performance-measures.

This release contains forward-looking statements that are subject to various risks and uncertainties. Future results could differ materially from those described in these forward-looking statements due to certain factors, e.g. changes in business, economic and competitive conditions, regulatory reforms, results of clinical trials, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings, and the availability of financing. Fresenius does not undertake any responsibility to update the forward-looking statements in this release.